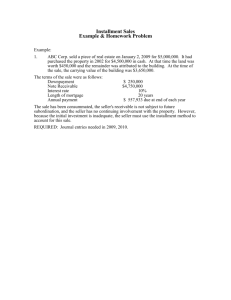

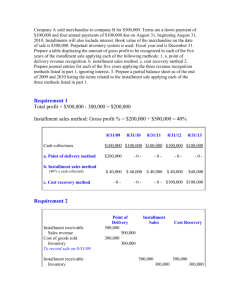

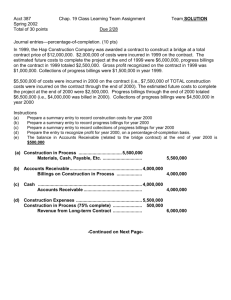

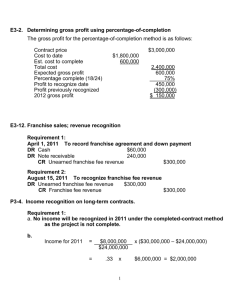

CHAPTER 18 Revenue Recognition

advertisement