Bond Basics - First Empire Securities

advertisement

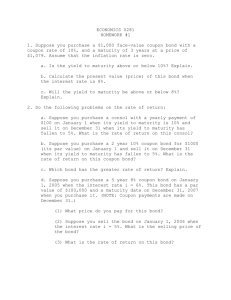

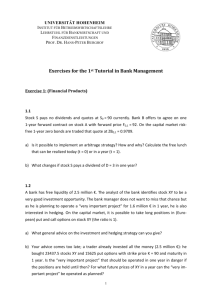

Member NASD/SIPC Bond Basics TYPES OF ISSUERS There are essentially five entities that issue bonds: US TREASURY SECURITIES - Issued by the U.S. Treasury Department and guaranteed by the “full faith and credit of the United States Government”. US AGENCY SECURITIES - Issued by an Agency of the U.S. Government ( i.e. Federal National Mortgage Association) and backed by the “full faith and credit” of the issuing Agency with the implied backing of the U.S. Government. MUNICIPAL BONDS – Issued by State or Local Municipalities ( i.e. The State of New York) and backed by the “full faith and credit”, taxing and revenue generating power of the issuing municipality. CORPORATE BONDS - Issued by a public corporation (i.e. IBM) and backed by the assets and earning power of the corporation. COLLATERALIZED BONDS - Issued by a special purpose trust (i.e. Asset-Backed Security) and backed by the issuer’s credit-worthiness and/or the underlying collateral, whose cash flow is used to pay the bondholders. MORTGAGE-BACKED SECURITIES – Issued by a U.S. Government Agency, whose cash flow comes from a specific pool of residential home mortgages. TYPES OF FIXED INCOME SECURITIES AGENCY DEBENTURES- Bond issued by a U.S. Government Agency or QuasiU.S. Agency, where the proceeds are used to fund the general operations, and whose cashflow is derived from the general operations or the issuer (Ex. Federal National Mortgage Association, Student Loan Marketing Association, etc.). ARMs – An Adjustable Rate Mortgage Backed Security, backed by a specific pool of adjustable rate residential mortgages. ASSET-BACKED SECURITIES - A series of bonds, whose cash flow is provided by a specific pool of collateral ( ex. Automobile loan receivables, credit card receivables, etc.) BALLOONS – A Mortgage-Backed Security, whose cash flow is provided by a specific pool of residential balloon mortgages. These securities have an intermediate term maturity of 5 to 10 years. CMOs (Collateralized Mortgage Obligation) – A series of bonds, whose cash flow is provided by a specific pool of Mortgage Backed Securities. CORPORATE BONDS - A bond issued by a publicly traded company or corporation, backed by the assets and earning power of the issuer. Headquarters – 100 Motor Parkway, 2nd Floor, Hauppauge, New York 11788-5157 Tel: 631-979-0097 Toll Free: 800-645-5424 Toll Free Branches: 800-551-2971 Fax: 631-979-0448 Website: www.1empire.com The information contained herein was obtained from sources we believe to be reliable. However, we do not guarantee it is accurate or complete. This information is for educational purposes only. This information is not and should not be construed as a offer or solicitation to buy or sell any security or securities. First Empire Securities, Inc. Member NASD/SIPC. Member NASD/SIPC DUS BONDS (“Delegated Underwriting and Servicing” Balloon MortgageBacked Security) - A DUS Balloon MBS is a bond backed by a specific pool of multi-family Balloon mortgages. The owner of the property has agreed in their mortgage to a “shorter term” final maturity in the form of a Balloon payment, and a substantial prepayment penalty over the life of the mortgage. (This prepayment penalty is a significant economic dis-incentive for the property owner to refinance, even if interest rates have fallen.) In addition, most DUS Balloons do not allow partial prepayments. During the yield maintenance period, if the property owner does refinance, typically a portion of the prepayment penalty is also passed through to the bondholder along with the principal and final interest payment. FHLMC PCs (Federal Home Loan Mortgage Corp. Participation Certificate) - A bond issued by “Freddie Mac” backed by a specific pool of residential home mortgages. The Mortgage-Backed Securities are issued by Freddie Mac. FNMA MBSs (Federal National Mortgage Association) - A bond issued by “Fannie Mae” backed by a specific pool of residential home mortgages. The Mortgage-Backed Securities are issued by Fannie Mae. GNMA PASS THROUGHS (Government National Mortgage Association Pass Through Security) – A bond issued by “Ginnie Mae” backed by a specific pool of residential home mortgages. The Mortgage-Backed Securities are issued by Ginnie Mae. GOs - A municipal bond backed by the “full faith and credit” and general taxing power of the issuer. Issued by municipalities, schools districts, and municipal authorities. NEGOTIABLE CDs – A time deposit with a Federally insured bank or savings and loan that can be traded in the secondary market. REVENUE BONDS - A municipal bond backed by the revenues generated by a specific municipal project ( ex. Toll road bonds, sports stadium bonds etc.). STEP-UPS - A security with a fixed coupon rate through its call date, where, if the bond is not called, the coupon will “step-up” (adjust up) to a new coupon rate. The call date (or dates) and coupons are established at issuance. TREASURY BILLS – Short term zero coupon bond issued (auctioned by the U.S. Treasury Department) on a weekly basis. New issues carry maturities of three months, six months, and one year. TREASURY BONDS - Long term securities issued (auctioned by the U.S. Treasury Department on a semi-annual basis with a maturity of 30 years. TREASURY NOTES – Intermediate term securities issued (auctioned) by the U.S. Treasury department on a periodic basis with maturities of two years, three years, five years, and ten years. Headquarters – 100 Motor Parkway, 2nd Floor, Hauppauge, New York 11788-5157 Tel: 631-979-0097 Toll Free: 800-645-5424 Toll Free Branches: 800-551-2971 Fax: 631-979-0448 Website: www.1empire.com The information contained herein was obtained from sources we believe to be reliable. However, we do not guarantee it is accurate or complete. This information is for educational purposes only. This information is not and should not be construed as a offer or solicitation to buy or sell any security or securities. First Empire Securities, Inc. Member NASD/SIPC. Member NASD/SIPC THE SECONDARY MARKET After issuance and prior to maturity, a bond can be bought and/or sold (“traded”) by its owner to another investor. Bonds are bought and sold in this “secondary market” at a negotiated price. The price is quoted as a percentage of face value and is referred to as being at a premium, at par, or at a discount. For instance, if the price were “par”, the bond would be selling at 100.00% of face value. A “discount” price might be 99.00% (verbally quoted as “ninety-nine”), and a “premium” price might be 101.00% (quoted as one-0-one). PRICE The price paid for a particular bond is based upon the general level of interest rates at the time of purchase. When a security is issued, the coupon rate will generally be reflective of the current interest rate environment, and the price will be at or close to par (100.00% of face value). After the bond is issued, if interest rates go down, the price of the bond will go up (to more than 100.00% of face value). This happens because a new bond issued in the lower interest rate environment would have a lower coupon rate, and trade at or close to par. The investor selling the older bond (with a higher coupon rate) would demand a higher price (a “premium”) for the bond (it has a higher coupon, pays more interest and, therefore is more valuable). Conversely, after a bond is issued, if interest rates go up, the price for the security will decline (to a “discount”), because its coupon will be less valuable. Of course, no investor is obligated to sell a bond prior to maturity regardless of whether interest rates rise or fall. YIELD The price paid by the buyer will equate to an “effective yield” to the bond’s stated maturity. The effective yield to maturity is calculated using a mathematical combination of the price paid, the coupon interest rate and the remaining term to maturity. The following are some examples: 1)PRICE = 100.00 (par) PAR VALUE = $1,000,000.00 TERM TO MATURITY = 10 years COUPON = 10.00% - paid semi-annually EFFECTIVE YIELD = 10% At purchase the investor will pay exactly $1 million to buy the bond ($1 million par values TIMES the 100.00% price). The investor will receive semi-annual interest payments of $50,000 (10% coupon TIMES the $1 million principal DIVIDED by 2), and the $1 million principal investment repaid at the end of ten years. This gives the investor a net effective annual yield of 10% ($100,000 annual net interest income DIVIDED by the principal of $1 million = 10%). For example: 2)PRICE = 90.00% (“ninety”) PAR VALUE = $1,000,000.00 TERM TO MATURITY = 10 years COUPON = 10.00% - paid semi-annually EFFECTIVE YIELD = 11.00% Headquarters – 100 Motor Parkway, 2nd Floor, Hauppauge, New York 11788-5157 Tel: 631-979-0097 Toll Free: 800-645-5424 Toll Free Branches: 800-551-2971 Fax: 631-979-0448 Website: www.1empire.com The information contained herein was obtained from sources we believe to be reliable. However, we do not guarantee it is accurate or complete. This information is for educational purposes only. This information is not and should not be construed as a offer or solicitation to buy or sell any security or securities. First Empire Securities, Inc. Member NASD/SIPC. Member NASD/SIPC At purchase the investor will pay only $900,000 to buy the bond ($1 million par value TIMES 90.00% price). In effect, the investor has received an annual DISCOUNT of $10,000 ($100,000 discount DIVIDED by 10 years to maturity). The investor will receive the same semi-annual interest payments of $50,000 (the 10% coupon rate TIMES the $1 million par value DIVIDED by 2), and the full par value of $1 million at maturity. When you add the effective annual discount (+ $10,000) to the annual interest payments ($100,000), this gives the investor a net effective yield of 11% ($100,00 total annual income DIVIDED by $1 million par = 11%). 2)PRICE = 100.00% (“one ten”) PAR VALUE = $1,000,000 TERM TO MATURITY = 10 years COUPON = 10.00% - paid semi-annually EFFECTIVE YIELD = 9% SPECIAL REDEMPTION FEATURES A bond has a stated maturity date and the issuer is contractually obligated to repay the bondholder’s principal on that date. Some securities allow the issuer more flexibility by having a special redemption feature. If the issuer is allowed to pay off the bondholder prior to the maturity date, the bond is said to be “callable”. If the bondholder is given the option to “cash-in” a bond prior to the maturity date, the bond is said to be “putable”. If a bond has a call (or put) feature, it will state the exact date (or dates) when the early redemption can be exercised. For example, a 10-year final maturity bond may contain a call feature allowing the issuer to “call” the bond (pay off the bondholder) after five years or any time thereafter. The issuer might choose to call the bond after five years if interest rates have fallen. The issuer could then “refinance” the debt with a new bond issue (at a lower interest rate) for the remaining five years. YIELD TO CALL If a bond is called prior to maturity and the investor paid a price other than par (a premium or discount) the effective yield on the investment will be affected: Bonds Bought at a Premium If called, the yield will be LESS than the yield to maturity. Bonds Bought at a Discount If called, the yield will be HIGHER than the yield to maturity. Bonds Bought at a Par If called, the yield will be THE SAME as the yield to maturity. Headquarters – 100 Motor Parkway, 2nd Floor, Hauppauge, New York 11788-5157 Tel: 631-979-0097 Toll Free: 800-645-5424 Toll Free Branches: 800-551-2971 Fax: 631-979-0448 Website: www.1empire.com The information contained herein was obtained from sources we believe to be reliable. However, we do not guarantee it is accurate or complete. This information is for educational purposes only. This information is not and should not be construed as a offer or solicitation to buy or sell any security or securities. First Empire Securities, Inc. Member NASD/SIPC. Member NASD/SIPC The yield is affected on premium and discount bonds, because the exercise of the call shortens the effective maturity of the investment. Therefore, the investor has less time in which to amortize the premium or discount and this will change the effective yield. For example: 1)PRICE = 90.00% PAR VALUE = $1,000,000 TERM TO MATURITY = 10 years CALLABLE = one time only at 5 years COUPON = 10.00% - paid semi-annually EFFECTIVE YIELD TO MATURITY = 11.00% EFFECTIVE YIELD TO CALL = 12.00% At purchase, the investor will pay only $900,000 to buy the bond ($1 million par value TIMES 90.00% price). If the bond is “called” after 5 years, the investor has received an annual DISCOUNT of $20,000 ($100,000 discount DIVIDED by the 5 years to the call – as opposed to dividing by 10 years to maturity). The investor will receive the same semiannual interest payments of $50,000 (the 10% coupon rate TIMES the $1 million par value DIVIDED by 2) and the full par value of $1 million on the call date. When you add the effective annual discount (+$20,000) to the annual interest payments ($100,000), this gives the investor a net effective annual yield of 12% ($120,000 total annual income DIVIDED by $1 million par = 12%). This is referred to as the “yield to call” and is higher than the yield to maturity of 11%. For example: 2) PRICE = 110.00% (“one-ten”) PAR VALUE = $1,000,000 TERM TO MATURITY = 10 years CALLABLE = one time only at 5 years COUPON = 10.00% paid semi-annually EFFECTIV YIELD TO MATURITY = 9% EFFECTIVE YIELD TO CALL = 8% At purchase, the investor will pay $1,100,000 to buy the bond ($1 million par value TIMES 110.00% price). If the bond is called after 5 years, the investor has paid an effective annual premium of $20,000 ($100,000 premium paid DIVIDED by the 5 years to the call). The investor will receive the same semi-annual interest payments of $50,000 (the 10% coupon rate TIMES the $1 million par value DIVIDED by 2), and only the par value of $1 million at maturity. When you subtract the effective annual premium (+$20,000) from the annual interest payments ($100,000), this gives the investor a net effective annual yield to call of 8%($80,000 total annual income DIVIDED by $1 million par = 8%). In this case, the yield to call is less than the yield to maturity of 9%. If the bond is purchased at par and the call is exercised, the effective yield does not change. There is no amortization of a premium or discount. The annual net income figure is the same whether the bond is called or if it remains outstanding until maturity. One last note on evaluating callable bonds, no one can predict whether or not a particular bond will be called in the future. The best advice to follow is to evaluate a callable bond’s yield under all possible scenarios, both on yield to each call date and the yield to maturity. Headquarters – 100 Motor Parkway, 2nd Floor, Hauppauge, New York 11788-5157 Tel: 631-979-0097 Toll Free: 800-645-5424 Toll Free Branches: 800-551-2971 Fax: 631-979-0448 Website: www.1empire.com The information contained herein was obtained from sources we believe to be reliable. However, we do not guarantee it is accurate or complete. This information is for educational purposes only. This information is not and should not be construed as a offer or solicitation to buy or sell any security or securities. First Empire Securities, Inc. Member NASD/SIPC. Member NASD/SIPC SETTLEMENT The delivery of a bond by the seller and the payment for the bond is referred to as “settlement”. US Government and US Agency Securities trading in the secondary market settle the next business day after the “trade date” (the deal is negotiated today and consummated tomorrow). Most other bonds settle three business days after the “trade date” (the deal is negotiated today and consummated in three days). The exception is new issue securities. When a new bond is being issued, settlement might not occur for up to 120 days after the trade date. Regardless of when settlement occurs, the terms of the sale are agreed upon by both parties (on the trade date), the price, yield, dollar amount due, and settlement date will not change. ACCRUED INTEREST Bonds pay interest at the coupon rate on a set schedule from issuance through maturity. The interest cycle can be monthly, quarterly, semi-annually or at maturity. When the bond is sold in the secondary market, it is uncommon for the settlement date to take place exactly on an interest payment date (semi-annual example: there are two interest payments per year). At settlement, the buyer pays the seller the purchase price PLUS interest earned (“accrued”) by the seller from the last interest payment, up to, but not including the settlement date. This is referred to as the “accrued interest”. For example: 1)PRICE = 100.00% (“par”) PAR VALUE = $1,000,000 TERM TO MATURITY = 10 years COUPON = 10.00% EFFECTIVE YIELD TO MATURITY = 10.00% INTEREST PAYMENTS = January 1 and July 1 (semi-annual) TRADE DATE = March 25 SETTLEMENT DATE = April 1 PRINCIPAL DUE = $1,000,000 ($1 million par value TIMES the price of 100.00%) ACCRUED INTEREST DUE = $25,000 (The interest the seller has earned from January1st – the last interest payment date – through the settlement date of April 1st). TOTAL DUE AT SETTLEMENT = $1,025,000.00 The mathematical formula to calculate the accrued interest due is: Par Value TIMES Coupon Rate DIVIDED by 360 (or 365 depending on the bond) TIMES # days from the last interest payment = Accrued interest The accrued interest paid at settlement will be “refunded” to the buyers as part of the interest payment on the next interest pay date. To use our above example on July 1st, the buyer will receive a full six months ($50,000) of interest. This is the three months accrued interest ($25,000) originally paid out at settlement and the 3 months earned income ($25,000) for the time the investor owned the bond (April 1st through July 1st). Headquarters – 100 Motor Parkway, 2nd Floor, Hauppauge, New York 11788-5157 Tel: 631-979-0097 Toll Free: 800-645-5424 Toll Free Branches: 800-551-2971 Fax: 631-979-0448 Website: www.1empire.com The information contained herein was obtained from sources we believe to be reliable. However, we do not guarantee it is accurate or complete. This information is for educational purposes only. This information is not and should not be construed as a offer or solicitation to buy or sell any security or securities. First Empire Securities, Inc. Member NASD/SIPC.