First Data Corporation - University of Connecticut

advertisement

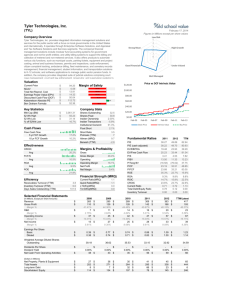

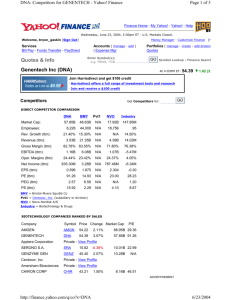

First Data Corporation Executive Summary First Data Corporation operates in four business segments: payment services, merchant services, card issuing services and emerging payments. Payment services primarily consist of Western Union, Integrated Payment Systems, Orlandi Valuta and ValueLink companies. Merchant services is comprised of First Data Merchant Services, TeleCheck, NYCE Corporation, TASQ Technologies, Inc. and First Data Financial Services. Card issuing services segment includes First Data Resources, First Data Europe, First Data Solutions and PaySys International, Inc. The emerging payments segment consists of eONE Global. The remainders of the Company’s business units are grouped in the All Other and Corporate category, which includes Teleservices, Call Interactive, Achex, Inc. and Corporate operations. From the following valuations and research we have conclude we have decided to buy First Data. Precise buy order information can be viewed on the following page. UConn Foundation Student Managed Fund Trade Form Presentation Date: 03/05/03 Covering managers: Scott Bores Anticipated date for trade: 03/06/03 Stock Name: First Data Corp. Ticker: FDC Decision: Buy Number of shares: approximately 118 shares Approximate cash value: $4000 Limits: Stop Loss: at $26.00 or 20 % of current price Appreciation review price target: $38.70 Vote results for: 11 against: 0 Abstain: Trade executed by: Professor Ghosh Trade manager present: University of Connecticut Student Managed Fund Stock Analysis Report University of Connecticut - Student Managed Fund Stock Analysis Report March 7, 2003 First Data Corporation - NYSE (FDC) Large Cap: $26.0 billion Industry: Industrial Sector: Conglomerates Valueline: Timeliness: 2 Safety: 2 Technical: 3 Stock Scouter Rating: 10 Business Summary First Data Corporation (FDC) operates in four business segments: payment services, merchant services, card issuing services and emerging payments. Payment services primarily consist of Western Union, Integrated Payment Systems, Orlandi Valuta and ValueLink companies. Merchant services is comprised of First Data Merchant Services (FDMS), TeleCheck, NYCE Corporation, TASQ Technologies, Inc. (TASQ) and First Data Financial Services (FDFS). Card issuing services segment includes First Data Resources (FDR), First Data Europe (FDE), First Data Solutions (FDS) and PaySys International, Inc. (PaySys). The emerging payments segment consists of eONE Global. The remainder of the Company's business units are grouped in the All Other and Corporate category, which includes Teleservices, Call Interactive, Achex, Inc. and Corporate operations. In June 2002, the Company acquired E Commerce Group, Inc. (ECG), an electronic bill payment and presentment company based in New York. ECG will operate as a part of the Western Union family of businesses. Payment Services This segment is a provider of non-bank money transfer and payment services to consumers and commercial entities, including money transfer, official check and money order. Western Union utilizes an agent network of over 50,900 agent locations in North America (United States, Canada and Mexico) and 68,800 international agent locations to provide money transfer services to consumers in 186 countries and territories. Through Western Union's Easy Pay and Quick Collect services, FDC also offers bill payment services to utility companies, collection agencies, finance companies and other institutions. Money transfer transactions totaled 108.8 million in 2001, compared to 88.9 million in 2000 and 73.5 million in 1999. ValueLink develops, implements and manages pre-paid stored-value gift card programs with brick and mortar, Internet, business-tobusiness and international applications for more than 100 major national retail, restaurant and grocery brands. Payment services revenue comprised 42% of FDC's total revenues in 2001. In the payment services segment, Western Union signed agreements with 7-Eleven, RiteAid and Publix. These agreements, signed in 2001, are expected to add approximately 30,000 new agent locations by the end of 2003. In addition, Western Union and Orlandi Valuta signed agreements with Banco Nacional de México, S.A. (Banamex CitiGroup), in 2001, for Banamex CitiGroup to become an agent in Mexico for consumer money transfers. In April 2002, the Company acquired Paymap Inc., a San Francisco-based financial services company offering proprietary electronic payment services to financial institutions. Paymap will become part of First Data's Western Union Financial Services subsidiary. In January 2001, Western Union acquired Bidpay.com, Inc., a provider of Web-based payment services to online auction markets. In December 2001, the Company acquired Gift Card Services, Inc., a provider of gift card solutions that complements its storedvalue business, ValueLink. Merchant Services This segment provides merchants with credit and debit card transaction processing services, including authorization, transaction capture, settlement, Internet-based transaction processing, check verification and guarantee services. This segment also provides processing services to debit card issuers and operates an automated teller machine (ATM). FDMS provides such services as authorization, transaction capture, settlement, chargeback handling and Internet-based transaction processing. TeleCheck, a check acceptance company, provides electronic check conversion, check guarantee, check verification and collections services. NYCE operates an ATM network. It provides online debit point-of-sale (POS) services and real-time payment solutions such as ATM management and monitoring services, and debit card issuance and authorization solutions. TASQ is an outsource provider of credit, debit, ATM, check, Internet and smart card technology. FDFS provides credit card, debit card and money transfer services to gaming establishments and their customers. The percentage of FDC's revenues from this segment's services was 35% during the year ended December 31, 2001. In the merchant services segment, the Company acquired the remaining 50% ownership interest in Cardservice International in December 2001. In August 2001, the Company acquired a 64% interest in NYCE, Inc., which services 48 million debit cardholders through 44,000 ATMs and 270,000 POS locations. Merchant services formed an alliance with Deutsche Postbank, a subsidiary of the German postal service, in June 2001. Also, in March 2001, the Company acquired a majority interest in TASQ, which will complement First Data FDMS' POS deployment operations. Card Issuing Services The card issuing services segment provides a comprehensive line of processing and related services to financial institutions issuing credit and debit cards, and to issuers of oil and private-label credit cards. FDR and FDE provide a comprehensive line of products and processing and related services to financial institutions issuing Visa and MasterCard credit cards, debit cards and oil company and retail store credit cards. FDS is a provider of consumer and business solutions in the areas of risk and fraud management and information verification associated with granting of credit, collecting debt and customer service. PaySys is a global provider of credit card transaction processing software to banks, retailers and third-party processors. Collectively, this segment's services constituted 23% of the Company's total revenues in 2001. In the card issuing services segment, the Company announced an agreement to process more than three million cardholder accounts that JP Morgan Chase acquired from Providian Master Trust in January 2002. In addition, the Company announced that it has signed a new multi-year contract with Citi Commerce Solutions, Citibank Cards' privatelabel credit card division. In April 2001, card issuing services acquired PaySys, which provides card processing software. Also, in March 2001, card issuing services entered into a joint venture and formed Nihon Card Processing Co., Ltd., the first company in Japan to provide thirdparty credit card processing services. Emerging Payments The Company holds over 70% of the outstanding equity in eONE Global. eONE Global is comprised of govONE Solutions, which provides electronic tax processing services to banks and governmental agencies, and other developmental companies focused on business-to-business e-procurement solutions, including the August 2001 acquisition of Taxware, a provider of worldwide commercial tax compliance systems, and the addition of Encorus Technologies, in November 2001, which is a provider of mobile payment products. In the emerging payments segment, eONE Global acquired Brokat A.G.'s mobile commerce business unit in November 2001. eONE Global also announced alliances with Verisign and IBM during 2001. In March 2001, eONE Global launched govONE Solutions, combining CashTax with the acquired transaction processing business of govWorks to augment payment solutions for local, state and federal governmental entities. In August 2001, the Company acquired the assets of Taxware International, Inc., a provider of worldwide commercial tax compliance systems. Financial Data/ Ratio Comparison Over the last five years, First Data has seen their revenues grow at an average of 10%. At the same time, earning per share has risen 17.1% on average, and their cash flow has grown at 14.3% on average, but both have also decreased in prior periods. The has also been growth in both return on equity and return on invested capital after the boom of 1999, both are expected to be over 10% for the current year. Their dividend has continued to constantly grow, and is currently paying $0.06/year, and is expected to increase at the end of the year. They have managed to see increased growth even in a time when the economy is struggling and their customers are buying less. Ratio Comparison: For these ratios, First Data was compared to the S&P 500, the industry, and one of their competitors, Ceridian Corp. Valuation Ratios P/E Ratio (TTM) P/E High - Last 5 Yrs. P/E Low - Last 5 Yrs. Beta Price to Sales (TTM) Price to Book (MRQ) FDC CEN Industry S&P 500 21.34* 22.37* 22.14 22.04 46.32 130.33 56.87 49.83 13.33 16.55 14.65 16.32 1.16 0.72 1.86 1 3.50* 1.75* 2.99 2.84 6.63 1.73 3.64 4.16 Price to Tangible Book (MRQ) Price to Cash Flow (TTM) NM 23.47 9.51 6.55 14.73 12.27 18.1 16.31 Price to Free Cash Flow (TTM) 23.3 15.4 22.4 25.28 88.55 93.15 43.56 61.22 % Owned Institutions Dividends Dividend Yield FDC CEN Industry S&P 500 0.23 NA 3.32 2.3 0.2 0 0.12 1.31 Dividend 5 Year Growth Rate 4.24 NM 8.11 -11.03 Payout Ratio (TTM) 2.43 0 8.78 26.07 Dividend Yield - 5 Year Avg. Growth Rates(%) Sales (MRQ) vs Qtr. 1 Yr. Ago FDC 33.62* CEN 6.21* Industry 21.79 S&P 500 8.84 Sales (TTM) vs TTM 1 Yr. Ago Sales - 5 Yr. Growth Rate EPS (MRQ) vs Qtr. 1 Yr. Ago EPS (TTM) vs TTM 1 Yr. Ago EPS - 5 Yr. Growth Rate Capital Spending 5 Yr. Growth Rate Financial Strength 18.38* 0.88* 14.71 4.97 5.49 4.64 37.01 10.56 30.08* 24.18* 15.67 25.05 47.37* 87.54* 34.44 23.72 9.97 -15.15 19.53 9.68 -11.42 3.07 15.59 -13.81 FDC Quick Ratio (MRQ) Current Ratio (MRQ) LT Debt to Equity (MRQ) Total Debt to Equity (MRQ) Interest Coverage (TTM) Profitability Ratios (%) Gross Margin (TTM) Gross Margin - 5 Yr. Avg. CEN Industry S&P 500 NM 1.39 1.48 1.15 NM 1.52 1.74 1.67 0.8 0.16 0.42 0.74 0.8 0.16 0.5 0.97 15.65 18.72 -3.01 11.1 FDC CEN Industry S&P 500 42.08 52.01 42.83 47.48 37.92 51.26 42.87 47.78 EBITD Margin (TTM) 33.39 19.42 -9.88 19.44 EBITD - 5 Yr. Avg. 33.16 15.55 12.32 21.82 Operating Margin (TTM) 23.99 12.43 -15.81 17.93 Operating Margin 5 Yr. Avg. 20.52 8.64 4.48 18.21 Pre-Tax Margin (TTM) 23.99 11.94 13.18 16.02 Pre-Tax Margin - 5 Yr. Avg. 20.52 7.47 12.27 17.35 Net Profit Margin (TTM) 16.22* 7.86* 8.82 10.98 Net Profit Margin 5 Yr. Avg. 13.56 7.29 5.99 11.39 Effective Tax Rate (TTM) 25.46 37.45 29.51 31.39 Effective Tax Rate - 5 Yr. Avg. 35.02 35.56 32.74 35.5 Management Effectiveness (%) Return On Assets (TTM) Return On Assets 5 Yr. Avg. Return On Investment (TTM) Return On Investment - 5 Yr. Avg. Return On Equity (TTM) Return On Equity 5 Yr. Avg. Efficiency Revenue/Employee (TTM) Net Income/Employee (TTM) Receivable Turnover (TTM) Inventory Turnover (TTM) Asset Turnover (TTM) CHART: FDC CEN Industry S&P 500 5.40* 2.14* -2.92 6.27 4.47 4.55 2.81 7.67 18.37* 2.39* 0.29 10.19 13.73 6.62 6.4 12.32 33.36* 8.37* -1.58 18.3 20.41 11.23 12.7 21.29 FDC CEN Industry S&P 500 263,317* 136,668* 278,615 486,486 42,697* 10,737* 25,600 74,468 6.64* 2.64* 6.92 9.67 NA NA 21.12 11.06 0.33* 0.27* 0.64 0.95 Recent News: February 20, 2003 First Data Expecting More Growth in Merchant Biz First Data Corp.'s merchant processing business is doing better than expected this quarter, the company's chairman and chief executive officer said Tuesday. Unlike its credit card processing business, whose profits have been flat for the past year, the merchant business is expected to continue to grow, aided by consumers' steadily increasing appetite for buying with credit and debit cards. Charles T. Fote, the chairman and CEO, predicted that by 2010 more than half of all transactions at the point of sale will be processed electronically, up from around 32% last year. Contributing to that growth will be new places where cards will be accepted, like gas stations and quick-serve restaurants, he said. Debit cards will help fuel the growth in card usage, Mr. Fote said at an investor conference in Chicago that focused on First Data's merchant business. "Up to now consumers have not had the option Another strength of First Data is that, instead of specializing in one business segment, it handles all types of merchants, he said. "We can ride winners and manage those with slower growth. We enjoy what national players give us, and we use them to build stronger relationships in the smaller merchant base." Growth prospects for the next few years include selling point of sale terminals that can do more things -- accept loyalty and gift cards, for example -- and getting credit cards accepted at more places, Mr. Fote said. Scott H. Betts, the president of the merchant services division, said it will concentrate on buying smaller merchantacquirers and promoting itself through its merchant/bank alliances, which bring in more stable clients. "Attrition varies significantly by channel and the type of merchant," Mr. Betts said. "One thing I am struck by is the figure when the merchant has a deposit account at the bank. It lowers attrition 20% and is an opportunity for us to leverage bank relationships to reduce attrition levels." Among the First Data executives he introduced was Diane Vogt, who will focus on quick-service restaurants and gasoline stations, two areas where he expects to see growth. Mr. Betts also said that First Data dominated Internet card transactions -- 70% of them go through the company at some point. He said the merchant processing business would continue its approximately 17% annual profit growth, which he said would put it slight ahead of the industry's 15% rate. First Data plans to hold investor days for its other business segments in the coming months, and Mr. Fote was firm in making analysts stick to the topic of the day. When one asked a question about international growth, Mr. Fote deferred the question and asked the audience to wait for a meeting to be held in June in London to discuss that topic. Alan Gitles, the CEO of Landmark Merchant Solutions LLC, an independent sales organization in Schaumburg, Ill., attended the presentation and said he liked what he heard. "Their credibility is pretty high, because they generally deliver on what they promise," Mr. Gitles said. "They have a pretty good hand on the pulse of the business." Jeffrey B. Baker, a senior research analyst at the Minneapolis-based investment banking firm U.S. Bancorp Piper Jaffray, said the First Data division's "better-than-expected start" to the year is consistent with what he has seen at other merchant processors. Models: Risk Free Rate: S&P500 (10 year average return, rm): Beta: 3.628% 7.930% 1.10 1. DDM Model k=rf +β(rm-rf): 8.36 Earnings 1993: .39 Earnings 2002: 1.67 ge: (1.67/0.39)^(1/9)-1= 17.552 Average ROE: 18.025 (4 year average) Average Retention: 1-[(.188+.228+.276+.275)/4] = 75.29% gr: ROE*retention ration (b)=.17552 *.7529=13.22% Average g= (.1322+.03628)/2=8.42% 2). Multistage Growth Model Is not necessary since this is a mature company growth will continue to be steady. 3). No Growth Po = Eo/k = 1.90/0.0836 = $22.73 4) P/E Model Avg P/E ratio 20 Expected EPS (VLIS)= $1.90 5-Year Horizon: $2.75 P/E Ratio: 19.5 Projected high price for the next 5 years: $2.75* 19.5= $53.63 Lowest price in the last 3 years: $23.75 Current Price: $33.65 5. Valuepro.net Intrinsic Value Growth Rate Risk Free Rate WACC 100.46 17 3.628 8.00 6. SSG Model Historical Sales Sales Growth Used Historical EPS EPS 14.6% 7.6% 12.5% 9.8% Recommendation: Buy Upside/Downside potential 7. Value line Model FDC: Long Term Debt + Shareholder Equity: 7,000 (million) Cash Flow Growth Estimate: 12% Common Shares Outstanding: 762 (million). Average Annual P/E Ratio: 20 Return on Total Capital: 18% The Future Price: 7000* 1.10^10 / 762 * .18 * 20 = $102.71 (Discount the future price at 15% for n=10) = $25.72 This means that we are overpaying for First Data now using conservative estimates, but the last few years have provided low returns but expectations point to large growth and an increasing share price. Ownership Structure Ownership Summary % Shares Owned: 86.80 Price Range Quarter: % Change in Ownership: 2.72 # New Buyers: # Institutions: 737 # Closed Positions: Total Shares Held: 652,966,311 3 Mo. Shares Purchased: 70,973,173 # Buyers: 3 Mo. Shares Sold: (53,661,587) # Sellers 3 Mo. Net Change: 17,311,586 # Net Buyers: $0 - $0 91 54 387 340 47 Top Institutional Holders Institution Name Shares Held Position Value % Shs. (000) Out. Portfolio Date FIDELITY MGMT & RESEARCH CO 60,455,923 $2,140,744.23 8.04% 12/31/2002 BARCLAYS GLOBAL INVESTORS INTL 28,791,926 $1,019,522.10 3.83% 12/31/2002 ALLIANCE CAPITAL MGMT 24,921,834 $882,482.14 3.31% 12/31/2002 STATE STREET GLOBAL ADVISORS 24,340,503 $861,897.21 3.24% 12/31/2002 WELLINGTON MGMT 20,703,646 $733,116.10 2.75% 12/31/2002 GOLDMAN SACHS ASSET MGMT 19,376,574 $686,124.49 2.58% 12/31/2002 GE ASSET MGMT 18,983,485 $672,205.20 2.52% 12/31/2002 T ROWE PRICE ASSOCIATES 18,384,327 $650,989.02 2.44% 12/31/2002 STEWART (WP) & CO 17,320,559 $613,320.99 2.30% 12/31/2002 VANGUARD GROUP 13,693,921 $484,901.74 1.82% 12/31/2002 MFS INVESTMENT MGMT 12,179,864 $431,288.98 1.62% 12/31/2002 AIM CAPITAL MGMT (HOUSTON) 11,844,211 $419,403.51 1.58% 12/31/2002 HARRIS ASSOCIATES 11,773,684 $416,906.15 1.57% 12/31/2002 PEREGRINE CAPITAL MGMT 9,758,195 $345,537.69 1.30% 12/31/2002 EATON VANCE MGMT 9,157,120 $324,253.62 1.22% 12/31/2002