Chapter 13

advertisement

CHAPTER 13

CASHFLOWS IN CAPITAL BUDGETING

CASH FLOW ESTIMATION

IN VALUING A CAPITAL PROJECT WE NEED TO KNOW THE AFTER-TAX

CASH FLOWS ASSOCIATED WITH THE PROJECT.

THESE ARE USUALLY

FORECASTS BASED ON REVENUE AND COST PROJECTIONS.

TO BE MEANINGFUL, CASH FLOWS

1. MUST BE AFTER TAX

2. MUST BE INCREMENTAL

3. MUST NOT INCLUDE SUNK COSTS

4. MUST INCLUDE OPPORTUNITY COSTS

THAT IS, THEY MUST BE RELEVANT, INCREMENTAL AFTER-TAX CASH

FLOWS.

IT IS EASY TO CLASSIFY CASH FLOWS AS:

1. INITIAL INVESTMENT

2. NET OPERATING CASH FLOWS

3. TERMINATION OR END-OF-PROJECT CASH FLOWS

INITIAL INVESTMENT (I0 0R CF0)

ALL NORMAL PROJECTS REQUIRE INITIAL INVESTMENT IN FIXED

ASSETS AND WORKING CAPITAL.

IT IS COMPUTED AS FOLLOWS:

INITIAL INVESTMENT I0 =

PRICE OF ASSET

+ MODIFICATION COSTS

+ SHIPPING & INSTALLATION COSTS

+ LEGAL COSTS ETC.

+ INCREASE IN NET WORKING CAPITAL

OF THESE COST, INCREASE IN NET WORKING CAPITAL IS NOT

DEPRECIABLE.

IT IS ASSUMED TO BE RECOVERED, FULLY OR

PARTIALLY, DEPENDING ON THE NATURE OF WORKING CAPITAL, AT

THE END OF THE PROJECT.

NET OPERATING CASH FLOWS (NOCF)

ONCE A PROJECT IS IMPLEMENTED, IT IS EXPECTED TO BRING IN

CASH FLOWS AFTER TAX.

FLOWS.

THESE ARE THE NET OPERATING CASH

THEY WILL OCCUR IN EACH OF THE PRODUCTIVE YEARS OF

THE PROJECT.

∆NOCFt = [∆Rt - ∆Ct)*(1-T) + (∆DEPRECIATION

WHICH IS THE SAME AS

∆NET OPERATING INCOMEt + ∆DEPRECIATIONt

t

* T)

TERMINATION CASH FLOWS

(TCF)

THESE CASH FLOWS OCCUR IN THE LAST YEAR (PERIOD) OF A

PROJECT WHEN IT IS TERMINATED OR ENDED.

THESE CASH FLOWS

WOULD ARISE FROM THE AFTER-TAX SALVAGE VALUE OF THE

PROJECT’S ASSETS, OTHER AFTER-TAX CASH FLOWS ASSOCIATED

WITH A PROJECT’S TERMINATION (E.G. CLEAN UP COSTS) AND ANY

RECOVERY OF INVESTMENT IN NET WORKING CAPITAL MADE AT TIME

0.

THESE CASH FLOWS CAN BE REPRESENTED ON A TIME LINE AS

FOLLOWS:

TCFn

NOCF1

NOCF2

NOCF3…..........NOCFt...........NOCFn

__________________________________________________________

0

1

2

3 ........... t ............ n

-CF0

ONCE THE CASH FLOWS HAVE BEEN ESTIMATED, THE PROJECT CAN BE

EVALUATED USING ANY OF THE TECHNIQUES STUDIED EARLIER.

INDEPENDENT PROJECT (PROBLEM 13-5)

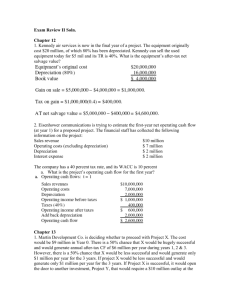

a. The net cost is $89,000:

Price

Modification

Change in NWC

($70,000)

(15,000)

(4,000)

($89,000)

b. The operating cash flows follow:

After-tax savings

Depreciation shield

Net cash flow

Year 1

Year 2

Year 3

$15,000

11,220

$26,220

$15,000

15,300

$30,300

$15,000

5,100

$20,100

Notes:

1. The after-tax cost savings is $25,000(1 – T) =

$25,000(0.6)= $15,000.

2. The depreciation expense in each year is the

depreciable basis, $85,000, times the MACRS

allowance percentage of 0.33, 0.45, and 0.15 for

Years 1, 2 and 3, respectively.

Depreciation

expense in Years 1, 2, and 3 is $28,050, $38,250,

and

$12,750.

The

depreciation

shield

is

calculated as the tax rate (40%) times the

depreciation expense in each year.

c. The additional end-of-project cash flow is $24,380:

Salvage value

Tax on SV*

Return of NWC

$30,000

(9,620)

4,000

$24,380

*Tax on SV = ($30,000 - $5,950)(0.4) = $9,620.

Note that the remaining BV in Year 4 = $85,000(0.07)

= $5,950.

d. The project has an NPV of -$6,705.

not be accepted.

Year

0

1

2

3

Net Cash Flow

($89,000)

26,220

30,300

44,480

Thus, it should

PV @ 10%

($89,000)

23,836

25,041

33,418

NPV = ($ 6,705)

Alternatively, with a financial calculator, input

the following:

CF0 = -89000, CF1 = 26220, CF2 =

30300, CF3 = 44480, and I = 10 to solve for NPV = $6,703.83.

REPLACEMENT ANALYSIS

THE DURST EQUIPMENT COMPANY PURCHASED A MACHINE 5 YEARS AGO

AT A COST OF $100,000.

IT HAD AN EXPECTED LIFE OF 10 YEARS

AT THE TIME OF PURCHASE AND AN EXPECTED SALVAGE VALUE OF

$10,000 AT THE END OF THE 10 YEARS.

IT IS BEING

DEPRECIATED BY THE STRAIGHT LINE METHOD TOWARD A SALVAGE

VALUE OF $10,000, OR BY $9,000 PER YEAR.

A NEW MACHINE CAN BE PURCHASED FOR $150,000, INCLUDING

INSTALLATION COSTS.

OVER ITS 5-YEAR LIFE, IT WILL REDUCE

CASH OPERATING EXPENSES BY $50,000 PER YEAR.

EXPECTED TO CHANGE.

SALES ARE NOT

AT THE END OF ITS USEFUL LIFE, THE

MACHINE IS ESTIMATED TO BE WORTHLESS.

MACRS DEPRECIATION

WILL BE USED, AND IT WILL BE DEPRECIATED OVER A 3-YEAR

RECOVERY PERIOD RATHER THAN ITS 5-YEAR ECONOMIC LIFE.

THE OLD MACHINE CAN BE SOLD TODAY FOR $65,000.

FIRM’S TAX RATE IS 34 PERCENT.

THE

THE APPROPRIATE DISCOUNT

RATE IS 15 PERCENT.

a. IF THE NEW MACHINE IS PURCHASED, WHAT IS THE AMOUNT OF

THE INITIAL CASH FLOW AT YEAR 0?

b. WHAT INCREMENTAL OPERATION CASH FLOWS WILL OCCUR AT

THE END OF YEARS 1 THOUGH 5 AS A RESULT OF REPLACING

THE OLD MACHINE?

c. WHAT INCREMENTAL NONOPERATING CASH FLOW WILL OCCUR AT

THE END OF YEAR 5 IF THE NEW MACHINE IS PURCHASED?

d. WHAT IS THE NPV OF THIS PROJECT? SHOULD THE FIRM

REPLACE THE OLD MACHINE?

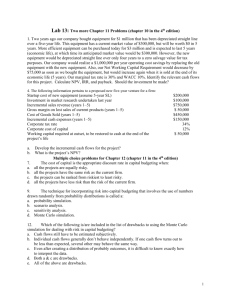

SOLUTION TO REPLACEMENT ANALYSIS PROBLEM DISCUSSED IN

CLASS

THE OLD MACHINE WAS ACQUIRED 5 YEARS AGO FOR $100,000, HAD AN

ESTIMATED SALVAGE VALUE OF $10,000 AND AN ESTIMATED USEFUL

LIFE OF 10 YEARS. IT IS DEPRECIATED ON A STRAIGHT LINE BASIS TO

EXPECTED SALVAGE VALUE of $10,000

OLD DEPRECIATION = (100000-10000)/10 = $9000/YEAR

BOOK VALUE NOW = 100000-(5*9000) = $ 55000

OLD MACHINE CAN BE CURRENTLY SOLD FOR $65000

GAIN = $65000 – 55000 = $10000

TAX ON GAIN = 10000* .34 = $3400

INCREMENTAL AFTER-TAX INITIAL INVESTMENT, I.E.,

(INCREMENTAL AFTER-TAX CASH FLOW AT TIME 0) :

PRICE NEW MACHINE

SALE OF OLD MACHINE (BEFORE-TAX)

TAX ON SALE OF OLD MACHINE

INCREMENTAL AFTER-TAX CASH FLOW

AT TIME 0

= ($150,000)

= $ 65,000

= ($3,400)

= ($ 88,400)

TO DETERMINE THE INCREMENTAL AFTER-TAX NET OPERATING CASH

FLOWS DUE TO REPLACEMENT, WE NEED TO DETERMINE THE

INCREMENTAL DEPRECIATION AND TAX SHELTER.

YEAR MACRS

DEPRECIABLE DEPRECIATION DEPRECIATION

CHANGE

RECOVERY BASIS ON NEW ON NEW

ON OLD

%

MACHINE

MACHINE

MACHINE

1

33

$150,000

$49,500

$9,000

$40,500

2

45

150,000

67,500

9,000

58,500

3

15

150,000

22,500

9,000

13,500

4

7

150,000

10,500

9,000

1,500

9,000

(9,000)

5

INCREMENTAL AFTER-TAX NET OPERATING CASH FLOWS

Δ NOCFt = (Δ Rt – Δ Ct ) * (1-TAX RATE) + Δ DEPRECIATIONt * TAX RATE

REPLACEMENT WILL HAVE NO IMPACT ON SALES & REVENUE

OPERATING COSTS WILL BE REDUCED BY $50,000 BEFORE TAX EACH

YEAR

YEAR (Δ Rt – Δ Ct )*( 1-TAX RATE) +(Δ DEPRECIATION *TAX RATE) = Δ

NOCFt

1

2

3

4

5

50,000 * .66 = 33,000

50,000 * .66 = 33,000

50,000 * .66 = 33,000

50,000 * .66 = 33,000

50,000 * .66 = 33,000

+

+

+

+

+

40,500*.34 = 13,770

58,500*.34 = 19,890

13,500 * .34 = 4,590

1,500 *.34 = 510

(9,000) * .34 = (3,060)

= 46,770

= 52,890

= 37,590

= 33,510

= 29,940

INCREMENTAL AFTER-TAX TERMINATIONCASH FLOWS

SALVAGE VALUE ON NEW MACHINE NET OF TAX

SALVAGE VALUE ON OLD MACHINE NET OF TAX

(OPPORTUNITY COST)

INCREMENTAL AFTER-TAX TERMINATION CASH FLOW

=0

= (10,000)

= (10,000)

SUMMARY OF INCREMENTAL AFTER-TAX CASH FLOWS

YEAR

AFTER-TAX CASH FLOW

0

1

2

3

4

5

(88,400)

46,770

52,890

37,590

33,510

29,940 + (10,000) = 19,940

NPV @ 15% = $46,051

SINCE INCREMENTAL NPV > 0, THE FIRM SHOULD REPLACE THE OLD

MACHINE

RISK IN CAPITAL BUDGETING

THE CONCEPTS OF RISK AND RETURN DEVELOPED IN CHAPTERS 2 & 3

CAN BE APPLIED IN THE CONTEXT OF CAPITAL BUDGETING.

THE

DIFFERENT TYPES OF RISK IN CAPITAL BUDGETING CAN BE

DESCRIBED AS FOLLOWS:

STAND ALONE RISK

THIS IS THE RISK OF A PROJECT IF HELD

ISOLATION.

THIS IS SIMILAR TO TOTAL

RISK AND, THEREFORE, INCLUDES A

PROJECT’S SYSTEMATIC AND UNSYSTEMATIC

RISK.

CORPORATE RISK

THIS IS THE RISK A PROJECT CONTRIBUTES

TO THE FIRM AND WOULD DEPEND VERY MUCH

ON THE CORRELATION BETWEEN THE PROJECT

AND THE FIRM’S PORTFOLIO OF OTHER

PROJECTS.

OBVIOUSLY, IT WILL INCLUDE

THE PROJECT’S SYSTEMATIC RISK AND SOME

UNSYSTEMATIC RISK DEPENDING ON

PROJECT’S CORRELATION WITH THE FIRM.

MARKET RISK

THIS IS THE RISK OF A PROJECT IN THE

CONTEXT OF A LARGE, WELL-DIVERSIFIED

PORTFOLIO (MARKET PORTFOLIO).

THIS IS

THE SYSTEMATIC RISK OF THE PROJECT AND

CAN BE MEASURED BY THE PROJECT’S BETA.

PURE PLAY METHOD

PURE PLAY METHOD IS USED TO ESTIMATE A PROJECT’S BETA.

THE

FOLLOWING MAJOR STEPS ARE INVOLVED:

1. IDENTIFY ONE OR MORE PURE PLAYS (COMPANY OR DIVISION)

IN A LINE OF BUSINESS SAME AS THE PROPOSED PROJECT.

2. ESTIMATE THE BETA, MOST LIKELY, THE LEVERAGED BETA,

CAPITAL STRUCTURE AND MARGINAL TAX RATE OF THE PURE

PLAY (AVERAGE BETA, CAPITAL STRUCTURE AND MARGINAL TAX

RATE, IF MORE THAN ONE PURE PLAY).

3. APPLY HAMADA MODEL TO BETA TO ESTIMATE THE UNLEVERED

(BUSINESS RISK) BETA:

ΒU = βL/[1+{(1-T)* D/S}]

WHERE ΒU, βL, D/S, AND T ARE, RESPECTIVELY, THE

UNLEVERED BETA, LEVERED BETA, CAPITAL STRUCTURE, AND

MARGINAL TAX RATE OF THE PURE PLAY ESTIMATED IN STEP 2.

4. ESTIMATE THE MARGINAL TAX RATE AND CAPITAL STRUCTURE

OF THE FIRM EVALUATING THE PROJECT.

5. FIND THE PROJECT’S LEVERED BETA FOR THIS FIRM BY

APPLYING HAMADA MODEL:

βL = βU

*

[1+{(1-T)* D/S}]

WHERE βU , D/S, AND T ARE, RESPECTIVELY, THE

UNLEVERED BETA IN STEP 3, AND CAPITAL STRUCTURE AND

MARGINAL TAX RATE IN STEP 4.

6. APPLY CAPM TO FIND THE

COST OF EQUITY FINANCING, KS,

FOR THE PROJECT:

KS = KRF + βL * [KM – KRF]

WHERE KRF AND KS ARE, RESPECTIVELY, THE RISK-FREE AND

MARKET PORTFOLIO RETURNS AND βL IS FROM STEP 5.

7. ESTIMATE THE BEFORE-TAX COST OF DEBT Kd FOR THE

PROJECT.

8. ESTIMATE THE PROJECT’S WEIGHTED AVERAGE COST OF

CAPITAL (WACC)

WACC = wd * Kd * (1-T) + ws * KS

WHERE wd AND ws ARE THE PROPORTIONS OF DEBT AND EQUITY

IN THE PROJECT’S MARGINAL CAPITAL STRUCTURE, T, THE

PROJECT’S MARGINAL TAX RATE (FROM STEP 4)

9. USE WACC IN STEP 8 TO EVALUATE THE PROJECT USING NPV

OR IRR.

PURE PLAY APPROACH

Williams Company has a target capital structure of 40

percent debt and 60 percent equity, and it will apply

this structure to the project under consideration.

The

firm’s beta, which is an average of five estimates by

financial service firms, is 1.5.

Williams is evaluating

a new project which is totally unrelated to its existing

line of business.

However, it has identified two proxy

firms exclusively engaged in this business line.

They,

on average have a beta of 1.2 and a debt ratio of 50

percent.

Williams’s new project has an estimated IRR of

13.5 percent.

The risk-free rate is 10 percent, and the

market risk premium is 5 percent.

marginal tax rate of 34 percent.

All three firms have a

Williams’s before-tax

cost of debt is 14 percent.

a. What is the project’s unlevered beta, bu?

b. What is the beta of the project if undertaken by

Williams?

c. Should the firm accept the project?

PURE PLAY METHOD PROBLEM SOLUTION

a.

ΒU = βL/[1+{(1-T)* D/S}]

=

=

=

=

b.

c.

d.

1.2/ [1+ {(1-.34)* (.5/.5)}]

1.2/[1+ {(.66*1)}]

1.2/1.66

0.72

βL = βU * [1+{(1-T)* D/S}]

= 0.72* [1+{(1-.34)*(.4/.6)}]

= 0.72* [1+ (.66*.67)]

= 0.72 * 1.44

= 1.04

kSL = kRF + βL * [kM - kRF]

= 10 + (1.04 * 5)

= 15.2%

WACC = [wd * kd * (1-T)] + [ws * kSL]

= [0.4*14*.66]+ [0.6*15.2]

= 12.81%

SINCE IRR=13.5% > WACC=12.81%, ACCEPT THE

PROJECT

WHAT CAN GO WRONG? WILLIAMS COMPANY’S BETA=1.5 IF

THIS BETA WERE TO BE USED (ERRONEOUSLY) AS THE

PROJECT’S BETA, kSL = kRF + βL * [kM - kRF]

= 10 + (1.54 * 5)

= 17.5%

WACC = [wd * kd * (1-T)] + [ws * kSL]

= [0.4*14*.66]+ [0.6*17.5]

= 14.2%

SINCE IRR=13.5% < WACC=14.2%,THE PROJECT WILL BE

REJECTED!