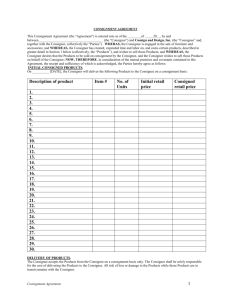

Consignment Accounting

advertisement

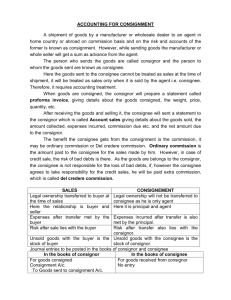

Chartered Accountancy CPT Course Session 1, Section A Fundamentals of Accounting Lecture 12 – Consignment Accounting 1 Points to be kept in mind Consignor remains the owner of goods even after sending to consignee. Consignor does not send any Invoice rather a Performa invoice. The Amount of Sales belongs to Consignor. All the exp. are to be borne by Consignor. If borne by consignee, recoverable from consignor. Consignee entitled to Commission. Consignee entitled to de-credere commission if he is responsible for bad debts. Consignee sends a statement called Account Sales, periodically. 2 Important Terns & Concepts Transaction Goods sent on consignment Exp. Incurred by Consignor Exp. Incurred by Consignee For Sale done by Consignee Commission due to Consignee Amount received from Consignee For unsold goods on consignment Transferring profit on consignment Transferring goods sent on consignment to Trading A/c Accounting Entry Consignment to ___ A/c Dr. To Goods sent on consignment A/c Consignment to ___ A/c Dr. To Cash/Bank A/c Consignment to ___ A/c Dr. To Consignee Consignee Dr. To Consignment to ___ A/c Consignment to ___ A/c Dr. To Consignee Cash/Bank A/c Dr. To Consignee Stock on Consignment A/c Dr. To Consignment to ___ A/c Consignment to ___ A/c Dr. To P. & L. A/c Goods sent on consignment A/c Dr. To Trading Account 3 Quick Revision Notes Important Concept 1. Valuation of Stock: Stock should be valued at cost or net realizable value whichever is lower. In case of consignment, cost means: Cost of Goods to Consignor + Exp. incurred till the goods reach the premises of the consignee 2. Goods invoiced above cost: If goods are booked at higher than cost, the effect of loading must be removed by additional entries. Additional Entries: 1. Goods sent on Consignment A/c Dr. To Consignment to ____ A/c (reversing loading in goods sent on consignment) 2. Consignment to _____ A/c Dr. To Stock Reserve A/c (reversing loading in value of closing stock) 3. Abnormal Loss: 1. Find out the cost of the goods lost 2. Pass the entry: P. & L. A/c Dr. To Consignment to ______ A/c 4. Normal Loss: Spread over the entire consignment Cost per unit = Total Cost + Expenses incurred / Qty available after normal loss 5. Return of Goods from the consignee: Goods valued at the price at which it was consigned to consignee Exp. incurred by the consignee to send those goods back to consignor are not taken into consideration. 4 Accounting Entries – In the books of consignee Ignore: 1. Entries for Goods sent on Consignment; 2. Exp. incurred by Consignor. Record: 1. Entries for advance sent by consignee to consignor; 2. Entries for making sales; 3. Exp. incurred by Consignee; 4. Earning Commission. © ICAI