6. Account Sale

advertisement

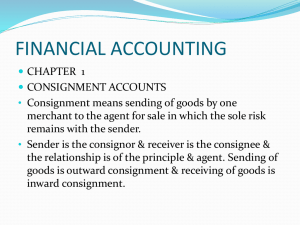

Chapter 2 Accounting For Consignment Learning Objectives • Define and explain the terms consignment, consignor and consignee. • What is the difference between consignment and sale? • Make journal entries in the books of consignor and that of consignee. • Prepare consignment account and consignee's account in the books of consignor. Consignment The word consignment can be generally defined as the act of sending a quantity of goods by the manufacturers or producers of one country or place to their agents in another at the risk of the principals for the purpose of sale. Goods so sent are known as "consignment". The sender of the goods is called the consignor. Generally the manufacturers or producers are consignors. The person to whom goods are forwarded for the purpose of sale is known as the consignee. Conti… 1. Goods sent on consignment do not become the property of the consignee. The ownership remains with the sender or the consigner. 2. If the goods are destroyed, the receiver (consignee) is not responsible. The loss will fall on the consignor. 3. The consignee tries to sell the goods according to the instructions of the consignor. 4. When the goods have been sold, consignee will deduct his expenses, commission, etc., from the sale proceeds and the balance is remitted to the consignor. Conti… 5. The relationship between the consignor and the consignee is that of principle and agent. 6. The consignee is entitled to his remuneration which is generally fixed on the basis of a commission of sales. 7. The expenses incurred by the consignee must also be reimbursed by the principal. Difference Between Consignment and Sale 1. Transfer of Legal Ownership of the Goods: In case of sale, the legal ownership of the goods sold is transferred to the purchaser of goods. Whereas in case of a consignment of goods , the legal ownership of the goods is not transferred to the consignment but the ownership of the goods remains with the consignor till the goods consigned are sold by the consignee. Conti… 2. Relationship Between Consignor and Consignee: In case of a sale of goods, the relationship between the seller and the purchaser of the goods is that of a creditor and a debtor whereas in case of a consignment the relationship between the consignor and the consignee is that of a principal and agent. because the consignee is to sell goods on behalf of the consignor. Conti… 3. Expenses Incurred: In consignment, expenses incurred by the consignee in connection with the goods consigned to him are usually borne by the consignor whereas in case of a sale, expenses incurred after sale of goods are born by the purchaser. 4. Risk Attached to the Goods: In case of consignment, risk attached to the goods sold lies with the consignor till the goods consigned are sold by the consignee. But in case of a sale, risk attached to the goods sold is transferred to the buyer of goods. Conti…. 5. Return of Goods: In case of consignment, return of goods is possible if the goods are not sold by the consignee. But in case of sale, return of goods is not possible as goods once sold are not returnable. 6. Requirement of Account Sale: In case of consignment, account sale is required to be submitted periodically by the consignee to the consignor. But in case of sales no account sale is required to be submitted by the purchaser to the seller Important Terms 1. Commission: The term commission as used in connection with consignment denotes the remuneration of the consignee for selling the goods of the consignor. This commission is generally calculated at a rate percentage on the gross proceeds of the sales. 2. Del Credere Commission: It is an extra commission allowed to the consignee on his guaranteeing the realization of the debts in full, in connection with the credit sale of goods on consignment. Conti… 3. Advance Against Consignment: Generally the consignor insist the consignee for some advance payment for the goods consigned at the time of delivery of goods. This advance payment is adjusted in full against the amount due by the consignee on account of the goods sold. 4. Consignment Account: The consignment account is one which shows what profit or loss is made out of the dealing of the goods sent on consignment. It is the combination of the trading and profit and loss account of any particular consignment. Conti… 5. Pro forma Invoice: When the consignor sends the goods to the consignee, he forwards a statement showing the particulars such as quantity, quality, price of goods etc. This statement is called the Pro forma invoice. 6. Account Sale: An account sale is a statement prepared and sent by the consignee to the consignor at periodical intervals, dealing there in the goods sold, price realized, expenses incurred, commission payable to and the net amount due from the consignee.