Registered Pension Plans

advertisement

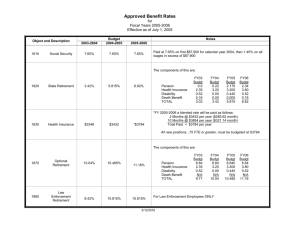

Group Retirement Solutions Registered Pension Plans A Registered Pension Plan (RPP) is a tax deferred savings vehicle that allows contributions to accumulate tax-free for later use as retirement income. What is a Registered Pension Plan (RPP)*? n A Registered Pension Plan provides the opportunity for individuals to save for retirement and gives employers a key component of a competitive compensation package. n RPPs are subject to applicable Federal and Provincial legislation, and must be registered with Canada Revenue Agency (CRA) and under pension benefits legislation maintained by all provinces. For more information, visit www.cra-arc.gc.ca. n Contributions made and fees paid by the plan sponsor reduce the amount of corporate income tax that the plan sponsor must pay. n Earnings in the plan will accumulate tax-free for the member until retirement. n The retirement income accumulated in a defined contribution pension plan depends on the amount of money contributed and the performance of the investment vehicles chosen by the member. *For the purposes of this document, only Defined Contribution pension plans are covered. Due to the preferred tax treatment this plan type receives, RPPs are subject to Federal and Provincial legislation. The chart below provides a description of some of the requirements of an RPP. Plan Details Description Eligibility Pension benefits legislation generally requires that all full-time employees must be allowed to join after two years of employment if they belong to the employee category for which the plan is established for. The plan sponsor can require mandatory participation in the plan. Contributions CRA mandates minimum plan sponsor required contributions of 1% of a member's earnings. The plan sponsor can require members to contribute. If plan provisions allow, the sponsor and members can make voluntary contributions. Contribution Limits CRA mandates the contribution limit for plan members as the lesser of 18% of each member's current year's earned income and a CRA set maximum dollar amount (updated annually). Vesting/Locking-in "Vesting" refers to the entitlement of a plan member to receive benefits in excess of their own contributions. "Locking-in" is the requirement that the vested contributions cannot be withdrawn until the funds are needed as retirement income (or under certain exceptional circumstances). Minimum vesting and locking-in requirements are determined by the applicable pension benefits legislation. The Federal legislated requirement is two years of plan membership. However, a plan sponsor can provide more favorable provisions. Withdrawals Members cannot withdraw required contributions while employed with the company. The member may withdraw amounts accumulated through voluntary contributions while employed, provided the plan allows for this. Funds must remain in an RPP until termination of employment, death, or retirement. Investments Members typically have control over investment decisions, however the plan sponsor retains a significant degree of fiduciary responsibility over investments available in the plan (including the selection of investment options and service providers). Each member assumes the risk and rewards of the investments they select. Termination of Employment A member is entitled to his or her own contributions and plan sponsor vested contributions. However, if the pension plan assets are locked-in, the savings cannot be withdrawn in cash and must be used to provide an income at retirement. Members also have the option to transfer accumulated amounts to another RPP or a locked-in RRSP. Retirement The plan sponsor can specify a retirement age for unreduced pension in the plan text as long as it complies with applicable pension benefits legislation and the Income Tax Act restrictions (e.g. age 65). When a member retires, funds in an RPP must be used to purchase a form of lifetime retirement income that meets the requirements of pension and tax legislation. Termination of a Plan The pension plan can be terminated by the plan sponsor at any time if sufficient notice is provided to members. Manulife, Manulife Financial, the Manulife Financial For Your Future logo and the Block Design are trademarks of The Manufacturers Life Insurance Company and are used by it, and by its affiliates under license. GP5556E 04/2011 FOR MORE INFORMATION ABOUT REGISTERED PENSION PLANS, PLEASE CONTACT YOUR MANULIFE REPRESENTATIVE.