Tax Rates & Thresholds Handy Guide

advertisement

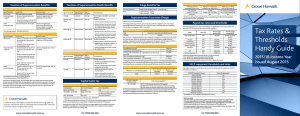

Tax Rates & Thresholds Handy Guide 2014/15 Income Year Issued August 2014 Taxation of Superannuation Benefits Superannuation benefits from a taxed source Age of recipient Lump Sum Income stream 60 and over Preservation age to age 59 Not assessable not exempt – No tax on amount below the low rate cap* Not assessable not exempt Taxed at marginal rates, but eligible for 15% tax offset Under preservation age – Taxed at a maximum rate of 15% on amount over the low rate cap Taxed at maximum rate of 20% Taxed at marginal rates, with no tax offset (15% tax offset available if a disability superannuation benefit) * Low rate cap amount: $185,000 (2014/15) Superannuation benefits from an untaxed source Age of recipient Lump sum Income stream 60 and over – Taxed at a maximum rate of 15% on amount up to the untaxed plan cap* Taxed at marginal rates but eligible for a 10% tax offset Preservation age to age 59 – Taxed at 45% on amount over the untaxed plan cap* – Taxed at maximum rate of 15% on amount up to the low rate cap** Taxed at marginal rates, with no tax offset – Taxed at maximum rate of 30% on amount above the low rate cap amount up to the untaxed plan cap Under preservation age – Taxed at 45% on amount over the untaxed plan cap – Taxed at a maximum rate of 30% on amount up to the untaxed plan cap Taxed at marginal rates, with no tax offset – Taxed at 45% on amount over the untaxed plan cap * Untaxed plan cap amount: $1.355m (2014/15) ** Low rate cap amount: $185,000 (2014/15) www.crowehorwath.com.au Taxation of Superannuation Death Benefits Payments to dependants Age of deceased Superannuation Age of death benefit recipient Any age Lump sum Any age Aged 60 and above Income stream Any age Below age 60 Tax treatment Tax-free (not assessable, not exempt income) Taxable component: – element taxed in the fund is tax-free Income stream Above age 60 – element untaxed in the fund is taxed at marginal rates. Recipient entitled to a 10% tax offset on this amount Taxable component: – element taxed in the fund is tax-free Below age 60 Income stream Below age 60 – element untaxed in the fund is taxed at marginal rates. Recipient entitled to a 10% tax offset on this amount Taxable component: – element taxed in the fund is taxed at marginal rates. Recipient entitled to a 15% tax offset on this amount – element untaxed in the fund is taxed at marginal rates Payments to non-dependants Age of deceased Superannuation Age of death benefit recipient Tax treatment Any age Lump sum Taxable component: Any age – element taxed in the fund is taxed at a maximum rate of 15% Any age Income stream Any age – element untaxed in the fund is taxed at a maximum rate of 30% – Death benefit cannot be paid as income stream – Income streams that commenced before 1 July 2007 are taxed as if received by a dependant (see above) Tel 1300 856 065 Capital Gains Tax Assets held longer than 12 months Purchase date CGT event happens CGT Calculation Before 20/9/1985 20/9/1985 - 20/9/1999 Any time After 20/9/1999 After 20/9/1999 Any time Nil Indexed cost base method* or discount method** Discount method** * Indexation of cost base frozen as at 30 September 1999 (68.7). ** 50% discount (individuals and trusts); 33 1/3% discount (complying superannuation entities, FHSA trust and life insurance companies for complying superannuation/FHSA assets). Note that from 8 May 2012, the CGT discount no longer applies to non-residents but remains available for capital gains accrued before this time where non-residents choose to obtain a market valuation of assets as at 8 May 2012. Fringe Benefits Tax FBT rate (2014/15) Fringe benefit taxable amount - gross-up rate 47 % - Type 1 benefits - 2.0802 - Type 2 benefits - 1.8868 Superannuation Guarantee Charge The SG rate is 9.5% for 2014/15. The government proposes to delay the increase in the SG rate so that it will remain at 9.5% until 2017/18, and then increase by 0.5% on 1 July of each year from 2018/19 to 2022/23, when the SG rate will be 12%. Maximum contribution base Year 2014/15 Amount in a quarterly contribution period $49,430 The maximum contribution base acts as a ceiling on an employee’s earnings for each quarter in a financial year effectively limiting the amount of superannuation support that the employer is required to provide for the employee for the quarter, and the amount of the SG shortfall (and consequent SG charge) payable in respect of the employee. Crowe Horwath is the largest provider of practical accounting, audit, tax, business and financial advice to individuals and businesses from a network of over 80 offices throughout the country. www.crowehorwath.com.au Superannuation Contributions Contribution caps Contributions cap type 2014/15 Concessional contributions cap Concessional contributions cap – aged 49 years or more on 30 June 2014 Non-concessional contributions cap* Non-concessional contributions - CGT cap amount $30,000 $35,000 $180,000 $1.355m * A bring forward rule allows individuals aged under 65 to make non-concessional contributions of up to three times their non-concessional contributions cap over a three-year period. The bringforward cap is three times the non-concessional contributions cap of the first year in which the rule applies. Government co-contribution (2014/15) Maximum co-contribution payable Lower income threshold Higher income threshold $500* $34,488 $49,488 Low income superannuation contribution 2012/13 Individual’s adjusted taxable income: $0 - $37, 000 LISC amount payable is: (i) ECC x 15% (except where (ii) or (iii) applies) (ii) $500 where the amount worked out in (i) exceeds $500 (iii) $10 where the amount worked out in (i) is less than $10 An individual is entitled to a low income superannuation contribution (LISC), based on 15% of the individual’s total eligible concessional contributions (ECC), up to a maximum of $500. However, the government proposes to abolish the LISC with effect from 1 July 2013. Spouse contributions – tax offset Receiving spouse’s assessable income* (AI) Maximum contributions entitled to tax offset (MC) Maximum tax offset (18% of the lesser of) $0 - $10,800 $10,801 - $13,799 $13,800 + $3,000 $3,000 - (AI - $10,800) Nil MC or actual contributions MC or actual contributions Nil * AI is the sum of the person’s assessable income, reportable fringe benefits total and reportable employer superannuation contributions. DISCLAIMER The information provided in this guide is believed to be accurate as at August 2014. However, the publisher and authors expressly disclaim all and any liability and responsibility to any person, of the consequences of anything done or omitted to be done by any such person in reliance of the contents of this publication. For all your taxation information, refer to the CCH Australian Master Tax Guide - the essential reference guide for tax professionals. Information is correct at time of printing. Tel 1300 856 065 Income Tax Rates Individuals (2014/15) Residents 2014/15 Taxable income (column 1) Tax on column 1 % on excess (marginal rate) $18,200 $37,000 $80,000 $180,000* Nil $3,572 $17,547 $54,547* 19 32.5 37 45* * For taxable incomes exceeding $180,000, the 2% budget repair levy applies for that part of the taxable income exceeding $180,000. Non-refundable tax offsets cannot be used to offset the budget repair levy; only the foreign income tax offset can be used to offset against the levy. Medicare levy/Medicare levy surcharge For 2014/15, the rate of Medicare levy is 2% of a resident individual’s taxable income for the income year. No Medicare levy is payable where a resident individual’s taxable income does not exceed a certain threshold amount (not yet known; $20,542 for 2013/14). Further, where a resident individual is not covered by private patient hospital insurance and their “income for surcharge purposes” for the year is more than $90,000, an additional Medicare levy surcharge of 1% to 1.5% is payable depending on their level of income and age. The table below indicates how the Medicare levy surcharge rules apply in conjunction with the private health insurance rebate rules. Singles Families* Under 65 years of age 65–69 years of age 70 years of age and over Percentage rate Income $90,001– $105,001– $105,000 $140,000 $180,001– $210,001– $0–$180,000 $210,000 $280,000 Private health insurance rebate Tier 1 Tier 2 $0–$90,000 $140,001 and over $280,001 and over Tier 3 29.04%† 19.36%† 9.68%† 0% 33.88%† 24.2%† 14.52%† 0% 38.72%† 29.04%† 19.36%† 0% 0% Medicare levy surcharge 1% 1.25% 1.5% * The families’ threshold is increased by $1,500 for each dependent child after the first. Families include couples and single parent families. † The private health insurance rebate is indexed annually by a rebate adjustment factor on 1 April each year. Accordingly, these rebate figures are only applicable from 1 July 2014 to 31 March 2015. Non-residents 2014/15 Taxable income (column 1) Tax on column 1 % on excess (marginal rate) Nil $ 80,000 $180,000 Nil $26,000 $63,000 32.5 37 45 * For taxable incomes exceeding $180,000, the 2% budget repair levy applies for that part of the taxable income exceeding $180,000. Non-refundable tax offsets cannot be used to offset the budget repair levy; only the foreign income tax offset can be used to offset against the levy. www.crowehorwath.com.au Company rates (2014/15) The following table shows the rates of tax applicable to companies in relation to their income for the 2013/14 income year. Type of company Tax Rate Private companies (other than life insurance companies) Public companies (other than life insurance companies) Companies (other than life insurance companies) that are RSA providers – Standard component of taxable income – RSA component of taxable income – FHSA component of taxable income (if any) Life insurance companies: – Ordinary class of taxable income – Complying superannuation/FHSA class of taxable income 30% 30% 30% 15% 15% 30% 15% Superannuation funds (2014/15) Type of fund Tax rate Complying superannuation funds: (i) Assessed on income, including realised capital gains and assessable contributions* (ii) Assessed on non-arm’s length income, private company dividends and certain trust distributions Non-complying superannuation funds Assessed on income, including realised capital gains and assessable contributions* Complying ADFs: (i) Assessed on income, including realised capital gains and assessable contributions (ii) Assessed on non-arm’s length income, private company dividends and certain trust distributions Non-complying ADFs: Assessed on income, including realised capital gains and assessable contributions PSTs (i) Assessed on income, including realised capital gains and assessable contributions transferred to the PST (ii) Assessed on non-arm’s length income, private company dividends and certain trust distributions. 15% 47% 47% 15% 47% 47% 15% 47% • Additional tax at the rate of 34% (complying funds) and 4% (non-complying funds) is payable on no-Tax File Number (TFN) contributions income that is included in assessable contributions. A tax offset is available if a TFN is provided to the fund within four years. Tel 1300 856 065 Personal tax offsets Personal tax offsets and rebates (2014/15) Personal tax offsets and rebates (2014/15) Cut-out when (adjusted) taxable income reaches Maximum amount Dependant spouse (with no Proposed to be abolished from dependant children) 2014/15 Dependant (Invalid and Carer) $2,535 Mature age worker Proposed to be abolished from 2014/15 Medical expenses Depending on taxpayer’s and/ or family’s adjusted taxable income, 20% of excess of net medical expenses over $2,218 or 10% of excess over $5,233. Note that transitional criteria apply Private health insurance Dependent on age of (see above) person(s) covered by policy and income level(s) Zone rebates • Ordinary Zone A $338 + 50% of dependent (invalid and carer) tax offset (proposed) • Ordinary Zone B $57 + 20% of dependent (invalid and carer) tax offset (proposed) • Special Zone A or B $1,173 + 50% of dependent (invalid and carer) tax offset (proposed) Defence Force Same as for Ordinary Zone A Income arrears Applicable to lump sum Medicare levy surcharge lump payments of income paid in sum arrears arrears $10,422 Low income earner’s tax offset (2014/15) Taxable income Amount of offset $0 - $37,000 $37,000-$66,667 > $66,667 $445 $445 - [(taxable income - $37,000) x 1.5%] Nil Senior Australians and Pensioners Tax Offset (2014/15) Family situation Maximum offset Single Couple (each) Illness separated couple $2,230 $1,602 $2,040 Shade-out threshold Cut-out threshold $32,279 $28,974 $31,279 $50,119 $41,790 $47,599 For further information on the availability and application of tax offsets, see Chapter 15 of the CCH Australian Master Tax Guide. www.crowehorwath.com.au Taxation of Employment Related Payments Life benefit employment termination payments Component Tax treatment Tax free component Taxable component Tax-free • P reservation age and over – amount up to ETP cap* — taxed at a maximum rate of 15% – amount over ETP cap* — taxed at 45% • B elow preservation age – amount up to ETP cap* — taxed at a maximum rate of 30% – amount over ETP cap* — taxed at 45% * ETP cap amount: $185,000 (2014/15). For certain ETPs, the ETP cap works in conjunction with a whole-of-income cap ($180,000). Preservation age Date of birth Preservation age Before 1 July 1960 1 July 1960 – 30 June 1961 1 July 1961 – 30 June 1962 1 July 1962 – 30 June 1963 1 July 1963 – 30 June 1964 On or after 1 July 1964 55 56 57 58 59 60 Tel 1300 856 065 Death benefit employment termination payments Component Tax treatment Tax free component Taxable component Tax-free •P ayment to a dependant – amount up to ETP cap — tax-free – amount over ETP cap — taxed at 45% •P ayment to a non-dependant – amount up to ETP cap — taxed at a maximum rate of 30% – amount over ETP cap — taxed at 45% •P ayment to trustee of deceased estate – taxed in the hands of the trustee, based on whether the beneficiary is a dependant or non-dependant (see above) * ETP cap amount: $185,000 (2014/15) Genuine redundancy and early retirement scheme payments Income year Base amount Plus for each complete year of service 2014/15 $9,514 $4,758 Unused annual leave payment rules Assessable portion Period of accrual of leave Maximum rate General retirement or termination: – accrual before 18 August 1993 100% 30% – accrual on or after 18 August 1993 100% Marginal Genuine redundancy amount, early retirement scheme amount or invalidity amount paid on or after 18 August 1993 100% 30% Unused long service leave payment rules Period of accrual of leave Assessable portion Maximum rate 5% Marginal General retirement or termination: – accrual before 16 August 1978 – accrual 16 August 1978 to 17 August 1993 100% 30% – accrual on or after 18 August 1993 Genuine redundancy amount, early retirement scheme amount or invalidity amount: 100% Marginal 5% Marginal 100% 30% – accrual before 16 August 1978 – accrual on or after 16 August 1978 Produced by www.cch.com.au www.crowehorwath.com.au