Analyzing credit risk

Optimizing opportunities

Why Asset Management

Firms Rely On

Moody’s KMV

Working with you.

Whether managing mutual funds, hedge funds, institutional accounts or any other type of

investment, portfolio managers need quality information and reliable credit risk tools to:

Th e N e e d f o r C r e d i t R i s k Ma n a g e m e n t

Enhance investment returns by identifying improving

n

The ever-changing investment marketplace offers

a broad array of opportunities across a number of

asset classes — from traditional debt instruments

to structured products. Regardless of investment

orientation, understanding and managing credit risk

is fundamental to making investment decisions and

determining fair pricing.

or deteriorating credits, performing “rich/cheap” analyses

and “stress testing” portfolios across industries, sectors

and indices.

Provide a structured, unbiased framework to

highlight relative value opportunities and examine

fundamental assumptions.

n

Conduct thorough capital and credit structure analysis

n

of complex deals such as structured products and

leveraged buyouts to determine the accuracy of implied

value and identify capital structure arbitrage.

Identify riskiest exposures and provide early warnings

n

of credit deterioration in their own portfolios and with

counterparties, through continued monitoring and

surveillance of credit quality.

Track, monitor and report risks in portfolios, and in

n

those of clients.

Hedge appropriately against downside risk and

n

generate additional income through the purchase and/or

sale of structured credit products, a growing business

among asset managers seeking to increase absolute returns.

RESULTS FOR OUR ASSET MANAGEMENT CLIENTS

Moody’s KMV serves more than

1,800 clients in 85 countries,

including some of the world’s

best-known institutional

money managers, mutual fund

companies and hedge funds.

Our clients best demonstrate

how our credit risk solutions

help manage their portfolios

and those of their clients.

“ MKMV forms an integral

part of Pioneer’s investment

process. In particular,

MKMV is an input into

credit risk assessment,

applied as part of a wider

quantitative screening tool,

incorporated within relative

value analysis and overall

helps to shape portfolio

construction and bottom-up

security selection.”

Francesco Sandrini

Senior Vice President

Head of Financial Engineering

Pioneer Global

Asset Management

“ Being a global corporate

bond investor with an intense

focus on name diversification,

Moody’s KMV plays a vital

role in our investment

process. Their tools help

us in finding deteriorating

credits and identifying

relative value opportunities.”

“ Moody’s KMV helps us

identify anomalies in

the capital markets and

is a valuable tool in our

investment process.”

Michael Fischer

Head of Quantitative Research

CQS

Arne W. Eidshagen

CFA

Portfolio Manager

KLP Asset Management

Moody’s KMV solutions are used by asset

management firms to bring greater transparency

to credit risk exposures and enhance relative

value pricing capabilities that, in turn, improve

investment returns.

ILLUMINATING RISK AND RETURN

Working with us.

Moody’s KMV is the global standard in

credit risk management. We transform vast

amounts of data and cutting-edge models

into enterprise-class solutions that cut

across the credit risk spectrum.

As the industry leader, our clients gain a critical competitive advantage

through our deeper, consistent and reliable insight. We provide

professional consulting, thought leadership, client service and expert

training that keep our clients “ahead-of-the-curve” in implementing

credit strategies.

We offer asset managers a number of credit risk solutions to manage

both individual and portfolio counterparty risk. Clients rely on us because

we offer:

n

n

n

n

n

“Moody’s KMV is the top risk

management systems vendor

of the past 20 years.”

Risk magazine

A dedicated team of sales and credit risk specialists who

understand the needs of the asset management business.

Superior quantitative metrics to conduct in-depth

analyses and manage credit risk exposures.

Models built upon the largest, most robust collection of

public and private company default information available

anywhere in the world.

Valuation tools from an independent source of credit risk

analysis to enhance pricing for investment decisions.

Internet solutions that can be immediately utilized as well

as enterprise-class systems that can be implemented in as

little as six months.

ASSET MANAGEMENT FIRMS

Moody’s KMV offers asset management

firms a range of solutions that cut across

the credit risk spectrum.

SIN G L E - R I S K A S S E S S M E N T

VALUATION

Our

solutions.

PORTFOLIO RISK MANAGEMENT

MOODY’S KMV:

A UNIQUE COMP E T I T I V E A D V A N T A G E

Moody’s KMV solutions measure and identify key

Moody’s KMV offers a number of tools that enable

Moody’s KMV has a comprehensive methodology for

EDF %

35%

credit risk drivers. These are available via XML

asset managers to evaluate credit risk within

measuring and benchmarking credit portfolio risks.

20%

to facilitate an efficient way to perform multiple

individual instruments and at the portfolio level.

market scenario analyses.

solution that offers insights into the contribution of

individual exposures to portfolio risk; credit migration

analysis and risk/return analysis for hedges and trades;

full portfolio loss and value distributions, both in

absolute terms and relative to a benchmark; Monte

Carlo-based calibrations drawn from the world’s

richest credit data sources; and scenario analysis to

stress-test a portfolio and perform what-if analyses.

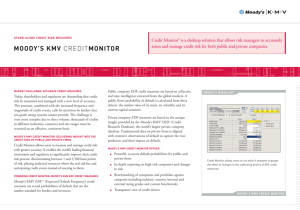

RiskFrontier covers a wide range of asset classes,

including loans, bonds, credit default swaps, CDO

tranches and equity.

updates on Moody’s KMV EDF™ (Expected Default

Frequency) measures and implied ratings for more than

30,000 public companies globally. It is also available

through a data file service format for use within client

proprietary systems allowing further data manipulation

and customization to suit individual client needs.

leverages default, migration, and correlation modeling;

calculates “fair value,” first-dollar-loss probability,

loss severity, and the internal rate of return for both

cash flow and synthetic CDO tranches. By utilizing

industry-leading pricing techniques, it computes breakeven spreads and hedge ratios for the protection against

movements in the underlying collateral or index.

Moody’s KMV RiskCalc® is an Internet tool that

Loan Valuation Web Service™ is an Internet tool

combines financial statement information and market

data with in-depth knowledge of default drivers to

produce EDF measures and implied ratings for private

companies in country-specific models.

that allows investors to use EDF measures and LGD

data to mark their loan portfolios for pricing or

fair valuation.

PROFESSIONAL SERVICES

CreditEdge® Plus is an Internet tool for calculating

Moody’s KMV also provides consulting services

daily EDF implied spread values. In addition to

single-risk management assessment, it provides a “fair

valuation” pricing framework for evaluating loan, bond

and credit default swap (CDS) instruments and can be

used to perform stress tests and sensitivity analyses on

entire portfolios. CreditEdge Plus is available with both

data file service and XML features.

that help clients customize their credit risk

Moody’s KMV LossCalc™ is an Internet tool that

offers predictive estimates of loss given default (LGD)

for bonds, loans and preferred stocks. It is powered

by market and security level information on rated and

unrated public and private firms. LossCalc is available

through a data file service format for use within client

proprietary systems allowing further data manipulation

and customization to suit individual client needs.

5

RiskFrontier™ is a “next generation” enterprise-class

CDO Analyzer™ is a downloadable solution that

CreditEdge® is an Internet tool providing daily

10

management processes.

Ca-C

2

Illustration:

Defaulted company EDF measure versus

industry group median EDF measure

1.0

.5

Caa

.20

.10

.05

.01

07/12/06 08/23/06

10/04/06

11/15/06

12/27/06

02/07/07

03/21/07

05/02/07

06/13/07

Sample Company EDF

Industry Peer Group EDF

Data: Moody’s KMV database, used for all of our models, is

the most comprehensive in the industry containing information

on both public and private institutions around the world. The

Moody’s KMV CRD® (Credit Research Database) of private

company data is routinely cleansed and filtered to ensure that

only the highest quality data is used in our solutions.

EDF measures: Moody’s KMV is the inventor of EDF

(Expected Default Frequency) measures. More granular and

mathematical than ordinal ratings, clients consider EDF

measures to be the most powerful and forward-looking in the

industry for forecasting default probabilities. The most recent

model version (EDF 8.0) comprises more than 30,000 public

companies globally, scoring them daily on a scale of .01 to 35

percent, as determined by enterprise value, enterprise volatility

and liability structure. Private company EDF measures are

built on financial statement data reflecting a number of

variables including profitability, activity, leverage, liquidity,

size, growth variables and debt coverage.

B

Baa

A

Aa

Aaa

North and South America

+1 (866) 321-MKMV (6568) or +1 (415) 874-6000

Europe, the Middle East and Africa +44 (20) 7280-8300

Asia-Pacific

+852 3551-3000

Japan

+81 (3) 3218-1160

E-mail

info@mkmv.com

www.moodyskmv.com

Copyright © 2007 Moody’s KMV Company. All rights reserved. Unless otherwise designated,

all trademarks are owned by MIS Quality Management Corporation and used under license.

Analyzing credit risk

Managing Portfolios

Why Banks

Rely On Moody’s KMV

Working with you.

As banks strive to maintain regulatory compliance, improve their capital management and

maximize performance, they require tools to help them:

THE NEED FOR CREDIT RISK MANAGEMENT

n

Is there a business that understands the importance

of credit risk management better than a bank?

Accuracy and consistency in credit risk management

are the linchpins of success or failure in the world of

banking. It is fundamental to ensuring that a bank’s

balance sheet not only meets regulatory standards

but that it is optimized to generate more income

and deliver profitable results.

of enterprise-wide capital to improve overall portfolio

performance and shareholder value.

n

Today’s global marketplace has exacerbated this

need as major corporations and small-and mediumsized enterprises alike now experience the free flow

of capital across borders and the impact of foreign

market interdependence on their business cycles.

These factors have sharpened the need for banks to

understand more complex credit risk issues and have

inspired regulators to raise the bar for credit standards

that ensure global comparability.

Identify the riskiest credit exposures and

concentrations to provide early warnings of credit

deterioration in loan books and investment portfolios.

n

Anticipate changes in the credit environment to modify

underwriting and portfolio parameters.

n

Ensure the performance accuracy of internal

rating models.

n

Conduct stress tests to determine how well portfolios

can withstand various stress scenarios

n

“Better risk management may be

the only truly necessary element

of success in banking.”

Alan Greenspan, October 2004

Calculate economic capital to maximize the efficient use

Make efficient and informed risk-based pricing

decisions for all bank products from corporate loans

to structured credits.

Basel II

In 2002, Basel II set forth recommendations on

capital adequacy and the development of an

efficient framework to support analytical integrity

on a global basis. Since then, Moody’s KMV has

helped banks around the world comply with these

guidelines to facilitate regulatory approval. Our

solutions help banks in developed economies and

emerging markets achieve best practices in credit

risk management.

IMPROVING CAPITAL MANAGEMENT

Working with us.

Moody’s KMV is the global standard in

credit risk management. We transform vast

amounts of data and cutting-edge models

into enterprise-class solutions that cut

across the credit risk spectrum.

For more than 20 years, we have helped banks manage credit risk — the

most fundamental element of their business — and have received multiple

awards for our industry leadership. We provide professional consulting,

thought leadership, client service and expert training that keep our clients

“ahead-of-the-curve” in implementing their credit strategies.

RESULTS FOR OUR BANKING CLIENTS

Moody’s KMV serves more

than 1,300 banks in more

than 85 countries, from global

institutions and regional money

centers to small community

organizations. Our clients best

demonstrate how we serve a

broad spectrum of credit risk

needs to improve business

operations and results.

“ Most of our investors are

happy if they see that you

assessed the portfolio with

RiskCalc because it is one of

the best known products in

the market, not just locally

but in the rest of Europe and

Asia as well.”

Michael Auracher

Head of the Structured

Solutions Group

HSBC Trinkaus & Burkhardt AG

“ Our partnership with

Moody’s KMV has more

than paid for itself. It has

enabled us to make better

and faster lending decisions

that are good for the Bank

and good for our customers.

As a result, we are a better

financial partner to the

residents and businesses

in our community.”

“ We’re in a partnership with

Moody’s KMV and it’s been

very beneficial to us. I think

this gives us a tremendous

competitive advantage. It’s

everything we’ve hoped it

would be.”

Dr. Terry Benzschawel

Head of Credit Modeling Group

Citi Markets and Banking

Tom Sommer

Senior Vice President and

Chief Credit Officer

Central Valley Community Bank

Banking clients work with us because we offer:

n

A dedicated team of professionals focused strictly on the

unique needs of the banking industry.

The Benefits of Economic Capital

n

n

Models built upon the largest, most robust collection of

public and private company default information available

anywhere in the world.

n

“Moody’s KMV is the top risk

management systems vendor

of the past 20 years.”

n

Superior methodologies to evaluate probabilities of

default and loss given default, from loan origination to

portfolio management.

Risk magazine

n

n

n

n

Valuation tools from an independent source of credit risk

analysis to enhance pricing insights on bank loans and

other instruments.

Portfolio management capabilities that measure and

benchmark credit portfolio risk as well as calculate

economic capital on an enterprise-wide basis.

Consulting capabilities to plan, develop and implement

customized credit risk systems, as well as validate and

calibrate existing internal models.

Internet solutions that can be immediately utilized as well

as enterprise-class systems that can be implemented in as

little as six months.

A client reported loan loss savings of roughly

six times the cost of purchasing portfolio

management tools over a three-year period.

As a result, the bank was able to originate three

times as many loans on the same capital base.

A client eliminated “non-core” customers, which

reduced the size of its portfolio by 35% and

economic capital by 70%. This significantly

increased returns and the capacity to use the

bank’s balance sheet more profitably.

Moody’s KMV helps banks build new

internal ratings-based credit risk models as

well as validate and calibrate their existing

models to assess single obligor credit risk,

monitor holdings and maximize overall

portfolio performance.

Moody’s KMV offers banks a range

of solutions that cut across the credit

risk spectrum.

Our

solutions.

BANKS

DAT A C O L L E C T I O N & A N A L Y S I S

VALUATION

Moody’s KMV solutions help banks to easily collect and

effectively analyze data.

Moody’s KMV offers solutions in determining the value of

loans, bonds and credit default swap instruments.

RiskAnalyst™ is a tool that provides a foundation for

CreditMark® is an Internet solution that provides a robust

developing an internal rating system. It improves the speed,

accuracy and consistency of data capture, analytics and the

storage of borrower and facility information. Through its

rating module, RiskAnalyst stores industry templates and

scorecards so all credit data can reside within one platform.

mark-to-market platform to accurately value thousands of

credit instruments on a daily basis by combining their terms

and conditions with valuation models, market data and

portfolio information.

CreditEdge® Plus is an Internet tool that provides a “fair-

Moody’s KMV solutions measure and identify key risk

drivers. These are available via XML to facilitate an

efficient way to perform multiple scenario analyses.

Moody’s KMV RiskCalc® is an Internet solution that

PORTFOLIO RISK MANAGEMENT

delivers country-specific models utilizing financial statement

information and market data with in-depth knowledge of

default drivers to produce Moody’s KMV EDF™ (Expected

Default Frequency) measures and implied ratings for small

and medium enterprises.

CreditEdge® is an Internet tool that compiles data from a

variety of forward-looking, timely sources and delivers daily

EDF measures and implied ratings on more than 30,000

corporate firms globally. It is available through a data file

service format for use within client proprietary systems

allowing further data manipulation and customization to suit

individual client needs.

MOODY’S KMV:

A UNIQUE COMP E T I T I V E A D V A N T A G E

EDF %

35%

Moody’s KMV provides consulting services that

help clients customize their credit risk management

programs. Clients can benefit from three areas

of expertise:

20%

10

5

Ca-C

2

Advisory Services provides counsel on how best to

Illustration:

Defaulted company EDF measure versus

industry group median EDF measure

optimize a client’s credit risk management practices from

risk evaluation to active portfolio management.

1.0

.5

Caa

.20

valuation” pricing framework for evaluating loan, bond

and credit default swap (CDS) instruments facilitating a

relative value credit risk comparison to existing marketplace

valuations. It is also available with both data file service and

XML features and provides the ability to perform stress tests

and sensitivity analyses on entire portfolios.

SIN G L E - R I S K A S S E S S M E N T

PROFESSIONAL SERVICES

Moody’s KMV also provides tools for analyzing credit

portfolio risk.

RiskFrontier™ is a “next-generation” enterprise-class solution

that measures credit portfolio risk, concentrations and

the management of economic capital. Covering a wide

range of asset classes, including loans, bonds, credit default

swaps, CDO tranches, and equity, it offers insights into the

contribution of individual exposures and concentrations

to portfolio risk; risk/return analysis for hedges and trades;

full portfolio loss and value distributions, both in absolute

terms and relative to a benchmark; and Monte Carlo-based

calibrations drawn from the world’s richest credit data

sources. RiskFrontier is used to perform routine portfolio

analysis and reporting; conduct scenario analyses for stress

testing; support capital allocation and pricing decisions,

and manage strategic portfolio planning.

DealAnalyzer® is a solution that evaluates a prospective

loan in the context of an institution’s current portfolio

to facilitate credit risk capital allocation and diversification

at the origination level.

Modeling Services develops models and provides the

.10

validation and calibration of internal credit risk models.

.05

Implementation Services works with clients to plan

software customization and the installation of credit risk

management solutions into their existing systems.

.01

07/12/06 08/23/06

10/04/06

11/15/06

12/27/06

02/07/07

03/21/07

05/02/07

06/13/07

Sample Company EDF

Industry Peer Group EDF

Data: Moody’s KMV database, used for all of our models, is

the most comprehensive in the industry containing information

on both public and private institutions around the world. The

Moody’s KMV CRD® (Credit Research Database) of private

company data is routinely cleansed and filtered to ensure that

only the highest quality data is used in our solutions.

EDF measures: Moody’s KMV is the inventor of EDF

(Expected Default Frequency) measures. More granular and

mathematical than ordinal ratings, clients consider EDF

measures to be the most powerful and forward-looking in the

industry for forecasting default probabilities. The most recent

model version (EDF 8.0) comprises more than 30,000 public

companies globally, scoring them daily on a scale of .01 to 35

percent, as determined by enterprise value, enterprise volatility

and liability structure. Private company EDF measures are

built on financial statement data reflecting a number of

variables including profitability, activity, leverage, liquidity,

size, growth variables and debt coverage.

B

Baa

A

Aa

Aaa

North and South America

+1 (866) 321-MKMV (6568) or +1 (415) 874-6000

Europe, the Middle East and Africa +44 (20) 7280-8300

Asia-Pacific

+852 3551-3000

Japan

+81 (3) 3218-1160

E-mail

info@mkmv.com

www.moodyskmv.com

Copyright © 2007 Moody’s KMV Company. All rights reserved. Unless otherwise designated,

all trademarks are owned by MIS Quality Management Corporation and used under license.

Managing Credit Risk Maximizing Performance

Why Corporations

Rely On Moody’s KMV

Working with you.

The adoption of meaningful credit risk programs can shape greater consistency, assist

hedging strategies and improve capital management across an organization to substantially

increase firm value. As corporations seek to enhance business performance and, in some

cases, address regulatory compliance, they require credit risk solutions to:

THE NEED FOR CREDIT RISK MANAGEMENT

In today’s marketplace, corporations experience the

free flow of capital across borders and the impact of

foreign market inter-dependence on their business

cycles. As boundaries disappear, corporate executives

require quality information and sophisticated analytical

tools to measure and manage their credit risk.

From pre-screening customers and suppliers to

diversifying an overall portfolio of business exposures,

credit risk solutions need to cut across a worldwide

horizon. And because one event can devastate

business performance and negatively impact

a company’s stock price, corporate executives

recognize that early-warning indicators of

deteriorating credits are the best defense.

n

Identify high-risk exposures or the weak financial

condition of counterparties that are crucial to their

business process.

n

Introduce efficiency and consistency to distill financial

data and execute a meaningful scale to measure credit risk

across the firm.

n

Anticipate changes in the credit environment when

addressing new business scenarios in light of changing

market dynamics.

n

Qualify new customers and suppliers both on a regional

and global basis.

n

Address credit reserve parameters to strengthen fiscal

responsibility and improve overall performance.

RESULTS FOR OUR CORPORATE CLIENTS

Moody’s KMV serves more than

1,800 clients in 85 countries,

including major corporations

across a variety of industries

ranging from technology and

energy to healthcare and large

industrials. Our clients best

demonstrate how we serve a

broad spectrum of credit risk

needs to improve business

operations and results.

“ With approximately 15

internal entities creating

risk with over 600

counterparties, we needed

a rapid, market-based view

of an organization’s financial

strength. We selected

Moody’s KMV CreditEdge

because it includes daily

market measures, rather

than relying solely on

financial information that

can be three months old

at best. CreditEdge has

significantly improved the

efficiency and accuracy of

our credit review process.”

“ By using Moody’s KMV

RiskCalc, we gain significant

value in two ways:

improvement in the overall

quality of our credit risk

management process

across the company and

the continuous expansion

of our global credit risk

analysis knowledge.”

Zhe Nie

Analyst

Essent Energy Trading B.V.

“ Our internal risk policy is

built around Moody’s KMV

EDFs. A customer is placed

on ‘pre-pay’ status once an

EDF goes above 1.00%. We

reduced exposure to Dana

Corporation over six months

prior to their March 2006

default, saving our company

over $2 million in credit

losses. We also saved

time and legal costs by not

having to be a claimant in

their bankruptcy.”

Energy Company

F. Scott Wilkerson

Director of Enterprise

Credit Risk Management

NiSource Inc.

MAKING CORPORATIONS MORE COMPETITIVE

Working with us.

Moody’s KMV is the global standard in

credit risk management. We transform vast

amounts of data and cutting-edge models

into enterprise-class solutions that cut

across the credit risk spectrum.

As the industry leader, our clients gain a critical competitive advantage

through our deeper, consistent and reliable insight. We provide

professional consulting, thought leadership, client service and expert

training that keep our clients “ahead-of-the-curve” in implementing

credit strategies.

Corporations choose to work with Moody’s KMV because we offer:

n

n

n

n

n

n

“Moody’s KMV is the top risk

management systems vendor

of the past 20 years.”

Risk magazine

A dedicated team of sales and credit risk specialists

focused exclusively on corporate clients.

Industry-leading models supported by robust data that

forecast default probabilities and provide implied ratings.

Valuation tools from an independent source of credit risk

analysis to enhance pricing insights on credit instruments.

Portfolio management capabilities that measure

and benchmark credit portfolio risk to justify credit

capital reserves.

Consulting capabilities to plan, develop and implement

customized credit risk models and systems.

Internet solutions that can be immediately utilized as well

as enterprise-class systems that can be implemented in as

little as six months.

Moody’s KMV offers corporations credit risk

solutions that enhance shareholder value.

We provide early warning indicators of

customer and supplier credit quality that

bring greater efficiency and consistency to

the management process.

CORPORATIONS

Moody’s KMV offers corporations

a range of solutions that cut across

the credit risk spectrum.

DAT A C O L L E C T I O N & A N A L Y S I S

VALUATION

Our

solutions.

PROFESSIONAL SERVICES

MOODY’S KMV:

A UNIQUE COMP E T I T I V E A D V A N T A G E

Moody’s KMV solutions easily collect and score

Moody’s KMV offers a tool to price credit risk

Moody’s KMV provides consulting services for

EDF %

35%

financial data.

with efficiency.

the development and customization of credit risk

20%

management systems. Clients can benefit from three

10

RiskAnalyst™ is a system that provides a foundation

CreditEdge® Plus is an Internet tool that provides

for internal credit ratings. It improves the speed,

accuracy and consistency of capturing, analyzing

and storing financial and non-financial information

on counterparties.

a framework for evaluating credit pricing and

facilitating a comparison to existing marketplace

valuations. It is also available through a data file

service and XML formats for use within client

proprietary systems.

SIN G L E - R I S K A S S E S S M E N T

Implementation Services works with clients to plan

Advisory Services provides counsel on how best to

measuring and benchmarking credit portfolio risks.

optimize a client’s credit risk management practices

from risk evaluation to active portfolio management.

available via XML to facilitate an efficient way to

EDF measures and implied ratings on more than

30,000 publicly traded firms globally. It is available

through a data file service for use within client

proprietary systems allowing further data manipulation

and customization to suit individual client needs.

RiskFrontier™ is a “next-generation” enterprise-class

solution that offers insights into the contribution

of individual exposures; concentration risks from

industries and geographies; hedging strategies;

capital reserve adequacies; and the potential level of

catastrophic losses. By performing routine portfolio

analysis and reporting, as well as scenario analyses for

stress testing, RiskFrontier supports capital allocation

and pricing decisions for strategic portfolio planning.

Caa

.20

.10

.05

.01

07/12/06 08/23/06

Moody’s KMV has a comprehensive methodology for

CreditEdge® is an Internet tool that delivers daily

.5

validation and calibration of internal credit risk models.

identify and measure key risk drivers. These are

utilizes financial statement information and market

data with in-depth knowledge of default drivers to

produce Moody’s KMV EDF™ (Expected Default

Frequency) measures and implied ratings on private

companies in country-specific models.

1.0

software customization and the installation of credit

risk management solutions into their existing systems.

customers, Moody’s KMV solutions help them

Moody’s KMV RiskCalc® is an Internet tool that

Illustration:

Defaulted company EDF measure versus

industry group median EDF measure

Modeling Services develops models and provides the

PORTFOLIO RISK MANAGEMENT

Ca-C

2

As corporations consider extending credit to

perform multiple scenario analyses.

5

areas of expertise:

10/04/06

11/15/06

12/27/06

02/07/07

03/21/07

05/02/07

06/13/07

Sample Company EDF

Industry Peer Group EDF

Data: Moody’s KMV database, used for all of our models, is

the most comprehensive in the industry containing information

on both public and private institutions around the world. The

Moody’s KMV CRD® (Credit Research Database) of private

company data is routinely cleansed and filtered to ensure that

only the highest quality data is used in our solutions.

EDF measures: Moody’s KMV is the inventor of EDF

(Expected Default Frequency) measures. More granular and

mathematical than ordinal ratings, clients consider EDF

measures to be the most powerful and forward-looking in the

industry for forecasting default probabilities. The most recent

model version (EDF 8.0) comprises more than 30,000 public

companies globally, scoring them daily on a scale of .01 to 35

percent, as determined by enterprise value, enterprise volatility

and liability structure. Private company EDF measures are

built on financial statement data reflecting a number of

variables including profitability, activity, leverage, liquidity,

size, growth variables and debt coverage.

B

Baa

A

Aa

Aaa

North and South America

+1 (866) 321-MKMV (6568) or +1 (415) 874-6000

Europe, the Middle East and Africa +44 (20) 7280-8300

Asia-Pacific

+852 3551-3000

Japan

+81 (3) 3218-1160

E-mail

info@mkmv.com

www.moodyskmv.com

Copyright © 2007 Moody’s KMV Company. All rights reserved. Unless otherwise designated,

all trademarks are owned by MIS Quality Management Corporation and used under license.

Managing Capital

Enhancing Returns

Why Insurance

Companies Rely On

Moody’s KMV

Working with you.

From life, and property and casualty, to reinsurance and monolines, insurance companies

need quality information and reliable credit risk tools that help them better manage both the

investment and liability management requirements of their businesses. Specifically, effective

credit risk management can help to:

THE NEED FOR CREDIT RISK MANAGEMENT

n

Who understands the importance of managing risk

better than an insurance company?

From the threat of natural disasters to the uncertainties

of credit and equity markets, insurance companies

routinely deal with a number of risky “unknowns”

that can significantly affect their success. Credit risk

demands the full attention of insurance companies

because it impacts both sides of their balance sheet.

As a result, meaningful credit risk management

strategies are required to:

n

Manage Investments: Diversify risk and enhance returns.

This is especially important as all types of insurance

companies move more aggressively from traditional fixed

income investing to more active participation in highyield and structured credit products such as credit-linked

notes, credit default swaps and synthetic collateralized

debt obligations (CDOs).

n

Manage Liabilities: Improve risk-based pricing and

capital allocation decisions to optimize results within

regulatory constraints. Specific to property and casualty

and specialty providers, Moody’s KMV can help insurers

better understand the credit risk exposures embedded in

their product lines that lead to better pricing, collateral

setting and portfolio management.

n

n

Build a structured, unbiased framework to highlight

n

Basel II and the European Union’s Solvency II initiative,

Identify riskiest exposures and provide early warnings

which are likely to influence similar standards throughout

the world.

of credit deterioration in their insured exposures and

investment portfolios through continued monitoring

and surveillance of credit quality.

n

Enhance investment returns by identifying improving

n

n

Hedge appropriately against downside risk and

generate additional income through the purchase and/or

sale of structured credit products, an option that is being

used more frequently by insurance companies.

n

Calculate economic capital to maximize the efficient

use of enterprise-wide capital to improve overall

portfolio performance and shareholder value, assuring

that the company will be able to confidently sustain

financial “shocks” brought about by excessive claims

or market conditions.

Qualify prospects and improve policy pricing through

the use of fair and accurate credit assessments.

or deteriorating credits, performing “rich/cheap” analyses

and “stress testing” portfolios across industries, sectors

and indices.

n

Implement risk-based approaches prompted by

opportunities and examine fundamental assumptions.

More effectively manage the correlation between

the financial health of a client and the probability

of future claims.

Anticipate broader changes in the credit environment

in light of changing market indicators.

“INSURANCE” FOR MANAGING CREDIT RISK

Working with us.

Moody’s KMV is the global standard in

credit risk management. We transform vast

amounts of data and cutting-edge models

into enterprise-class software solutions that

cut across the credit risk spectrum.

As the industry leader, our clients gain a critical competitive advantage

through our deeper, consistent and reliable insight. We provide

professional consulting, thought leadership, client service and expert

training that keep our clients “ahead-of-the-curve” in implementing

credit strategies.

RESULTS FOR OUR INSURANCE CLIENTS

Moody’s KMV serves more than

1,800 clients in 85 countries,

including life insurance, property

and casualty, and reinsurance

companies. Our clients best

demonstrate how we serve a

broad spectrum of credit risk

needs to improve business

operations and results.

“ Moody’s KMV provides

us with user-friendly,

customizable tools that will

serve as the foundation of our

group’s credit management

processes worldwide,

enabling us to make more

informed decisions regarding

economic capital allocation.”

Raj Singh

Credit Risk Officer

Allianz Group

“ Spurred on by Solvency II,

insurance companies are

refining their approach to

managing credit risk. As a

result, some insurers’ credit

risk management methods

are beginning to converge

with those favoured by banks.

Insurers such as Swiss Re,

Munich Re and ING Insurance

were early adopters of credit

portfolio modelling practices,

and have put in place

measurement tools such

as Moody’s KMV Portfolio

Manager, a credit portfolio

risk measurement tool.

Companies like ours,

with a strong focus on

economic capital, started,

like banks, to look at credit

portfolio management in the

late 1990s as a way to identify

and measure risk from an

economic point of view,

instead of from a regulatory

or a rating agency point

of view.”

Davide Crippa

Head of Credit Solutions

Portfolio Management

and Analytics

Swiss Re

Insurance companies rely on Moody’s KMV because we offer:

n

n

“Moody’s KMV is the top risk

management systems vendor

of the past 20 years.”

n

Risk magazine

n

n

n

n

A dedicated team of sales and credit risk specialists who

understand the needs of the insurance industry.

Models built upon the largest, most robust collection of

public and private company default information available

anywhere in the world.

Correlated default analysis is critical to insurance

companies that are required to maintain high

quality agency ratings. With the breadth and depth

of our data, Moody’s KMV provides a portfolio

modeling and correlation framework that stands

without peer, and is recognized as “best of class”

in default analysis.

Superior methodologies to evaluate probabilities of default

and loss given default from underwriting decisions through

to portfolio management.

Valuation tools from an independent source of credit

risk analysis to enhance pricing insights on policies

and investments.

Portfolio management capabilities that measure and

benchmark credit portfolio risk as well as calculate

economic capital on an enterprise-wide basis.

Consulting capabilities to plan, develop and implement

credit risk models and systems.

Internet solutions that can be immediately utilized

as well as enterprise-class systems that can be

implemented in as little as six months.

Moody’s KMV provides insurance companies with

solutions that assist in accurately measuring

and managing credit risk to enhance value and

maximize returns. In addition, Moody’s KMV helps

insurance companies deploy an economic capital

framework to maintain a competitive edge while

satisfying regulatory requirements.

INSURANCE COMPANIES

Moody’s KMV offers insurance companies

a range of solutions that cut across the

credit risk spectrum.

INVESTMENT MANAGEMENT

Our

solutions.

LIABILITY MANAGEMENT

MOODY’S KMV:

A UNIQUE COMP E T I T I V E A D V A N T A G E

Moody’s KMV provides a suite of proven credit

risk solutions to improve portfolio performance

and enhance investment returns. Credit risk

management tools offered by Moody’s KMV include:

CreditEdge Plus is an Internet tool that delivers daily

®

Moody’s KMV EDF™ (Expected Default Frequency)

measures and implied ratings on more than 30,000

publicly traded firms globally and provides a “fair

valuation” pricing framework for evaluating bond and

CDS instruments. It also performs stress tests and

sensitivity analyses on entire portfolios.

Moody’s KMV RiskCalc® is an Internet tool that

combines financial statement information and market

data with in-depth knowledge of default drivers to

produce EDF measures for private companies in countryspecific models. RiskCalc is also used to arrive at implied

ratings for private companies and “shadow ratings” for

unrated collateralized debt/loan obligation assets.

Moody’s KMV LossCalc™ is an Internet tool that offers

predictive estimates of loss given default (LGD) for

bonds, loans and preferred stocks.

Loan Valuation Web Service™ is an Internet tool that

allows investors to use EDF measures and LGD data to

mark their loan portfolios for pricing or fair valuation.

CDO Analyzer is a downloadable solution that

™

leverages default, migration and correlation modeling;

calculates “fair value,” first-dollar-loss probability,

loss severity, and the internal rate of return for both

cash flow and synthetic CDO tranches. By utilizing

industry-leading pricing techniques, it computes breakeven spreads and hedge ratios for the protection against

movements in the underlying collateral or index.

RiskFrontier™ is a “next-generation” enterprise-

class solution that measures credit portfolio risk,

concentrations and the management of economic

capital. Covering a wide range of asset classes, including

loans, bonds, credit default swaps, CDO tranches,

and equity, it offers insights into the contribution of

individual exposures and concentrations to portfolio

risk; risk/return analysis for hedges and trades; full

portfolio loss and value distributions, both in absolute

terms and relative to a benchmark; and Monte Carlobased calibrations drawn from the world’s richest credit

data sources. RiskFrontier is used to perform routine

portfolio analysis and reporting; conduct scenario

analyses for stress testing; support capital allocation

and pricing decisions, and manage strategic portfolio

planning.

In addition to the tools that calculate probability

EDF %

35%

of default, Moody’s KMV offers a framework that

20%

can help insurance companies to manage the data

10

5

required for their credit risk management system:

Ca-C

2

Illustration:

Defaulted company EDF measure versus

industry group median EDF measure

RiskAnalyst is a tool that provides the foundation

™

1.0

.5

for developing an internal rating system. It improves

the speed, accuracy and consistency of data capture,

analytics and the storage of financial and non-financial

information on counterparties.

PROFESSIONAL SERVICES

Moody’s KMV offers services that help clients

customize their credit risk management systems.

Clients can benefit from three areas of expertise:

Advisory Services provides counsel on how best to

optimize a client’s credit risk management practices

from risk evaluation to active portfolio management.

.10

.05

.01

07/12/06 08/23/06

10/04/06

11/15/06

12/27/06

02/07/07

03/21/07

05/02/07

06/13/07

Sample Company EDF

Industry Peer Group EDF

Data: Moody’s KMV database, used for all of our models, is

the most comprehensive in the industry containing information

on both public and private institutions around the world. The

Moody’s KMV CRD® (Credit Research Database) of private

company data is routinely cleansed and filtered to ensure that

only the highest quality data is used in our solutions.

Modeling Services develops models and provides the

EDF measures: Moody’s KMV is the inventor of EDF

validation and calibration of internal credit risk models.

(Expected Default Frequency) measures. More granular and

mathematical than ordinal ratings, clients consider EDF

measures to be the most powerful and forward-looking in the

industry for forecasting default probabilities. The most recent

model version (EDF 8.0) comprises more than 30,000 public

companies globally, scoring them daily on a scale of .01 to 35

percent, as determined by enterprise value, enterprise volatility

and liability structure. Private company EDF measures are

built on financial statement data reflecting a number of

variables including profitability, activity, leverage, liquidity,

size, growth variables and debt coverage.

Implementation Services works with clients to plan

software customization and the installation of credit

risk management solutions into their existing systems.

Caa

.20

B

Baa

A

Aa

Aaa

North and South America

+1 (866) 321-MKMV (6568) or +1 (415) 874-6000

Europe, the Middle East and Africa +44 (20) 7280-8300

Asia-Pacific

+852 3551-3000

Japan

+81 (3) 3218-1160

E-mail

info@mkmv.com

www.moodyskmv.com

Copyright © 2007 Moody’s KMV Company. All rights reserved. Unless otherwise designated,

all trademarks are owned by MIS Quality Management Corporation and used under license.