Optimal Credit Limit Management

advertisement

Optimal Credit Limit

Management

presented by

Markus Leippold

joint work with

Paolo Vanini and Silvan Ebnoether

Collegium Budapest - Institute for Advanced Study

September 11-13, 2003

Introduction

A. Background

Main Applications of Credit Risk Models:

• Pricing of credit risky securities:

– Corporate bonds, swaps, and vulnerable securities.

– collateralized bond obligations (CDOs’), basket credit derivatives (ith-todefault swap).

• Credit risk management:

– Computation of loss distribution and associated risk measures (such as

VaR, coherent measures, ...) for portfolios of defaultable bonds and loans.

– Determination of risk capital.

2

B. Motivation

What happens during market downturns?

• Credit derivatives become very costly.

• Credit portfolio diversification cannot be pursued to the extend required.

• Banks stick to short-term policies to control credit exposure.

How to achieve a short-term control?

• Banks decrease the credit limits for their debtors.

• Examples are numerous: Swiss (UBS, Credit Suisse), ANZ ”de-risking” strategy for corporate debt portfolios.

V Our goal is to analyze the optimal credit limit policy.

3

C. Preview

• Credit risk model as a two players game (bank and firm) in continuous time

to obtain and analyze optimal limit policy :

– closely linked to structural models, but with endogenous firm value;

• We develop the model in three steps:

– Model for Non-Defaultable Firms

∗ We analyze the risk/return profile, the optimal credit usage, and the

optimal limit policy.

– Model with Partial Information

∗ We analyze the effect of the volatility of the signal.

∗ Adverse selection and pooling.

– Contracting under Partial and Incomplete Information

∗ Removal of pooling effects,

∗ Design of optimal contract,

∗ Why some banks attract “bad debtors”.

4

Model Basics

A. The Economy

• Financial market defined on (Ω, F, P) with a terminal time T .

• Uncertainty is driven by a one dimensional Brownian motion {Wt, Ft; 0 ≤

t ≤ T }.

• The economy is populated by two agents B and C.

• Agent C demands credit, agent B supplies credit. Therefore, we call C “a

company”, and agent B “a bank”.

• Both agents optimize their value function, taking into account the optimizing

behavior of the other agent.

5

B. Agent C - The Company

• The company maximizes her final surplus,

ST = AT − LT .

• Surplus dynamics

dSt = µ0dt + σ0dWt, S0 ≥ 0.

• The company can demand a credit amount ctSt, provided by agent B.

• The demand ctSt is limited by `t, the credit limit imposed by bank B.

• This additional amount of money can be invested such that

dSt = (µ0 + (µ1 − p)ct) dt + (σ0 + σ1ct) dWt,

where

ct

p

µ1

σ1

:

:

:

:

credit demand as a fraction of surplus St;

cost of credit;

mean of new investment;

volatility of new investment.

6

(cont’d)

Agent C solves

(C0)

:

hR

i

T −δ(T −s)

V (S, t) = maxct E t e

Ssds |Ft ,

h

i

RT

s.t. var t Ssds |Ft ≤ ς 2,

ctSt ≤ `t , ∀t ∈ [0, T ],

0 ≤ ct, ∀t ∈ [0, T ],

dSt = (µ0 + (µ1 − p)ct) dt + (σ0 + σ1ct) dWt.

à (C0) is not separable in the dynamic programming sense.

à Embedding technique (Li and Ng (2000); Leippold, Trojani, and Vanini

(2001)) gives a separable problem:

¸

·Z T

¡

¢

(C1) : V (S, t, ω, λ) = max E

e−δ(T −s) λSs − ωSs2 ds |Ft .

ct ∈C(S)

t

à Choosing ω, λ appropriately, then, if c∗ solves (C1), it also solves (C0).

7

C. Agent B - The Bank

• The bank maximizes expected earnings minus capital costs from her credit

lending business and solves

T

Z

(B1) : J(S, t) = max E e−δ(T −s) (pcsSs − κ`s) ds |Ft

`t

s.t.

t

dSt = (µ0 + (µ1 − p)ct)dt + (σ0 + σ1ct)dWt,

`t ≥ 0, ∀t ∈ [0, T ].

Hence, the bank optimizes the limit amount ` over the duration T − t.

• Following regulatory practice, the capital costs κ are calculated on the limit

amount set-off for the client and not on the actual credit exposure!

8

D. Problem Characteristics

• Problems (C1) and (B1) define a non-cooperative game, where the decision

of each player affects the value function of the other one.

• Solution Concept:

– Subgame-perfect Nash equilibrium (SPNE):

A pair (c∗, `∗) is a Nash equilibrium if

J(S, t, c∗, `∗) ≥ J(S, t, c∗, `) , V (S, t, c∗, `∗) ≥ V (S, t, c, `∗)

for any feasible policies c and ` and where c∗ (`∗) is the optimal

strategy of C (B).

– (c∗, `∗) depend on the state S and time t.

9

Model for Non-Defaultable Firms

A. The Result

Proposition 1. Consider an economy with two players solving (C1) and

(B1), respectively. The strategies

µ ∗ ¶

¡

¢

`

c∗t = max t , 0 , `∗t = max γ1St + γ2St2, 0 ,

St

are a subgame perfect Nash equilibrium, where γ1 and γ2 are constants.

The value functions read

¡

¢

J(S, t) = e−δ(T −t) (p − κ) b0 + b1St + b2St2 ,

¡

¢

−δ(T −t)

2

V (S, t) = e

k0 + k1St + k2St ,

Note: The parameter κ ( = costs for providing limit) does not enter the optimal

limit policy.

10

B. Discussion “Non-defaultable Firm”

√

δ (µ1 −p+ δσ1 )

δσ0 σ1 −µ0 (µ1 −p) :

• Critical level of financing Sc =

(

0 σ1

< 0, if µ0 > δσ

µ1 −p > 0,

Sc

0 σ1

> 0, if 0 < µ0 < δσ

µ1 −p ,

(1)

Thus, Sc > 0 becomes more likely, when

a) the difference between the mean of the investment opportunity µ1 and

the costs of the credit becomes small,

b) the volatility of both investments, σ0 and σ1, are large,

c) the time preference parameter δ is large.

• The surplus is convex (concave) in `∗, if γ2 > 0 (γ2 < 0).

• The surplus dynamics follows a stationary process if and only if

(µ1 − p)γ2 > 0.

11

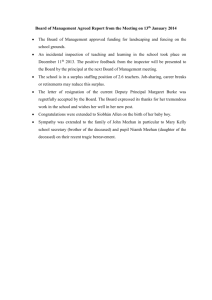

(B)

(A)

8

γ >0

1.2

2

1.15

7

surplus

1.1

6

1.05

1

0.95

0.9

5

γ2 < 0

γ2 > 0

4

50

100

150

200

250

200

250

days

(C)

3

1.5

γ <0

2

γ >0

2

1.4

2

1.3

optimal limit

optimal limit

0.85

1.2

1.1

1

1

surplus

0.9

0

0.8

γ <0

2

0.7

0.6

−1

0

2

4

6

8

50

surplus S

100

150

days

Figure 1: Optimal limit policy.

12

Model with Partial Information

A. Problem Motivation

• Bank B has only partial information about the true surplus of company C

(Enron, WorldCom, Swissair).

• B makes a “best guess” Ŝ of the company’s surplus.

• The guess might be based on the credit usage ct.

• The signal ζt = St + “noise” follows

(O)

:

dζt = (A0 + A1St) dt + BdZt.

• The Brownian motions Wt and Zt are independent, Ŝt is Gt-measurable,

where

Gt = σ {Zs : 0 ≤ s ≤ t} .

• Again, the firm is non-defaultable.

13

B. The Company’s Decision

• C knows that bank B obtains a noisy signal of the current surplus. C solves

·Z T ³

¸

´

(C2) : V (S, t, ω, λ) = max E

e−δ(T −s)λSs − ωSs2 ds |Ft .

ct ∈C(Ŝt )

t

• The optimal ct is given by

µ

c∗t = max

`∗t

Ŝt

¶

,0 .

• The state variable St evolves according to

(U)

:

dSt = (µ0 + (µ1 − p)c∗t ) dt + (σ0 + σ1c∗t ) dWt.

• Note that:

– we replaced C(St) by C(Ŝt),

– the conditional distribution Fct0 = P (St ≤ k|Gt) is (P-a.s.) Gaussian.

14

C. The Bank’s Decision using Kalman Filter

• Bank obtains signal ζt and makes a best guess

Z

n h

h

i

i¯

o

2

2

2 ¯

2

|St − Ŝt| dP = E |St − Ŝt| = inf E |Ŝt − Y | Y ∈ L (G, P) ,

Y

Ω

with (Ω, F, P) the probability space for (Wt, Zt) and E(·) denotes the expectation w.r.t. P.

Proposition 2. Given equations (U) and (O), the process Ŝt follows

µ

¶

A21

A1

dŜt = µ0 + (µ1 − p)ct + ρt 2 (St − Ŝt) dt + ρt dZt, Ŝ0 = E [S0] ,

B

B

where ρt solves a Riccati equation.

à Ŝ dynamics are nonlinear.

à We use perturbation theory to maintain analycity of the bank’s value function

J(Ŝ).

15

Perturbation Step 1: Linearize ρt

We use a first-order approximation

(1)

ρt ,

such that ρt =

(1)

ρt

³

2

´

+ O (ctσ1) , i.e.,

(1)

ρt = r0(t) + r1(t)ct.

Perturbation Step 2: J-function

• The optimization problem for the bank reads

T

Z

³

´

−δ(T

−s)

pcsŜs − κ`s ds |Gt .

(B2) : J(Ŝ, t) = max E e

`t ∈B(Ŝ)

t

• The HJB for (B2) cannot be solved in closed form.

• We assume that B is competent enough such that

• Then, we expand the J-function around

16

St −Ŝt

St

∼ 0.

St −Ŝt

St

is close to 0.

D. The Result

Proposition 3. Consider an economy with two players solving (B2) and

(C2), where player B has only partial information on C’s surplus. Then,

the strategies

Ã

!

µ ∗ ¶

St − Ŝt

`

(1)∗

ct

= max t , 0 + O

,

S

t

Ŝt

!

Ã

³

´

St − Ŝt

(1)∗

`t

= max γ̂1(t)Ŝt + γ̂2(t)Ŝt2, 0 + O

,

St

are a subgame perfect Nash equilibrium.

We note:

• The value function of B and C are again quadratic, but in Ŝ.

• Partial information introduces time-dependent parameters.

• Differences in optimal policies given by changes in the volatility terms:

A1

A1

σ0 → r0(t) , σ1 → r1(t) .

B

B

• Already to first-order, the differences in the models are significant!

17

Partial Information and Adverse Selection

low signal variance

medium signal variance

high signal variance

2

2

2

1.5

1.5

1.5

A

optimal limit

2.5

optimal limit

2.5

optimal limit

2.5

A

1

1

1

0.5

0.5

0.5

0

0

0.5

1

1.5

surplus

2

2.5

0

0

0.5

1

1.5

surplus

2

2.5

0

0

0.5

1

1.5

2

2.5

surplus

Figure 2: The influence of signal variance for low µ1 (µ1 = 5%). We make the following assumptions: µ0 =

2%, σ0 = 10%, σ1 = 30%, δ = 5%, p = 1%. For the signal process ζt we assume A1 = −0.2. As ‘low signal

variance’ we choose B = 7.5%, for ‘medium signal variance’ B = 20%, and for ‘high signal variance’ B = 50%. The

bold dashed line is the satiation level. The thin dashed line denotes the optimal limit policy with full information.

Finally, the bold straight line is the optimal limit policy under partial information.

18

low signal variance

medium signal variance

1.2

high signal variance

1.2

1.2

A

A

1

A

0.6

1

0.8

optimal limit

0.8

optimal limit

optimal limit

1

0.6

0.8

0.6

0.4

0.4

0.4

0.2

0.2

0.2

0

0

0.5

surplus

1

0

0

0.5

surplus

1

0

0

0.5

1

surplus

Figure 3: The influence of signal variance for high µ1 (µ1 = 10%). We make the following assumptions: µ0 =

2%, σ0 = 10%, σ1 = 30%, δ = 5%, p = 1%. For the signal process ζt we assume A1 = −0.2. As ‘low signal

variance’ we choose B = 7.5%, for ‘medium signal variance’ B = 20%, and for ‘high signal variance’ B = 50%. The

bold dashed line is the satiation level. The thin dashed line denotes the optimal limit policy with full information.

Finally, the bold straight line is the optimal limit policy under partial information.

19

Optimal Contracting

A. Problem Motivation

• Partial information introduces adverse selection effects.

• Optimal limit policy for high and low signal variances is possibly reduced

considerably, compared to case with full information.

• Low surplus reduces bank’s utility from providing credit.

• Firm has vital interest in obtaining large limits.

20

B. Basic Mechanisms

Firm:

• Has to undertake some costly effort to diminish noise acting on true state.

• Reducing noise reduces signal variance.

Bank:

• Cannot observe the firm’s effort.

• To differentiate between high and low efforts, bank sets up a contract:

– Bank rewards efforts by using a compensation scheme K.

– Contract needs to be incentive compatible for the firm and be at least as

good as the next best opportunity.

Credit demand c(ε) and the payment K(ε) has to satisfy the following requirements:

1. Incentive constraint (IC).

2. Rationality constraint (PC).

21

C. The Bank’s Decision

The primary formal model with incomplete and partial information reads:

·Z T

¸

´

³

f

(B3)

: J(Ŝ, t) = max E

e−δ(T −s) pĉsŜs(ε) − κ`s − K(ε) ds|Gt .

`∈B̂,K∈K

subject to

·Z

t

¸

¡

¢

ε∗, c∗t ∈ argmaxct∈C,ε

e−δ(T −s) λSs(ε) − ωSs2(ε) + K(ε) ds |Ft ,

ˆ E

t

·Z T

¸

¡

¢

ū ≤ E

e−δ(T −s) λSs(ε) − ωSs2(ε) + K(ε) ds |Ft ,

T

(IC)

(PC)

t

dSt = (µ0 + (µ1 − (p + ε))ct)dt + (σ0 + σ1ct)dZt, .

f generalizes the standard theory of contracts with hidden inThe program (B3)

formation:

f is a dynamic program.

1. (B3)

2. The state variable S is not observable for the bank. Instead, there is a noisy

signal. This defines partial information about the state variable.

22

D. Solution

Proposition 4. With J C and J B the value functions of the firm and bank,

the optimality conditions are:

∂J B (Ŝ) ∂J C (Ŝ) 1 − F (²) ∂ 2u1(y(ε))

+

=

AŜ J +

+ ∆AŜ J B

| {z } | ∂ĉ {z ∂ĉ }

| {z }

f (²)

∂ε∂ĉ

|

{z

}

(B )

(B )

B

1

(A)

2

(C)

where AŜ is the generator of the filter state dynamics Ŝ without incomplete

∂

is the generator corrections due to incomplete

information, ∆AŜ = εĉ ∂ĉ

information.

Summarizing:

static

information complete/partial

incomplete/partial

23

(A)

(A) + (C)

time

dynamic

(A) + (B1 )

(A) + (B1 ) + (C) + (B2 )

E. Interpretation

à Bank faces tradeoff between maximizing surplus (A) and appropriating the

firm’s information rent (C).

à In a static economy, the optimum is obtained when an increase in surplus

equals the expected increase in agent C’s rate.

à When ² = ²̄, (C) = 0 and the company’s effort is of no concern. Only (A)

is maximized (“no distortion at the top”).

à Within a dynamic setup, two additional terms appear:

B1 : The generator of the filter state dynamics Ŝ without incomplete information

B2 : A dynamic hedging component against incomplete information on ².

24

(cont’d)

à The impact of (C) on the bank’s marginal utility function depends on the

2 (y(ε))

1

sign of the cross-derivative term ∂ u∂ε∂ĉ

. If the effort ε and the credit usage

c are

– substitutes, (C) > 0. The information rent to be payed by the bank

is decreasing, when the effort ε is increasing. High efforts imply a low

information rent. As the information rent is negative, high efforts increase

the bank’s utility. .

– complements, (C) < 0. The bank obtains a positive information rent.

This information rent will become even more positive and inducing a

higher utility for the bank if the firm’s effort is decreased. Hence, the

bank has an interest to attract “bad debtors”.

25

Summary

• Endogenous firm values can be analyzed in closed-form using a subgame

perfect Nash equilibrium.

• Possibility of credit usage may alter statistical properties of surplus dynamics.

• Partial information leads to adverse selection/pooling.

• Design of optimal contract.

• Rationalizing “bad” debt.

...proposal for future research:

1. Multiple companies demanding credit.

2. Allowing for default.

3. Embedding credit rating.

26