Engro Foods Limited An emerging growth story

advertisement

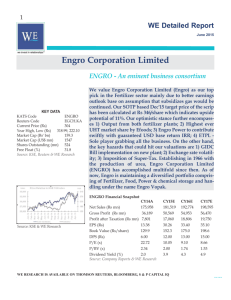

Engro Foods Limited An emerging growth story With a growing population (2010 growth rate: 2.05%) the demand for processed food is anticipated to grow in the coming years. This is what Engro Foods has been doing and aims to capitalize on going forward. Penetrating and diversifying into different areas of high quality dairy segment, Engro Foods first tuned into profits in 2010. Now with a strong foothold in the UHT milk, ice cream and further potential for tapping the growing demand within the segments, the company is set to be listed on the stock exchange. The offer price is set at Rs25 per share. Based on a DCF valuation of Rs35 per share, we recommend ‘Subscribe’ on the stock as it offers a potential upside of 40% to our target price. Initiating Coverage: Target Price: SUBSCRIBE Rs35 June 2011 JS Global Capital Limited What’s on offer? Engro Corp (ENGRO) is planning to offer 27mn shares (3.6% of the total paid up capital) of Engro Foods to the general public at Rs25 per share. Subscription dates are July 5-7, 2011. The company has already raised Rs1.2bn (48mn share at Rs25 each) through pre IPO to foreigners and local institutions. Product Portfolio: Ambient UHT to ice cream to rice Since its inception in 2006, Engro Foods has been a story of growth and diversifying its base into high quality dairy products. Engro Foods started its business with a launch of all purpose (Olpers) milk and cream. The company then expanded into liquid tea whitener (Tarang) and cooking oil (Tarka) in 2007. Since then, the company’s market share in the ambient UHT market has grown many folds to 39% and currently holds the position of a market leader. The aggressive approach continued in 2009 with the launch of Omore ice cream and flavored milk (Owsum) followed by fruit juices (Olfrute: 1% market share) and powder tea whitener in 2010. The new addition to its exquisite product line is the rice business (mainly export oriented) and its Global business unit (GBU) Al Safa, a Halal meat brand in North America. Al Safa is currently held under ENGRO’s books and will eventually be bought by Engro Foods, subject to SBP approvals. Offer Price: Rs25 Offer size: General Public: 27mn shares Pre-IPO: 48mn shares Subscription Dates: General Public: 5-7th Jul 2011 Key numbers 2010A 2011E 2012F 2013F 2014F EPS (Rs) 0.2 1.0 1.8 2.9 4.6 PBV (x) 3.6 2.3 1.9 1.6 1.2 PE (x) NM 25.2 13.5 8.6 5.4 Price/sales (x) 0.9 0.6 0.4 0.3 0.3 Source: JS Research Profits to post a 4 year (2011-15) CAGR of 65% We project the company’s earnings to grow at a 4 year (2011-2015) CAGR of 65% to Rs5.5bn driven by untapped ambient UHT milk demand in the country. Out of the total processed milk market (only 7% of total the country’s milk production), ambient UHT milk segment comprises of a mere 4%. Furthermore, strong advertising effort to penetrate into the markets of existing products (ice cream and juices) is also likely to play its role. Valuation: 40% upside to the offer price of Rs25 Using the DCF methodology with a risk free rate of 14.0% and cost of equity of 19.7%, our fair value for Engro Foods arrives at Rs35, which implies a 40% upside to the offer price of Rs25 per share. Our liking for Engro Foods is also backed by the company’s 2011E Price to sale of 0.6x which when compared to Nestlé’s (its closest peer) average historic multiple is at a deep discount of 67%. Completed on June 30, 2011 – Distributed on June 30, 2011 Bilal Qamar Analyst bilal.qamar@js.com 92 (21) 111-574-111 (Ext: 3099) JS Research is available on Bloomberg, Thomson Reuters and CapitalIQ Please refer to the important Disclaimer on the last page Engro Foods Limited Page 2 Engro Foods – what it offers? Engro Foods was formed as a wholly owned subsidiary of ENGRO (formerly known as Engro Chemical Pakistan Limited) in 2006. In a short period of 5 years, the company has gained a strong foothold in UHT milk, powder and the ice cream businesses and looks to diversify its high quality dairy based products. Within this period, Engro foods Supply Chain (Pvt) Limited was created to look after the supply chain of the business. It is a 70% owned subsidiary of Engro Foods and the remaining 30% is owned by Engro Eximp. To top it all up, Engro Foods also set up a rice plant in Muridke (Punjab) under Engro Foods Supply Chain (Pvt) Limited (EFSC). Processed milk – an ever growing segment Engro Foods business started with the processed milk segment which they currently dominate in terms of market share (39%), overtaking Nestlé in 2010. This segment offers a great opportunity for growth as it constitutes a mere 7% (1.4bn litres) of the total trade-able milk. A further break up of the segment reveals that only a 4% of the total processed milk is used in the Ambient UHT milk segment, 2.6% in Powder and the rest in Chilled Dairy. Country’s total milk consumption (mn litres) Milk Prod uction 38,000 Wastage 6,000 Farmer Tradeable Retention 20,685 (100% ) 11,315 Unprocessed Processed Milk Milk 19,250 (93%) Gawala 8,450 (41%) Milk Shops 7,300 (35%) Source: Company presentation June 2011 1,435 (7%) Industrial Sweets 3,500 (17%) Ambient UHT 795 (4%) Powder 540 (2.6%) Chilled Dairy 100 (0.5%) Engro Foods Limited Ambient UHT milk – This section mainly comprises of Engro Foods (Olpers, Tarang, Owsum and Olper’s cream) and Nestlé constituting ~71% of the total market share. Engro Foods currently lead the market with a share of 39% with strong growths coming in from Tarang and Olpers. Powder Milk – Engro Foods entered the whitening powder business in mid 2010 and gained a single ppt of market share during the year. Nestlé currently dominates the market, however aggressive advertisement campaign by Engro Foods on this front can create a niche market for Tarang Powder as in the case of liquid tea whitener. More so, the company also plans to enter the growing up powder milk business which is currently dominated by Nido (Nestlé). Juices – Olfrute juices were launched in mid May 2010 and the company currently faces strong competition from Nestlé (already a market giant with 66% share) and Shezan (19% market share). With the help of its strong marketing chain, the company is well positioned to make inroads into the juices and nectar market. Furthermore, rising health awareness among the urban population can trigger a growth potential in this sector. Ice cream Omore (Engro Foods ice cream brand) - since its launch in 2009 – has been able to deeply penetrate into the market and achieve a commendable market share of 17%. Omore’s launch in Karachi (the biggest ice cream market accounting of 23% of the total market demand) was delayed due to pure dairy nature of the ice cream. Nevertheless, Omore was finally launched in the city during the current year which saw its revenue soaring by 96% in 1Q2011. The brand is still in its development stage and efforts are being made by the company to establish its brand loyalty through heavy marketing expenditures. That is why the segment has still been in losses so far. Going forward, we expect the segment’s revenues to witness a 4 year (2011-15) CAGR of 17% and to post profits from next year. Rice Business – unlocking international presence As per the latest numbers released in the economic survey, rice accounts for 0.9% of the GDP and is amongst the major crops being sown in Pakistan. Pakistan is one of the largest exporters of rice with the most popular type being Basmati. With ENGRO’s vision of tapping the international market, Engro Foods has set up a rice plant through EFSC to refine and process rice for Engro Eximp. The plant has an initial processing capacity of 28k tons which is expected to double in 2011. EFSC has a ‘Take or Pay’ agreement with Engro Eximp for rice export and a guaranteed 18% IRR on assets while risks will be borne by Engro Eximp. Global Business Unit – Al Safa Continuing with a global vision, ENGRO has acquired Al Safa at an acquisition price of US$6.3mn. Due to SBP’s terms and conditions the ownership remains under ENGRO which eventually be transferred to Engro Foods at cost. Al Safa is the oldest Halal meat brand in North America and the company aims to target Muslim population through Halal and Ethnic Food segments. This can further broaden the aspects of the company to establish itself in the international market. June 2011 Page 3 Cur r ent ambient UHT mk t. s har e 14% 39% 15% 32% Engro Foods Nestle Haleeb Rest So urce: Co mpany presentatio n Cur r ent juic es ' mar k et s har e 14% 1% 19% 66% Engro Foods Nestle So urce: Co mpany presentatio n Shezan Rest Engro Foods Limited Page 4 Profitability; 4 year (2011-15) CAGR of 65% We project the company’s earnings to grow at a 4 year (2011-2015) CAGR of 65% to Rs5.5bn driven by untapped ambient UHT milk demand in the country. Furthermore, the company’s continuous efforts to diversify its product base and add value to its existing portfolio seconds our view. Revenues from the ambient UHT milk segment along with juices are expected to grow at a 4 year (2011-15) CAGR of 28%. Engro Foods market share in the ambient UHT milk segment is expected to grow to 49% from the existing 39%. Further growth is witnessed in the ice cream segment where the market share is expected to grow to 20% in 2015 from the existing 17%. Keeping in mind the growing revenues and attainment of economies of scales, company’s gross margins are expected to rise to 25.3% from 20.9% in 2010. Segmented revenue (Rs mn) Net profit (Rs mn) 100,000 Others 6,000 80,000 Ice cream 5,000 60,000 Dairy 4,000 3,000 40,000 2,000 20,000 1,000 0 0 2010 2011 2012 2013 2014 2015 2010 Source: JS Research Valuation: 40% upside to the offer price of Rs25 Using the DCF methodology with a risk free rate of 14.0% and cost of equity of 19.7%, our fair value for Engro Foods arrives at Rs35, which implies a 40% upside to the offer price of Rs25 per share. Our liking for Engro Foods is also backed by the company’s 2011E Price to sale of 0.6 which when compared to Nestlé’s (its closest peer) average historic multiple is at a deep discount of 67%. Pr ic e to s ales ( x ) Pr ic e to ear nings ( x ) 0.70 0.60 0.50 0.40 0.30 0.20 0.10 0.00 30 June 2011 20 15 10 So urce: JS Research 2015F 2014F 2013F 2012F 0 2011E 2015F 2014F 2013F 2012F 5 2011E 2012 2013 2014 2015 Valuations (Rs mn) PV of cashflows 7,683 Terminal value 18,304 Total present value 25,987 No of shares (mn) 748 Target price (Rs) 35 Source: JS Research 25 So urce: JS Research 2011 Source: JS Research Engro Foods Limited Page 5 Financial highlights (Rs m n) 2010A 2011E 2012F 2013F 2014F 2015F Net sales 20,945 31,282 42,163 55,720 68,567 80,978 COGS 16,552 24,381 32,530 42,824 52,047 60,471 4,393 6,900 9,633 12,895 16,520 20,507 930 1,930 3,458 4,807 6,820 9,372 1,630 2,717 4,877 7,105 9,655 12,470 Incom e State m e nt Gr os s pr ofit Operating prof it EBITDA Financial charges 660 789 1,333 1,475 1,491 956 PBT 270 1,141 2,125 3,332 5,329 8,416 Tax 94 399 744 1,166 1,865 2,946 PAT 176 742 1,381 2,166 3,464 5,470 Shar e holde r's Equity 5,124 8,216 9,597 11,763 15,227 20,697 Non current liabilities 4,814 5,607 8,999 8,696 6,386 4,486 Current liabilities 2,522 5,740 11,192 14,767 17,396 15,696 12,460 19,563 29,788 35,226 39,009 40,879 8,722 15,075 24,211 29,953 32,979 34,000 Balance She e t Total Liabilitie s & Equity Non current assets Total current assets 3,738 4,488 5,577 5,273 6,030 6,879 12,460 19,563 29,788 35,226 39,009 40,879 Earning per share 0.2 1.0 1.8 2.9 4.6 7.3 Book value per share 6.9 11.0 12.8 15.7 20.4 27.7 Price to earning ratio (x) NM 25.2 13.5 8.6 5.4 3.4 Price to book value (x) 3.6 2.3 1.9 1.6 1.2 0.9 Price to sales (x) 0.9 0.6 0.4 0.3 0.3 0.2 21% 22% 23% 23% 24% 25% Operating margin 4% 6% 8% 9% 10% 12% Pretax margin 1% 4% 5% 6% 8% 10% Net margin 1% 2% 3% 4% 5% 7% 0.4 0.3 0.4 0.4 0.4 0.2 Total debt to equity 0.9 0.8 1.4 1.2 0.9 0.4 Long term debt to equity 0.9 0.7 0.9 0.7 0.4 0.2 Interest cover 1.4 2.4 2.6 3.3 4.6 9.8 ROE 3% 9% 14% 18% 23% 26% ROA 1% 4% 5% 6% 9% 13% Total As s e ts Ratio Analys is V aluation Pr ofitability Gross margin Solve ncy Total debt to total assets M om e ntum Sales grow th 43% 49% 35% 32% 23% 18% Net prof it grow th NM 322% 86% 57% 60% 58% Source: Company prospectus & JS Research June 2011 Research Team Muzzammil Aslam Economy & Politics (92-21) 111574111 (ext. 3035) muzzammil.aslam@js.com Umer Bin Ayaz Strategy, E&P, Refinery & Power (92-21) 111574111 (ext. 3103) umer.ayaz@js.com Syed Atif Zafar OMCs, Cement, Autos & Chemicals (92-21) 111574111 (ext. 3118) atif.zafar@js.com Mustufa Bilwani Banks & Telecom (92-21) 111574111 (ext. 3100) mustufa.bilwani@js.com Bilal Qamar Fertilizer, Insurance & Textile (92-21) 111574111 (ext. 3099) bilal.qamar@js.com Sana Hanif Chemicals (92-21) 111574111 (ext. 3102) sana.hanif@js.com Rabia Tariq Textile & Paper&Board (92-21) 111574111 (ext. 3119) rabia.tariq@js.com Raheel Ashraf Technical Analyst (92-21) 111574111 (ext. 3098) raheel.ashraf@js.com Adeel Jafri Database Manager (92-21) 111574111 (ext. 3098) adeel.jafri@js.com Muhammad Furqan Librarian (92-21) 111574111 (ext. 3105) muhammad.furqan@js.com (92-21) 32799511 junaid.iqbal@js.com Murtaza Jafar (92-21) 32799516 murtaza.jafar@js.com M. Jawad Khan (92-21) 32799518 jawad.khan@js.com Ahmed Abdul Rauf (92-21) 32799518 ahmed.rauf@js.com Asim Ali (92-21) 32799509 asim.ali@js.com Mujtaba Barakzai (92-21) 32800152 mujtaba.barakzai@js.com Abdul Aziz (92-21) 32799507 abdul.aziz@js.com Irfan Iqbal (92-21) 32799502 irfan.iqbal@js.com Irfan Ali (92-21) 32462567 irfan.ali@js.com Equity Sales Junaid Iqbal Head Office KSE Office Lahore Office Islamabad Office Hyderabad Office 6th Floor, Faysal House 2nd Floor, Room No.75, Ground Floor, Room No.413, 4th Floor Office M-7, Rabbi Center, Main Shahra-e-Faisal Karachi Stock Exchange 307 – Upper Mall ISE Towers, 55-B, Jinnah adj. Belair Hospital, Cantt. Karachi, Pakistan Stock Exchange Rd, KHI Lahore, Pakistan Avenue, Islamabad. Saddar, Hyderabad Tel: +9221 111-574-111 Tel: +9221 32425692 Tel: +9242 111-574-111 Tel: +9251 111-574-111 Tel: +9222 111-574-111 Fax: +9221 32800163,66 Fax: +9221 32418106 Fax: +9242 35789109 Fax: +9222 2720581 Fax: +9251 2806328 Website: www.js.com JS Global Capital Limited ANALYST CERTIFICATION I, Bilal Qamar, the author of this report, hereby certify that all of the views expressed in this research report accurately reflect my personal views about any and all of the subject issuer(s) or securities. I also certify that no part of my compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. DISCLAIMER This report has been prepared for information purposes by the Research Department of JS Global Capital Limited. The information and data on which this report is based are obtained from sources which we believe to be reliable but we do not guarantee that it is accurate or complete. In particular, the report takes no account of the investment objectives, financial situation and particular needs of investors who should seek further professional advice or rely upon their own judgment and acumen before making any investment. This report should also not be considered as a reflection on the concerned company’s management and its performances or ability, or appreciation or criticism, as to the affairs or operations of such company or institution. JS Global does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Warning: This report may not be reproduced, distributed or published by any person for any purpose whatsoever. Action will be taken for unauthorized reproduction, distribution or publication.