Practice Quiz 3: Bonds

advertisement

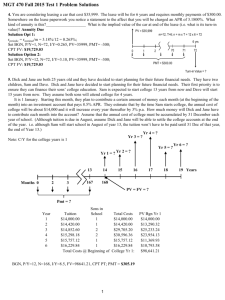

Practice Quiz 3: Bonds 1. This question has two parts. a. What is the price of a 20-year, zero-coupon bond with a 5.1% yield and $1,000 face value? By hand: PV = $1000 (1 + 0.051) 20 = $369.78 On the HP-12C: n = 20 i = 5.1 PMT = 0 FV = 1000 So PV = -369.78 b. Take the above bond and add annual 4.8% coupons. What is the price of this new bond? By hand: PV = $48 ⎛ ⎛ 1 ⎞ ⎜⎜1 − ⎜ ⎟ 0.051 ⎝ ⎝ 1 + 0.051 ⎠ 20 ⎞ $1000 = $962.93 ⎟⎟ + 20 1 0.051 + ( ) ⎠ On the HP-12C: n = 20 i = 5.1 PMT = 48 FV = 1000 So PV = -962.93 2. What is the price of a 3-year, U.S. corporate bond with 3.4% coupon, a 3.6% yield, and a $1,000 face value? Remember that corporate bonds, just like Treasury bonds, pay semi-annual coupons. $17 ⎛ ⎛ 1 ⎞ By hand: PV = ⎜⎜ 1 − ⎜ ⎟ 0.018 ⎝ ⎝ 1 + 0.018 ⎠ 6 ⎞ $1000 = $994.36 ⎟⎟ + 6 1 + 0.018 ( ) ⎠ On the HP-12C: Foster MBA – Finance Jump Start – Thomas Gilbert n = 2*3 = 6 i = 3.6/2 = 1.8 PMT = 34/2 = 17 FV = 1000 So PV = -994.36 3. This question has two parts. a. What is the price of a 3-year Eurobond with 5% annual coupons, a face value of $1,000, and the following spot rates: r1 = 4.5%, r2 = 5.5%, and r3 = 6%? You have to solve this by hand: $50 $50 $1050 PV = + + = $974.37 2 1 + 0.045 (1 + 0.055 ) (1 + 0.06 )3 b. What is the yield-to-maturity of the above bond? You have to solve this using the HP-12C: n=3 PV = -974.37 PMT = 50 FV = 1000 So i = 5.96% Foster MBA – Finance Jump Start – Thomas Gilbert