Problem 14-46 (25 minutes)

advertisement

")

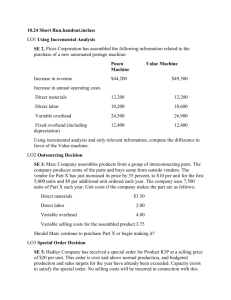

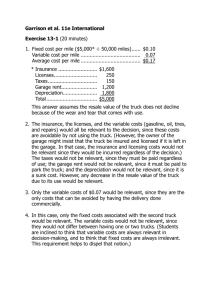

Select solutions to Chapter 14 PROBLEM 14-44 (25 MINUTES) 1. Contemporary Trends will be worse off by $6,400 if it discontinues wallpaper sales. Sales…………………….. Less: Variable costs…. Contribution margin…. Paint and Supplies Carpeting Wallpaper $190,000 114,000 $ 76,000 $230,000 161,000 $ 69,000 $ 70,000 56,000 $ 14,000 If wallpaper is closed, then: Loss of wallpaper contribution margin…... $(14,000) Remodeling……………………………………. (6,200) Added profitability from carpet sales*…… 32,500 Fixed cost savings ($22,500 x 40%)………. 9,000 Decreased contribution margin from paint and supplies ($76,000 x 20%)…………….. (15,200) Increased advertising……………………….. (12,500) Income (loss) from closure………………… $ (6,400) * The current contribution margin ratio for carpeting is 30% ($69,000 ÷ $230,000). This ratio will increase to 35%, producing a new contribution for the line of $101,500 [($230,000 + $60,000) x 35%]. The end result is that carpeting’s contribution margin will rise by $32,500 ($101,500 $69,000), boosting firm profitability by the same amount. 2. This cost should be ignored. The inventory cost is sunk (i.e., a past cost that is not relevant to the decision). Regardless of whether the department is closed, Contemporary Trends will have a wallpaper inventory of $11,850. 3. The Internet- and magazine-based firms likely have several advantages: These companies probably carry little or no inventory. When a customer places an order, the firm simply calls its supplier and acquires the goods. The result may be lower expenditures for storage and warehousing. These firms do not need retail space for walk-in customers. Internet- and magazine-based firms can conduct business globally. Contemporary Trends, on the other hand, is confined to a single store in Baltimore. PROBLEM 14-45 (50 MINUTES) 1. Sets result in a 20% increase, or 1,500 dresses (1,250 1.20 = 1,500). Complete sets .................................. Dress and accessory cape ............. Dress and handbag ......................... Dress only ........................................ Total units if additional items are introduced ...................................... Less: Unit sales if additional items are not introduced ......................... Incremental sales ............................ Incremental contribution margin per unit (excluding material and cutting costs) ................................. Total incremental contribution margin ............................................ Percent of Total Dresses 70% 1,050 6% 90 15% 225 9% 135 100% Total Number of Accessory Capes Handbags 1,050 1,050 90 225 1,500 1,140 1,275 1,250 250 -1,140 -1,275 $192.00 $48,000 Additional costs: Additional cutting cost (1,500 91% $14.40) ................ Additional material cost (250 $80.00) .............................. Lost remnant sales [(1,250 – 135) $8.00] ................. Incremental cutting for extra dresses (250 $32.00)....... Incremental profit ............................ 2. $12.80 $14,592 Total $4.80 $6,120 $68,712 $19,656 20,000 8,920 8,000 56,576 $12,136 Qualitative factors that could influence the company’s management team in its decision to manufacture matching accessory capes and handbags include: accuracy of forecasted increase in dress sales. accuracy of forecasted product mix. PROBLEM 14-45 (CONTINUED) company image of a dress manufacturer versus a more extensive supplier of women’s apparel. competition from other manufacturers of women’s apparel. whether there is adequate capacity (labor, facilities, storage, etc.). PROBLEM 14-46 (25 MINUTES) 1. Food Blender Processor Unit cost if purchased from an outside supplier ...................................... $60 Incremental unit cost if manufactured: Direct material ......................................................................................... $18 Direct labor ..............................................................................................12 Variable overhead $48 – $30 per hour fixed ......................................................................18 $96 – (2)($30 per hour fixed) ............................................................... Total ...................................................................................................... $48 Unit cost savings if manufactured ............................................................. $12 Machine hours required per unit ............................................................... 1 Cost savings per machine hour if manufactured $12 ÷ 1 hour ............................................................................................. $12 $18 ÷ 2 hours ........................................................................................... $114 $ 33 27 36 $ 96 $ 18 2 $ 9 Therefore, each machine hour devoted to the production of blenders saves the company more than a machine hour devoted to food processor production. Machine hours available .................................................................................... Machine hours needed to manufacture 20,000 blenders ................................. 50,000 20,000 Remaining machine hours ................................................................................. 30,000 Number of food processors to be produced (30,000 ÷ 2) ................................ 15,000 Conclusion: Manufacture Manufacture Purchase PROBLEM 14-46 (CONTINUED) 2. 20,000 blenders 15,000 food processors 13,000 food processors If the company’s management team is able to reduce the direct material cost per food processor to $18 ($15 less than previously assumed), then the cost savings from manufacturing a food processor are $33 per unit ($18 savings computed in requirement (1) plus $15 reduction in material cost): Food Blender Processor New unit cost savings if manufactured ......................................... $12.00 $33.00 Machine hours required per unit .................................................... 1 MH 2 MH Cost savings per machine hour if manufactured $12 ÷ 1 hour ................................................................................. $33 ÷ 2 hours ............................................................................... $12.00 $16.50 Therefore, devote all 50,000 hours to the production of 25,000 food processors. Conclusion: Manufacture: 25,000 food processors Purchase: 3,000 food processors and 20,000 blenders PROBLEM 14-47 (25 MINUTES) 1. 2. Incremental unit cost if purchased: Purchase price ......................................................................................... Material handling ...................................................................................... Total .......................................................................................................... $ 45,000 9,000 $ 54,000 Incremental unit cost if manufactured: Direct material .......................................................................................... Material handling ...................................................................................... Direct labor ............................................................................................... Variable manufacturing overhead ($36,000 1/3) ................................. Total .......................................................................................................... Increase in unit cost if purchased ($54,000 – $39,600) ............................. $ 3,000 600 24,000 12,000 $ 39,600 $ 14,400 Increase in monthly cost of acquiring part RM67 if purchased (10 $14,400, as computed above) .......................................................... Less: rental revenue from idle space ......................................................... Increase in monthly cost ............................................................................. $144,000 75,000 $ 69,000 PROBLEM 14-47 (CONTINUED) 3. Contribution forgone by not manufacturing alternative product ............ Savings in the cost of acquiring RM67 (10 $14,400 as computed in requirement 1) ......................................... Net cost of using limited capacity to produce part RM67 ........................ $156,000 144,000 $ 12,000 PROBLEM 14-48 (20 MINUTES) The analysis prepared by the engineering, manufacturing, and accounting departments of Cincinnati Flow Technology (CFT) was not correct. However, their recommendation was correct, provided that potential labor-cost improvements are ignored. An incremental cost analysis similar to the following table should have been prepared to determine whether the pump should be purchased or manufactured. In the following analysis, fixed factory overhead costs and general and administrative overhead costs have not been included because they are not relevant; these costs would not increase, because no additional equipment, space, or supervision would be required if the pumps were manufactured. Therefore, if potential labor cost improvements are ignored, CFT should purchase the pumps because the purchase price of $102 is less than the $108 relevant cost to manufacture. Incremental cost analysis: Purchased components .................................................................. Assembly labor ................................................................................ Variable manufacturing overhead .................................................. Total relevant cost ........................................................................ Cost of 10,000 Unit Assembly Run Per Unit $ 180,000 $ 18 450,000 45 450,000 45 $1,080,000 $108 PROBLEM 14-49 (25 MINUTES) 1. Per-unit contribution margins: Standard Selling price………………………………….. Less: Variable costs: Direct material………………………… Direct labor…………………………….. Variable manufacturing overhead … Sales commission $375 x 10%; $495 x 10%…………. Total unit variable cost………………. Unit contribution margin…………………… Enhanced $375.00 $495.00 $42.00 22.50 36.00 $67.50 30.00 48.00 37.50 49.50 138.00 $237.00 195.00 $300.00 2. The following costs are not relevant to the decision: Development costs—sunk Fixed manufacturing overhead—will be incurred regardless of which product is selected Sales salaries—identical for both products Market study—sunk 3. Martinez, Inc. expects to sell 10,000 Standard units (40,000 units x 25%) or 8,000 Enhanced units (40,000 units x 20%). On the basis of this sales forecast, the company would be advised to select the Standard model. 4. Standard Enhanced Total contribution margin: 10,000 units x $237; 8,000 units x $300…. $2,370,000 Less: Marketing and advertising……………… 195,000 Income……………………………………………... $2,175,000 $2,400,000 300,000 $2,100,000 The quantitative difference between the profitability of Standard and Enhanced is relatively small, which may prompt the firm to look at other factors before a final decision is made. These factors include: - Competitive products in the marketplace Data validity Growth potential of the Standard and Enhanced models Production feasibility Effects, if any, on existing product sales Break-even points PROBLEM 14-50 (20 MINUTES) 1. When there is no limit on production capacity the Pro model should be manufactured since it has the highest contribution margin per unit. Basic Model Selling price ......................................................................... $116 Direct material ...................................................................... 32 Direct labor ........................................................................... 20 Variable overhead ................................................................ 16 Total variable cost ............................................................... $ 68 Contribution margin ............................................................ $ 48 2. Deluxe Model $130 40 30 24 $ 94 $ 36 Pro Model $160 38 40 32 $110 $ 50 When labor is in short supply the Basic model should be manufactured, since it has the highest contribution margin per direct-labor hour. Basic Model Contribution margin per unit .............................................. $48 Direct-labor hours required ................................................ 1 Contribution margin per direct-labor hour ........................ $48 Deluxe Model $36 1.5 $24 Pro Model $50 2 $25 PROBLEM 14-51 (25 MINUTES) Yes, the order should be accepted because it generates a profit of $68,100 for the firm. Note: The fixed administrative cost is irrelevant to the decision, because this cost will be incurred regardless of whether Mercury accepts or rejects the order. Selling price………………………………………………… Less: Direct material ($16.40 - $4.20)…………………... Direct labor………………………………………….. Variable manufacturing overhead (.5 hours x $15.00*)…………………………….. Unit contribution margin…………………………………. Total contribution margin (11,000 units x $7.30)…….. Less: Additional setup costs…………………………… Special device………………………………………. Net contribution to profit…………………………………. $31.50 $12.20 4.50 7.50 24.20 $ 7.30 $80,300 $7,400 4,800 12,200 $68,100 * Fixed manufacturing overhead: $1,500,000 ÷ 60,000 machine hours = $25.00 per hour Variable manufacturing overhead: $40.00 - $25.00 = $15.00 No, Mercury lacks adequate machine capacity to manufacture the entire order. Planned machine hours (5,000 hours x 3 months)…… 15,000 Current usage (15,000 hours x 70%)…………………….. 10,500 Available hours……………………………………………… 4,500 Required machine hours (11,000 units x .5 hours)…… 5,500 Options include the following: Sacrificing some current business in the hope that a long-term relationship with Venus can be established and proves to be profitable Acquiring more machine capacity Outsourcing some units Working overtime