ch16sm

advertisement

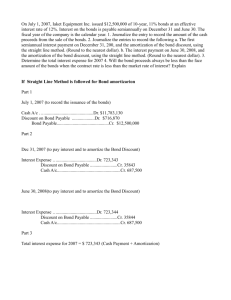

CHAPTER 16 Long-Term Liabilities ASSIGNMENT CLASSIFICATION TABLE Study Objectives Brief Exercises Questions Exercises Problems Set A Problems Set B 1. Describe the advantages and illustrate the impact of issuing bonds instead of common shares. 1, 2, 3, 4, 5, 6 1 1 2. Prepare the entries for the issue of bonds and the recording of interest expense. 7, 8, 9, 10, 11, 12 2, 3, 4, 5, 6, 7 2, 3, 4, 7, 8 1, 2, 3, 5, 6 1, 2, 3, 5, 6 3. Contrast the effects of the straight-line and effective interest methods of amortizing bond discounts and premiums. 13, 14 7, 8 5, 6 4, 5 4, 5 4. Prepare the entries when bonds are retired. 15 9 7, 8, 9 6 6 5. Account for long-term notes payable. 16, 17 10, 11 10 7 7 6. Contrast the accounting for operating leases and capital leases. 18, 19 12 11, 12 8 8 7. Explain and illustrate the methods for the financial statement presentation and analysis of long-term liabilities. 20, 21, 22 13, 14 12, 13 1, 2, 5, 7, 9 1, 2, 5, 7, 9 16-1 ASSIGNMENT CHARACTERISTICS TABLE Problem Number Description Difficulty Level Time Allotted (min.) 1A Prepare entries for bonds, using straight-line method of amortization. Show balance sheet presentation. Simple 25-35 2A Prepare entries for bonds, using straight-line method of amortization. Show balance sheet presentation. Simple 25-35 3A Prepare entries for bonds using effective interest method of amortization. Moderate 20-30 4A Prepare entries for bonds sold between interest periods. Simple 10-20 5A Prepare entries for bonds, using effective interest method of amortization. Show balance sheet presentation. Answer analytical questions. Moderate 25-35 6A Prepare entries for bonds, using straight-line method of amortization, and redemption of bonds. Moderate 25-35 7A Prepare instalment payments schedule and entries for mortgage note payable. Show balance sheet presentation. Moderate 20-30 8A Analyse various lease situations, prepare entries, and discuss financial statement presentation. Moderate 20-30 9A Calculate and analyse debt ratios. Moderate 20-30 1B Prepare entries for bonds, using straight-line method of amortization. Show balance sheet presentation. Simple 25-35 2B Prepare entries for bonds, using straight-line method of amortization. Show balance sheet presentation. Simple 25-35 3B Prepare entries for bonds, using effective interest method of amortization. Moderate 20-30 4B Prepare entries for bonds sold between interest periods, using straight-line method of amortization. Complex 25-35 5B Prepare entries for bonds, using effective interest method of amortization. Show balance sheet presentation. Answer analytical questions. Moderate 25-35 6B Calculate interest rate on bonds; prepare entries for bonds, using straight-line method of amortization, and redemption of bonds. Complex 25-35 7B Prepare instalment payments schedule and entries for mortgage note payable. Show balance sheet presentation. Moderate 20-30 8B Analyse various lease situations, prepare entries and discuss financial statement presentation. Moderate 20-30 16-2 Problem Number 9B Description Difficulty Level Time Allotted (min.) Calculate and analyse debt ratios. Moderate 20-30 16-3 BLOOM’S TAXONOMY TABLE Correlation Chart between Bloom’s Taxonomy, Study Objectives and End-of-Chapter Material Study Objectives 1. Describe the advantages and illustrate the impact of issuing bonds instead of common shares. Knowledge Comprehension Q16-1 Q16-2 Q16-3 Q16-4 Q16-5 Q16-6 Application BE16-1 Analysis E16-1 2. Prepare the entries for the issue of bonds and recording of interest expense. Q16-10 Q16-7 Q16-8 Q16-9 Q16-11 Q16-12 BE16-2 BE16-3 BE16-4 BE16-5 BE16-6 BE16-7 E16-2 E16-3 E16-4 E16-7 E16-8 P16-1A P16-2A P16-3A P16-6A P16-1B P16-2B P16-3B P16-6B P16-5A P16-5B 3. Contrast the effects of the straight-line and effective interest methods of amortizing bond discounts and premiums. Q16-14 Q16-13 BE16-7 BE16-8 E16-5 P16-4A P16-4B E16-6 P16-5A P16-5B 4. Prepare the entries when bonds are retired. Q16-15 BE16-9 E16-7 E16-8 E16-9 P16-6A P16-6B 5. Account for long-term notes payable. Q16-16 Q16-17 BE16-10 BE16-11 E16-10 P16-7A P16-7B 6. Contrast the accounting for operating leases and capital leases. Q16-18 Q16-19 BE16-12 E16-11 P16-8A P16-8B E16-12 7. Explain and illustrate the methods for the financial statement presentation and analysis of long-term liabilities. Q16-21 Q16-22 BE16-13 BE16-14 E16-13 P16-1A P16-2A P16-7A P16-1B P16-2B P16-7B E16-12 P16-5A P16-9A P16-5B P16-9B BYP16-4 BYP16-1 BYP16-2 BYP16-5 Broadening Your Perspective Q16-20 16-4 BYP16-3 BYP16-6 BYP16-7 Synthesis Evaluation BYP16-8 ANSWERS TO QUESTIONS 01. Long-term liabilities are obligations that are expected to be paid after one year. Examples include bonds, long-term notes payable, and lease liabilities. 02. (a) The major advantages are: 1. Shareholder control is not affected—bondholders do not have voting rights, with the result that current shareholders retain full control over the company. 2. Income tax savings result—bond interest is deductible for tax purposes; dividends on shares are not. 3. Income to common shareholders may increase—if a company can earn more on borrowed funds than the interest cost on these funds, the income to common shareholders will increase. 4. Earnings per share may be higher—although bond interest expense will reduce net income, earnings per share will often be higher under bond financing, because no additional common shares are issued. (b) The major disadvantages in using bonds are that interest must be paid on a periodic basis and the principal (face value) of the bonds must be paid at maturity. They are binding legal obligations. 03. (a) Secured bonds have specific assets of the issuer pledged as collateral. In contrast, unsecured bonds are issued against the general credit of the borrower. These bonds are called debenture bonds. (b) Term bonds mature at a single specified future date. In contrast, serial bonds mature in instalments. (c) Retractable bonds can be redeemed before maturity at the option of the bondholder. In contrast, redeemable bonds are subject to call and retirement at a stated dollar amount prior to maturity, at the option of the issuer. 16-5 Questions Chapter 16 (Continued) 04. (a) Face value is the amount of principal due at the maturity date. Face value is also called par value. (b) The contractual interest rate is the rate used to determine the amount of cash interest the borrower pays and the investor receives. This rate is also called the stated interest rate, because it is the rate stated on the bonds. (c) The market rate of interest is the rate investors demand for lending their money. 05. The two major obligations incurred by a company when bonds are issued are the interest payments due on a periodic basis and the principal that must be paid at maturity. 6. Convertible bonds are bonds that can be converted into shares. The advantage to a bondholder is that they have the opportunity to convert their bonds if the market price of the shares increases. While waiting for the share price to increase, the bondholders still receive interest payments. For the issuer, bonds with a conversion feature generally sell at a higher price and pay a lower rate of interest than comparable debt securities that do not have a conversion option. 07. Investors paid less than the face value; therefore, the market interest rate must have been greater than the contractual rate. 08. $30,000. $600,000 X 10% X 6/12 months = $30,000. Because there is no premium or discount the interest expense will be the same regardless of whether the effective interest method or the straight-line method of amortization is used. 09. $860,000. The balance of the Bonds Payable account minus the balance of the Discount on Bonds Payable account (or plus the balance of the Premium on Bonds Payable account) equals the carrying value of the bonds. 16-6 Questions Chapter 16 (Continued) 10. The straight-line method results in the same amortized amount being allocated to Interest Expense each interest period. This amount is determined by dividing the total bond discount or premium by the number of interest periods the bonds will be outstanding. The effective interest method results in varying amounts of amortization and interest expense per period but a constant percentage rate. The amount is determined by multiplying the carrying value of the bonds at the beginning of the period by the market (effective) rate of interest. 11. $14,400. Interest expense is the interest to be paid in cash less the premium amortization for the year. Cash to be paid equals 8% X $200,000 or $16,000. Total premium equals 4% of $200,000 or $8,000. Since this is to be amortized over 5 years (the life of the bonds) in equal amounts, the amortization amount is $8,000 5 = $1,600. Thus, $16,000 – $1,600 or $14,400 equals interest expense for 2003. Since the straight line method is being used interest expense for 2004 will also be $14,400. 12. Decrease. Under the effective-interest method the interest charge per period is determined by multiplying the carrying value of the bonds by the effective-interest rate. When bonds are issued at a premium, the carrying value decreases over the life of the bonds. As a result, the interest expense will also decrease over the life of the bonds, because it is determined by multiplying the decreasing carrying value of the bonds by the effective-interest rate. 13. The investor will pay 4 months accrued interest, $27 ($1,000 X 8% X 4/12). The bond discount will be amortized over 56 months (60 – 4). 14. Julia should tell her staff that the effective-interest method results in a varying amount of interest expense but a constant rate of interest on the balance outstanding. Accordingly, it results in a better matching of expenses with revenues than the straight-line method. 16-7 Questions Chapter 16 (Continued) 15. Bond Payable ..................................................................... XXX Premium on Bonds ............................................................ XXX Gain on Redemption ................................................ Cash .......................................................................... XXX XXX 16. Instalment notes payable with fixed principal payments are repayable in equal periodic amounts, plus interest. Instalment notes with blended principal and interest payments are repayable in equal periodic amounts, including interest. 17. This is not the case. Each payment by Doug consists of (1) interest on the unpaid balance of the loan and (2) a reduction of loan principal. The interest decreases each period (as the principal owing is reduced) while the portion applied to the loan principal increases each period. 18. (a) A lease agreement is a contract in which the lessor gives the lessee the right to use an asset for a specified period, in return for one or more periodic rental payments. The lessor is the owner of the property and the lessee is the renter or tenant. (b) The two major types of leases are operating leases and capital leases. (c) In an operating lease the property is rented by the lessee and the lessor retains all ownership risks and responsibilities. A capital lease transfers substantially all the benefits and risks of ownership from the lessor to the lessee, so that the lease is in effect a purchase of the property. 19. In a capital lease agreement, the lessee records the present value of the lease payments as an asset and a liability. Therefore, Rasch Company would debit Leased Equipment for $186,300 and credit Lease Liability for the same amount. 16-8 Questions Chapter 16 (Continued) 20. The nature and the amount of each long-term liability should be presented in the balance sheet or in schedules in the accompanying notes to the financial statements. The notes should also indicate the interest rates, maturity dates, conversion privileges, any assets pledged as collateral, and the currency (e.g., Cdn. dollars, US dollars, Euros, etc.) in which the liabilities are denominated. 21. EBIT stands for earnings before interest expense and income tax expense. EBITDA stands for interest before interest expense, income tax expense, and depreciation and amortization expense. EBITDA is a basic measure of a company’s ability to generate cash from operating activities. 22. The accrual-based interest coverage ratio does not necessarily indicate whether the company has sufficient cash available to pay interest. Therefore, investors often consider the cash based interest coverage ratio to be a better indication of an entity’s ability to meet debt service requirements. 16-9 SOLUTIONS TO BRIEF EXERCISES BRIEF EXERCISE 16-1 Issue Shares Issue Bonds Income before interest and income tax Interest expense ($2,000,000 X 8%) Income before income tax Income tax expense (30%) Net income (a) $1,000,000 00, 00,000 01,000,000 0 ,300,000 $ 700,000 $1,000,000 00,160,000 00,840,000 0 ,252,000 $ 588,000 Issued shares (b) Earnings per share (a) (b) 00,700,000 00$1.00 00,500,000 00$1.18 Net income is higher if shares are issued. However, earnings per share is lower because of the additional shares that are issued. Therefore, on the basis of earnings per share, the bonds alternative is preferable. BRIEF EXERCISE 16-2 (a) Mar. 01 Cash ....................................................... Bonds Payable (1,000 X $1,000) ... 1,000,000 (b) Sept. 01 Bond Interest Expense ......................... Cash ($1,000,000 X 9% X 6/12) ...... 45,000 (c) Dec. 31 Bond Interest Expense ......................... Bond Interest Payable ($1,000,000 X 9% X 4/12) ............ 30,000 16-10 1,000,000 45,000 30,000 BRIEF EXERCISE 16-3 (a) (a) Mar. 01 Cash (98% X $1,000,000) ...................... Discount on Bonds Payable ................. Bonds Payable ............................... 980,000 20,000 (b) Sept. 01 Bond Interest Expense ......................... Discount on Bonds Payable ($20,000 5 X 6/12) .................... Cash ($1,000,000 X 9% X 6/12) ...... 47,000 (c) Dec. 31 Bond Interest Expense ......................... Discount on Bonds Payable ($20,000 5 X 4/12) ..................... Bond Interest Payable ($1,000,000 X 9% X 4/12) ............ 31,333 1,000,000 2,000 45,000 1,333 30,000 (b) (a) Mar. 1 Cash (102% X $1,000,000) .................... Bonds Payable ............................... Premium on Bonds Payable ......... 1,020,000 Interest Expense ................................... Premium on Bonds Payable ($20,000 5 X 6/12) ........................... Cash ($1,000,000 X 9% X 6/12) ...... 43,000 (c) Dec. 31 Bond Interest Expense ......................... Premium on Bonds Payable ($20,000 5 X 4/12) ........................... Bond Interest Payable ($1,000,000 X 9% X 4/12) ........... 28,667 (b) Sept. 1 16-11 1,000,000 20,000 2,000 45,000 1,333 30,000 BRIEF EXERCISE 16-4 (a) Jan. 01 Cash (96% X $2,000,000) ...................... Discount on Bonds Payable ................. Bonds Payable ............................... 1,920,000 80,000 (b) July 01 Bond Interest Expense ......................... Discount on Bonds Payable ($80,000 10 X 6/12) .................. Cash ($2,000,000 X 9% X 6/12) ...... 94,000 2,000,000 4,000 90,000 BRIEF EXERCISE 16-5 (a) Jan. 1 Cash (103% X $3,000,000) .................... Bonds Payable ............................... Premium on Bonds Payable ......... 3,090,000 (b) July 1 Interest Expense .................................... Premium on Bonds Payable ($90,000 5 X 6/12) ............................. Cash ($3,000,000 X 10% X 6/12) .... 141,000 16-12 3,000,000 90,000 9,000 150,000 BRIEF EXERCISE 16-6 Discount = $100,000 – $92,639 = $7,361 (a) Straight-Line Amortization Date October 1, 2003 1. Bond Interest Payable $100,000 X 10% X 6/12 = $5,000 April 1, 2004 $100,000 X 10% X 6/12 = $5,000 2. Amortization of Discount $7,361 ÷ 5 x 6/12 = $736.10 $7,361 ÷ 5 X 6/12 = $736.10 3. Interest Expense (1 + 2) $5,736.10 (b) $5,736.10 Effective Interest Amortization Date October 1, 2003 April 1, 2004 1. Bond Interest Payable $100,000 X 10% X 6/12 = $5,000 $100,000 X 10% X 6/12 = $5,000 2. Interest Expense $92,639 X 12% X 6/12 = $5,559 $92,639 + $559 = $93,198 X 12% X 6/12 = $5,592 3. Amortization of Discount $5,000 - $5,559 (1-2) = $559 16-13 $5,000 - $5,592 = $592 BRIEF EXERCISE 16-7 (a) Bond Interest Expense ................................................... Discount on Bonds Payable ................................... Cash ......................................................................... 46,884 1,884 45,000 (b) Contractual interest rate: ($45,000 X 2) ÷ ($62,311 + $937,689) = 9% Market interest rate: ($46,884 X 2) ÷ $937,689 = 10% (c) Interest expense is greater than interest paid because the bonds sold at a discount. The bonds sold at a discount because investors demand a market (or effective) interest rate higher than the contractual interest rate. (d) Interest expense increases each period because the bond carrying value increases each period. As the market interest rate is applied to this bond carrying amount, interest expense will increase. (e) The advantage of the effective rate method is that it uses a constant rate of interest. The effective-interest method results in a varying amount of interest expense but a constant rate of interest on the balance outstanding. Accordingly, it results in a better matching of expenses with revenues than the straight-line method. BRIEF EXERCISE 16-8 (a) May 01 Cash ....................................................... Bonds Payable ............................... Bond Interest Payable ($1,000,000 X 9% X 4/12) ........... 1,030,000 (b) July 01 Bond Interest Payable .......................... Bond Interest Expense ($1,000,000 X 9% X 2/12) ................... Cash ($1,000,000 X 9% X 6/12) ...... 30,000 16-14 1,000,000 30,000 15,000 45,000 BRIEF EXERCISE 16-9 July 1 Bonds Payable ....................................... Loss on Bond Redemption ($990,000 – $940,000) ........................ Discount on Bonds Payable ......... Cash ($1,000,000 X 99%) ............... 1,000,000 50,000 60,000 990,000 BRIEF EXERCISE 16-10 (a) Monthly Interest Period Nov. 30, 2003 Dec. 31, 2003 Jan. 31, 2004 2003 Nov. 30 Dec. 31 2004 Jan. 31 (A) Cash Payment $5,000 04,979 (B) Interest Expense (D) X 10% X 1/12 (C) Reduction of Principal (A) – (B) $2,500 02,479 $2,500 02,500 Cash ............................................................. Mortgage Note Payable ....................... 300,000 Interest Expense ......................................... Mortgage Note Payable .............................. Cash ..................................................... 2,500 2,500 Interest Expense ......................................... Mortgage Note Payable .............................. Cash ..................................................... 2,479 2,500 16-15 (D) Principal Balance (D) – (C) $300,000 297,500 295,000 2,000 300,000 5,000 4,979 BRIEF EXERCISE 16-10 (Continued) (b) Monthly Interest Period Nov. 30, 2003 Dec. 31, 2003 Jan. 31, 2004 2003 Nov. 30 Dec. 31 2004 Jan. 31 (A) Cash Payment $3,964.52 3,964.52 (B) Interest Expense (D) X 10% X 1/12 $2,500.00 2,487.79 (C) Reduction of Principal (A) – (B) (D) Principal Balance (D) – (C) $1,464.52 1,476.73 01476.73 $300,000.00 298,535.48 297,058.75 22,000 Cash ............................................................. 300,000.00 Mortgage Note Payable ....................... 300,000.00 Interest Expense ......................................... Mortgage Note Payable .............................. Cash ..................................................... 2,500.00 1,464.52 Interest Expense ......................................... Mortgage Note Payable .............................. Cash ..................................................... 2,487.79 1,476.73 3,964.52 3,964.52 BRIEF EXERCISE 16-11 Monthly Interest Period Issue Date 1 2 3 (A) Cash Payment $132.15 0132.15 132.15 (B) Interest Expense (D) X 10% X 1/12 $83.33 082.93 82.52 16-16 (C) Reduction of Principal (A) – (B) (D) Principal Balance (D) – (C) $48.82 49.22 49.63 01476.73 $10,000.00 9,951.18 9,901.96 9,852.33 22,000 BRIEF EXERCISE 16-12 1. 2. Rent Expense ........................................................ Cash ............................................................... 70,000 Leased Asset—Building ....................................... Lease Liability ............................................... 600,000 70,000 600,000 BRIEF EXERCISE 16-13 WAUGH COMPANY Balance Sheet (Partial) December 31, 2003 Long-term liabilities Bonds payable, due 2005 .................................... $900,000 Less: Discount on bonds payable ..................... 45,000 Notes payable, due 2007 ......................................................... Lease liability ........................................................................... Total long-term liabilities ................................................. $855,000 80,000 0 50,000 $985,000 Note that any portion to be paid within the next year should be reported separately, under current liabilities. 16-17 BRIEF EXERCISE 16-14 ($ in millions) (a) Debt to total assets = Total debt ÷ Total assets $2,086.1 67.04% $3,111.8 (b) Interest coverage= EBIT ÷ Interest expense ($70.8) ($4.9) $77.8 0.03 times $77.8 (c) Cash interest coverage = EBITDA ÷ Interest expense ($70.8) ($4.9) $77.8 $100.3 1.32 times $77.8 16-18 SOLUTIONS TO EXERCISES EXERCISE 16-1 Issue Shares Issue Bonds Income before interest and income tax Interest expense ($2,700,000 X 13%) Income before income tax Income tax expense (30%) Net income Issued shares Earnings per share $500,000 0 0500,000 0150,000 $350,000 0150,000 0$2.33 $500,000 0351,000 0149,000 0 44,700 $104,300 0090,000 0$1.16 Net income and earnings per share would be higher if the company financed the fleet using a share issue versus debt. EXERCISE 16-2 (a) Jan. 01 Cash ........................................................... Bonds Payable ................................... 100,000 (b) July 01 Bond Interest Expense ............................. Cash ($100,000 X 10% X 6/12)........... 5,000 (c) Dec. 31 Bond Interest Expense ............................. Bond Interest Payable ....................... 5,000 16-19 100,000 5,000 5,000 EXERCISE 16-3 (a) Jan. 01 Cash ........................................................... Discount on Bonds Payable ..................... Bonds Payable ................................... (b) July 01 Bond Interest Expense ($609,497 X 10% X 6/12) ......................... Discount on Bonds Payable ............. Cash ($650,000 X 9% X 6/12)............. (c) Dec. 31 Bond Interest Expense [($609,497 + $1,225) X 10% X 6/12] ....... Discount on Bonds Payable ............. Bond Interest Payable ....................... 609,497 40,503 650,000 30,475 1,225 29,250 30,536 1,286 29,250 Detailed Calculations: Semiannual Interest Period Issue date 1 2 (B) (A) Interest Expense Interest (Preceding (C) (D) Payment Bond Carrying Discount Unamortized ($650,000 X Value X 10% X Amortization Discount 9% X 6/12) 6/12) (B) – (A) (D) – (C) 29,250 29,250 30,475 30,536 1,225 1,286 16-20 40,503 39,278 37,992 (E) Bond Carrying Value 609,497 610,722 612,008 16-21 EXERCISE 16-4 (a) Jan. 01 Cash ........................................................... Premium on Bonds Payable ............. Bonds Payable ................................... 637,378 37,378 600,000 (b) July 01 Bond Interest Expense ($637,378 X 10% X 6/12) .......................... Premium on Bonds Payable ..................... Cash ($600,000 X 11% X 6/12)........... 31,869 1,131 (c) Dec. 31 Bond Interest Expense [($637,378 – $1,131) X 10% X 6/12] ...... Premium on Bonds Payable ..................... Bond Interest Payable ....................... 31,812 1,188 33,000 33,000 Detailed Calculations: (A) Interest Semi - Payment annual ($600,000 Interest X 11% X Period 6/12) Issue date 1 2 33,000 33,000 (B) Interest Expense (Preceding (C) Bond Carrying Premium Value X 10% X Amortization 6/12) (A) – (B) 31,869 31,812 1,131 1,188 16-22 (D) Unamortized Premium (D) – (C) 37,378 36,247 35,059 (E) Bond Carrying Value 637,378 636,247 635,059 EXERCISE 16-5 (a) Apr. 01 Cash ........................................................... Bonds Payable ................................... Bond Interest Payable ($120,000 X 10% X 3/12) ................ 123,000 (b) July 01 Bond Interest Payable .............................. Bond Interest Expense ............................. Cash ($120,000 X 10% X 6/12)........... 3,000 3,000 (c) Apr. 01 Cash ........................................................... Bonds Payable ................................... Premium on Bonds............................ Bond Interest Payable ($120,000 X 10% X 3/12) ................ 124,200 July 01 Bond Interest Payable .............................. Bond Interest Expense ............................. Premium on Bonds ($1,200 ÷ 10 X 6/12) .. Cash ($120,000 X 10% X 6/12)........... 3,000 2,940 60 16-23 120,000 3,000 6,000 120,000 1,200 3,000 6,000 EXERCISE 16-6 (a) Jan. 1 Cash ........................................................ Discount on Bonds Payable .................. Bonds Payable ............................... 864,100 135,900 1,000,000 (b) (1) Straight-Line Method Period 1 Period 20 Bond Interest Expense .......................... Discount on Bonds Payable ($135,900 ÷ 20) ............................. Cash ($1,000,000 X 6% X 6/12)....... 36,795 Bond Interest Expense .......................... Discount on Bonds Payable ($135,900 ÷ 20) ............................. Cash ($1,000,000 X 6% X 6/12)....... 36,795 6,795 30,000 6,795 30,000 (2) Effective Interest Method Period 1 Period 20 1 Bond Interest Expense ($864,100 X 8% X 6/12) ........................ Discount on Bonds Payable .......... Cash ($1,000,000 X 6% X 6/12)....... Bond Interest Expense .......................... Discount on Bonds Payable .......... Cash ($1,000,000 X 6% X 6/12)....... 34,564 4,564 30,000 39,6151 Principal: $1,000,000 X 0.96154 (Table 3, n=1, i=4%) = $961,540 Interest: $30,000 x 0.96154 (Table 4, n=1, i=4%) = $28,846 Carrying (present) value of bond at end of period 19 = $961,540 + $28,846 = $990,386 x 8% x 6/12 = $39,615 16-24 9,615 30,000 EXERCISE 16-6 (Continued) (c) (1) Straight-Line Method Period 1 $36,795 ÷ $864,100 = 4.3% Period 20 $36,795 ÷ $990,386 = 3.7% (2) Effective Interest Method Period 1 $34,564 ÷ $864,100 = 4.0% Period 20 $39,615 ÷ $990,386 = 4.0% (d) The effective rate of interest method provides the better measure of the effective cost of borrowing. Using this method interest expense as a percentage of the carrying value remains constant over the life of the bond. EXERCISE 16-7 2003 (a) Jan. 01 Cash ($400,000 X 103%) ........................... Premium on Bonds Payable ............. Bonds Payable ................................... (b) July 01 Bond Interest Expense ............................. Premium on Bonds Payable ($12,000 ÷ 20 X 6/12) ................................. Cash ($400,000 X 9% X 6/12)............. 2022 (c) Dec. 31 Bond Interest Expense ............................. Premium on Bonds Payable ..................... Bond Interest Payable ....................... 2023 (d) Jan. 1 Bonds Payable ........................................... Cash ................................................... 16-25 412,000 12,000 400,000 17,700 300 18,000 17,700 300 18,000 400,000 400,000 EXERCISE 16-8 (a) 2003 Dec. 31 Cash ........................................................... Discount on Bonds Payable ..................... Bonds Payable ................................... (b) 2004 June 30 Bond Interest Expense ............................. Discount on Bonds Payable ($20,000 10 X 6/12) ...................... Cash ($300,000 X 11% X 6/12)........... (c) 2004 Dec. 31 Bond Interest Expense ............................. Discount on Bonds Payable ............. Cash ................................................... (d) 2013 Dec. 31 Bonds Payable .......................................... Cash ................................................... 280,000 20,000 300,000 17,500 1,000 16,500 17,500 1,000 16,500 300,000 300,000 EXERCISE 16-9 1. 2. June 30 Bonds Payable .......................................... Loss on Bond Redemption ($121,200 – $107,500) ............................ Discount on Bonds Payable ($120,000 – $107,500) .................... Cash ($120,000 X 101%) .................... 120,000 June 30 Bonds Payable .......................................... Premium on Bonds Payable ..................... Gain on Bond Redemption ............... Cash ($150,000 X 96%) ...................... 150,000 1,000 16-26 13,700 12,500 121,200 7,000 144,000 EXERCISE 16-10 (a) Semi-annual Interest Period Dec. 31, 2003 June 30, 2004 Dec. 31, 2004 (A) Cash Payment $15,000 14,625 01 (B) Interest Expense (D) X 10% X 6/12 $7,500 07,125 (C) Reduction of Principal (A) – (B) (D) Principal Balance (D) – (C) $7,500 7,500 01476.73 $150,000 142,500 135,000 22,000 Issue of Note 2003 Dec. 31 Cash .................................................... Mortgage Note Payable .............. 150,000 150,000 First Instalment Payment 2004 June 30 Interest Expense ($150,000 X 10% X 6/12) ................. Mortgage Note Payable...................... Cash ............................................ 7,500 7,500 15,000 Second Instalment Payment Dec. 31 Interest Expense [($150,000 – $7,500) X 10% X 6/12] Mortgage Note Payable...................... Cash............................................. 16-27 7,125 7,500 14,625 EXERCISE 16-10 (Continued) (b) Semi-annual Interest Period Issue Date June 30, 2004 Dec. 31, 2004 (A) Cash Payment $12,036.39 12,036.39 01 (B) Interest Expense (D) X 10% X 6/12 $7,500.00 7,273.18 (C) Reduction of Principal (A) – (B) (D) Principal Balance (D) – (C) $4,536.39 4,763.21 01476.73 $150,000.00 145,463.61 140,700.40 22,000 0 Issue of Note 2003 Dec. 31 Cash .................................................... Mortgage Note Payable .............. 150,000 150,000 First Instalment Payment 2004 June 30 Interest Expense ($150,000 X 10% X 6/12) ................. 7,500.00 Mortgage Note Payable...................... 4,536.39 Cash ............................................ 12,036.39 Second Instalment Payment Dec. 31 Interest Expense [($150,000 – $4,536.39) X 10% X 6/12] .............. 7,273.18 Mortgage Note Payable...................... 4,763.21 Cash............................................. 16-28 12,036.39 EXERCISE 16-11 (a) May 21 Car Rental Expense ................................. Cash .................................................. 500 (b) Jan. 01 Leased Equipment ................................... Lease Liability................................... 149,211 500 149,211 EXERCISE 16-12 (a) ($ in millions) 1. Debt to total assets = Total debt ÷ Total assets $2,199.9 62.0% $3,546.2 2. Interest coverage = EBIT ÷ Interest expense $199.6 $145.0 $72.3 5.8 times $72.3 3. Cash interest coverage = EBITDA ÷ Interest expense $199.6 $145.0 $72.3 $113.5 7.3 times $72.3 (b) The implication of these unrecorded liabilities is that it reduces the cash available to meet debt-servicing requirements. 16-29 EXERCISE 16-13 (a) PRIYA CORPORATION Balance Sheet (Partial) July 31, 2004 Long-term liabilities Bonds payable, due 2010 .......................... $150,000 Add: Premium on bonds payable ............ 0 32,000 Lease liability..................................................... Total long-term liabilities .......................... $182,000 48,500 $230,500 (b) Bond Interest Payable should be classified as a current liability. Similarly, the portion of the lease liability due within one year should be classified as a current liability 16-30 SOLUTIONS TO PROBLEMS PROBLEM 16-1A (a) 1. 2. 3. Jan. 01 Cash ($2,500,000 X 100%) ....................... 2,500,000 Bonds Payable .................................. July 01 Bond Interest Expense ............................ Cash ($2,500,000 X 8% X 6/12) ......... 100,000 Dec. 31 Bond Interest Expense ............................ Bond Interest Payable ...................... 100,000 100,000 100,000 Jan. 01 Cash ($2,500,000 X 103%) ....................... 2,575,000 Premium on Bonds Payable ............ Bonds Payable .................................. July 01 Bond Interest Expense ............................ Premium on Bonds Payable ($75,000 10 X 6/12) ............................ Cash ($2,500,000 X 8% X 6/12) ......... 96,250 Dec. 31 Bond Interest Expense ............................ Premium on Bonds Payable .................... Bond Interest Payable ...................... 96,250 3,750 75,000 2,500,000 3,750 100,000 100,000 Jan. 01 Cash ($2,500,000 X 96%) ......................... 2,400,000 Discount on Bonds Payable .................... 100,000 Bonds Payable .................................. July 01 Bond Interest Expense ............................ Discount on Bonds Payable ($100,000 10 X 6/12) .................... Cash .................................................. 105,000 Dec. 31 Bond Interest Expense ............................ Discount on Bonds Payable ............ Bond Interest Payable ...................... 105,000 16-31 2,500,000 2,500,000 5,000 100,000 5,000 100,000 PROBLEM 16-1A (Continued) (b) Par ECOMDRIVE.COM CORPORATION Balance Sheet (Partial) December 31, 2003 Current liabilities Bond interest payable .................................................... Long-term liabilities Bonds payable, due 2013 .............................................. 00, $ 100,000 2,500,000 Premium ECOMDRIVE.COM CORPORATION Balance Sheet (Partial) December 31, 2003 Current liabilities Bond interest payable .................................................... Long-term liabilities Bonds payable, due 2013 ....................... Add: Premium on bonds payable.......... $2,500,000 67,500 $0,0100,000 2,567,500 Discount ECOMDRIVE.COM CORPORATION Balance Sheet (Partial) December 31, 2003 Current liabilities Bond interest payable .................................................... Long-term liabilities Bonds payable, due 2013 ....................... Less: Discount on bonds payable ........ 16-32 $2,500,000 0 ,090,000 $0,0100,000 2,410,000 PROBLEM 16-2A (a) 2003 Jan. 01 Cash (104% X $4,000,000) .................... Bonds Payable ............................... Premium on Bonds Payable ......... 4,160,000 4,000,000 160,000 (b) See following page. (c) 2003 July 01 Bond Interest Expense ......................... Premium on Bonds Payable ................. Cash ............................................... Dec. 31 Bond Interest Expense ......................... Premium on Bonds Payable ................. Bond Interest Payable ................... 2004 Jan. 01 Bond Interest Payable .......................... Cash ............................................... 192,000 8,000 200,000 192,000 8,000 200,000 200,000 200,000 July 01 Bond Interest Expense ......................... Premium on Bonds Payable ................. Cash ............................................... 192,000 8,000 Dec. 31 Bond Interest Expense ......................... Premium on Bonds Payable ................. Bond Interest Payable ................... 192,000 8,000 16-33 200,000 200,000 PROBLEM 16-2A (Continued) (b) Semiannual Interest Period Jan. 1, 2003 July 1, 2003 Jan. 1, 2004 July 1, 2004 Jan. 1, 2005 (A) Interest Payment ($4,000,000 X 10% X 6/12) $200,000 0200,000 0200,000 0200,000 (B) Interest Expense (A) – (C) (C) (E) Premium (D) Bond Amortization Unamortized Carrying Value ($160,000 10 Premium [$3,000,000 + X 6/12) (D) – (C) (D)] $192,000 0192,000 0192,000 0192,000 $160,000 0152,000 0144,000 0136,000 0128,000 $8,000 08,000 08,000 08,000 (d) EASTER ELECTRIC Balance Sheet (Partial) December 31, 2004 Current liabilities Bond interest payable ...................................................... Long-term liabilities Bonds payable, due 2013........................... $4,000,000 Add: Premium on bonds payable ............. 0 128,000 16-34 $200,000 4,128,000 $4,160,000 04,152,000 04,144,000 04,136,000 04,128,000 PROBLEM 16-3A (a) (b) 2003 July 01 Cash ....................................................... Discount on Bonds Payable ................. Bonds Payable ............................... 2,531,760 168,240 2,700,000 GLOBAL SATELLITES Bond Discount Amortization Effective Interest Method—Semi-annual Interest Payments 9% Bonds Issued at 10% Semiannual Interest Period (A) (B) Interest Interest Payment Expense July 1, 2003 Jan. 1, 2004 $121,500 $126,588 July 1, 2004 0121,500 0126,842 Jan. 1, 2005 0121,500 0127,110 (C) Discount Amortization (B) – (A) $5,088 05,342 05,610 (D) (E) UnamorBond tized Carrying Discount Value (D) – (C) ($2,700,000 – D) $168,240 0163,152 0157,810 0152,200 (c) 2003 Dec. 31 Bond Interest Expense ($2,531,760 X 10% X 6/12) .................. Discount on Bonds Payable ......... Bond Interest Payable ($2,700,000 X 9% X 6/12) ............ (d) 2004 July 01 Bond Interest Expense [($2,531,760 + $5,088) X 10% X 6/12] Discount on Bonds Payable ......... Cash ............................................... 16-35 $2,531,760 02,536,848 02,542,190 02,547,800 126,588 5,088 121,500 126,842 5,342 121,500 PROBLEM 16-3A (Continued) (e) Dec. 31 Bond Interest Expense [($2,536,848 + $5,342) X 10% X 6/12] Discount on Bonds Payable ......... Bond Interest Payable ................... 16-36 127,110 5,610 121,500 PROBLEM 16-4A (a) Dec. 01 Cash ($1,000,000 X 100%) ....................... 1,020,000 Bonds Payable .................................. Bond Interest Payable ($1,000,000 X 12% X 2/12) ............ (b) Dec. 31 Bond Interest Expense ............................ Bond Interest Payable ($1,000,000 X 12% X 1/12) ............ 10,000 (c) Mar. 31 30,000 30,000 Bond Interest Expense ............................ Bond Interest Payable ............................. Cash ($1,000,000 X 12% X 6/12) ....... 16-37 1,000,000 20,000 10,000 60,000 PROBLEM 16-5A (a) 1. 2. 3. 4. 2003 July 01 Dec. 31 2004 July 01 Dec.31 Cash ............................................... Bonds Payable ....................... Premium on Bonds Payable . 5,623,112 5,000,000 623,112 Bond Interest Expense ($5,623,112 X 10% X 6/12) .......... Premium on Bonds Payable ......... Bond Interest Payable ($5,000,000 X 6% X 6/12) .... 281,156 18,844 300,000 Bond Interest Expense [($5,623,112 – $18,844) X 5%] .... Premium on Bonds Payable ......... Cash........................................ 280,213 19,787 Bond Interest Expense [($5,604,268 – $19,787) X 5%] .... Premium on Bonds Payable ......... Bond Interest Payable ........... 279,224 20,776 300,000 300,000 (b) WEBHANCER CORP. Balance Sheet (Partial) December 31, 2004 Long-term liabilities Bonds payable........................................... Add: Premium on bonds payable............ $5,000,000 0 ,563,705* * $623,112 – $18,844 – $19,787 – $20,776 = $563,705 16-38 $5,563,705 PROBLEM 16-5A (Continued) (c) Dear Webhancer Corp. The effective-interest method will result in more interest expense reported than the straight-line method in 2004 when the bonds are sold at a premium. Straight-line interest expense for 2004 is $537,688 ($300,000 – $31,156 = $268,844 x 2), compared to $559,437 ($280,213 + $279,224) under the effective-interest method. The cost of borrowing over the life of the bonds is equal to the cash payments made less the bond premium received when the bonds were originally sold. Semi-annual interest payments ($5,000,000 X 12% X 10 periods)......................... Less: Bond premium ............................................ Total cost of borrowing .......................................... $6,000,000 00,623,112 $5,376,888 Interest expense will be exactly the same regardless of the method of amortization used. The choice of amortization methods will determine the amount of the premium to be amortized each period. While the different methods will cause the amortization to be different in each period, the overall amount of amortization will be the same—it will always equal the amount of the premium. 16-39 PROBLEM 16-6A (a) Jan. 01 Bond Interest Payable ............................ Cash ................................................. 120,000 (b) July 01 Bond Interest Expense ........................... Discount on Bonds Payable ($90,000 20 periods) ................. Cash ($2,400,000 X 10% X 6/12) ...... 124,500 (c) July 01 Bonds Payable ........................................ Loss on Bond Redemption..................... Discount on Bonds Payable [($90,000 – $4,500) X ¼] ............... Cash ($600,000 X 102%) .................. 600,000 33,375 (d) Dec. 31 Bond Interest Expense ........................... Discount on Bonds Payable ($64,125* 19 periods) ................ Bond Interest Payable ($1,800,000 X 10% X 6/12) ............ 93,375 * $90,000 – $4,500 – $21,375 = $64,125 16-40 120,000 4,500 120,000 21,375 612,000 3,375 90,000 PROBLEM 16-7A (a) Semi-annual Interest Period Dec. 31, 2003 June 30, 2004 Dec. 31, 2004 June 30, 2005 Dec. 31, 2005 Cash Payment $64,194 064,194 064,194 064,194 Interest Expense $40,000 038,790 037,520 036,186 Reduction of Principal Principal Balance $024,194 0025,404 0026,674 0028,008 $800,000 0775,806 750,402 723,728 0695,720 (b) 2003 Dec. 31 Cash ........................................................... Mortgage Notes Payable ................... 800,000 2004 June 30 Interest Expense ....................................... Mortgage Notes Payable .......................... Cash ................................................... 40,000 24,194 Dec. 31 Interest Expense ....................................... Mortgage Notes Payable .......................... Cash ................................................... 16-41 800,000 64,194 38,790 25,404 64,194 PROBLEM 16-7A (Continued) (c) KINYAE ELECTRONICS Balance Sheet (Partial) December 31, 2004 Current liabilities Current portion of mortgage note payable ..... $ 54,682* Long-term liabilities Mortgage notes payable .................................. 695,720** * $26,674 + $28,008 = $54,682 ** $750,402 (Dec. 31, 2004) – $54,682 = $695,720 or see Dec. 31, 2005 balance 16-42 PROBLEM 16-8A (a) Manitoba Enterprises should record the Potter Co. lease as a capital lease because the lease term is greater than 75% of the estimated economic life of the leased property. Both the Haskins Inc. and Lornegren Associates leases should be reported as operating leases, because none of the conditions is met to require treatment as a capital lease. It should be noted that only one condition need be met to require capitalization. (b) The Potter Co. lease is a capital lease. The entry to record the capital lease on January 1, 2003 is as follows: Leased Asset—Truck ................................................... Lease Liability ....................................................... 50,000 50,000 The Lornegren Associates lease is an operating lease. The entry to record the lease payment in 2003 therefore is as follows: Rent Expense ................................................................ Cash ....................................................................... 13,000 13,000 This entry would be made on the date the rental payment is due. The Haskins Inc. lease is an operating lease. The entry to record the lease payment in 2003 therefore is as follows: Rent Expense ................................................................ Cash ....................................................................... 4,000 This entry would be made on the date the rental payment is due. 16-43 4,000 PROBLEM 16-8A (Continued) (c) Since the Lornegren lease and Haskins lease do not qualify as a capital leases, nothing would appear on Manitoba’s balance sheet regarding either the bulldozer or the furniture. As well, no amount payable under the terms of the lease arrangement will appear on Manitoba’s balance sheet. The annual rental fees would simply be charged to expense when they are paid each year. The Potter Co. lease is a capital lease. Therefore, the truck would be recorded as an asset on Manitoba’s balance sheet. A corresponding liability for leased assets would also be recorded. 16-44 PROBLEM 16-9A (a) ($ in millions) 1. Debt to total assets = Total debt ÷ Total assets 2000 1999 $5,075 ÷ $7,979 = 63.6% $4,510 ÷ $7,105 = 63.4% 2. Interest coverage = EBIT ÷ Interest expense 2000 1999 ($376 + $280 + $112) ÷ $112 = 6.9 times ($261 + $199 + $68) ÷ $68 = 7.8 times 3. Cash interest coverage = EBITDA ÷ Interest expense 2000 1999 (b) ($376 + $280 + $112 + $273) ÷ $112 = 9.3 times ($261 + $199 + $68 + $183) ÷ $68 = 10.5 times Although Loblaw has a significant amount of debt, the company appears to be generating sufficient income and cash to continue to operate without any concerns as to solvency. 16-45 PROBLEM 16-1B (a) 1. 2. 3. July 01 Cash ($500,000 X 100%) .......................... Bonds Payable .................................. 500,000 Dec. 31 Bond Interest Expense ............................ Bond Interest Payable ($500,000 X 12% X 6/12) ................ 30,000 July 1 Cash ($500,000 X 104%) .......................... Premium on Bonds Payable ............ Bonds Payable .................................. 520,000 Dec. 31 Bond Interest Expense ............................ Premium on Bonds Payable ($20,000 ÷ 10 X 6/12) .............................. Bond Interest Payable ($500,000 X 12% X 6/12) ................ 29,000 July 01 Cash ($500,000 X 98%) ............................ Discount on Bonds Payable .................... Bonds Payable .................................. 490,000 10,000 Dec. 31 Bond Interest Expense ............................ Discount on Bonds Payable ($10,000 ÷ 10 X 6/12) ...................... Bond Interest Payable ($500,000 X 12% X 6/12) ................ 30,500 16-46 500,000 30,000 20,000 500,000 1,000 30,000 500,000 500 30,000 PROBLEM 16-1B (Continued) (b) 1. Par EATSLEEPMUSIC.COM INC. Balance Sheet (Partial) December 31, 2003 Current liabilities Bond interest payable .................................................... $ 30,000 Long-term liabilities Bonds payable, due 2013 .............................................. 500,000 2. Premium EATSLEEPMUSIC.COM INC. Balance Sheet (Partial) December 31, 2003 Current liabilities Bond interest payable .................................................... Long-term liabilities Bonds payable, due 2013 ......................... Add: Premium on bonds payable............ $ 30,000 $500,000 0 19,000 519,000 Current liabilities Bond interest payable .................................................... $ 30,000 3. Discount EATSLEEPMUSIC.COM INC. Balance Sheet (Partial) December 31, 2003 Long-term liabilities Bonds payable, due 2013 ......................... Less: Discount on bonds payable .......... 16-47 $500,000 0 ,09,500 490,500 PROBLEM 16-2B (a) 2003 April 01 Cash (98% X $3,000,000) .............. Discount on Bonds Payable ........ Bonds Payable ..................... 2,940,000 60,000 3,000,000 (b) See following page. (c) 2003 1. Oct.0 1 2. Dec. 31 2004 3. April0 1 Bond Interest Expense ................. Discount on Bonds Payable Cash ..................................... Bond Interest Expense ($136,500 X 3/6) .......................... Discount on Bonds Payable ($1,500 X 3/6)..................... Bond Interest Payable ($135,000 X 3/6) ................. Bond Interest Payable .................. Bond Interest Expense ($136,500 X 3/6) .......................... Discount on Bonds Payable ($1,500 X 3/6)..................... Cash ..................................... 16-48 136,500 1,500 135,000 68,250 750 67,500 67,500 68,250 750 135,000 PROBLEM 16-2B (Continued 16-49 PROBLEM 16-2B (Continued (b) Semi-annual Interest Period Apr. 1, 2003 Oct. 31, 2003 Apr. 1, 2004 (A) Interest Payment ($3,000,000 X 9% X 6/12) $135,000 0135,000 (C) Discount (D) Amortization Unamortized ($60,000 20 Discount X 6/12) (D) – (C) (B) Interest Expense (A) – (C) $136,500 0136,500 $1,500 01,500 $60,000 058,500 057,000 (d) KYBERPASS CORP. Balance Sheet (Partial) December 31, 2003 Current liabilities Bond interest payable ...................................................... $ 67,500 Long-term liabilities Bonds payable, due 2023 .......................... $3,000,000 Less: Discount on bonds payable ........... 57,750* 2,942,250 * $60,000 - $1,500 - $750 = $57,750 16-50 (E) Bond Carrying Value [$3,000,000 (D)] $2,940,000 02,941,500 02,943,000 PROBLEM 16-3B (a) (b) 2002 July 01 Cash ....................................................... Premium on Bonds Payable ......... Bonds Payable ............................... 1,686,934 186,934 1,500,000 CLIO CORPORATION Bond Premium Amortization Effective Interest Method—Semi-annual Interest Payments 12% Bonds Issued at 10% Semiannual Interest Period July 1, 2002 Jan. 1, 2003 July 1, 2003 Jan. 1, 2004 (A) (B) Interest Interest Payment Expense $90,000 090,000 090,000 $84,347 084,064 083,767 (C) Premium Amortization (A) – (B) $5,653 05,936 06,233 (D) (E) UnamorBond tized Carrying Premium Value (D) – (C) ($1,500,000 + D) $186,934 0181,281 0175,345 0169,112 (c) 2002 Dec. 31 Bond Interest Expense ($1,686,394 X 10% X 6/12) .................. Premium on Bonds Payable ................. Bond Interest Payable ($1,500,000 X 12% X 6/12) .......... (d) 2003 July 01 Bond Interest Expense [($1,686,934 - $5,653) X 10% X 6/12] . Premium on Bonds Payable ................. Cash ............................................... 16-51 $1,686,934 01,681,281 01,675,345 01,669,112 84,347 5,653 90,000 84,064 5,936 90,000 PROBLEM 16-3B (Continued) (e) 2003 Dec. 31 Bond Interest Expense [($1,681,281 - $5,936) X 10% X 6/12] . Premium on Bonds Payable ................. Bond Interest Payable ................... 16-52 83,767 6,233 90,000 PROBLEM 16-4B (a) Bond Interest Payable = $1,500,000 X 6% X 2/12 = $15,000 (b) Sept. 01 Cash [($1,500,000 X 102%) + $15,000)] ... 1,545,000 Premium on Bonds........................... Bonds Payable .................................. Bond Interest Payable ($1,500,000 X 6% X 2/12) .............. (c) Jan. 1 Bond Interest Expense ............................ Premium on Bonds Payable ($30,000 X 4/118 months)...................... Bond Interest Payable ............................. Cash ($1,500,000 x 6% X 6/12) ......... 16-53 30,000 1,500,000 15,000 28,983 1,017 15,000 45,000 PROBLEM 16-5B (a) 1. 2. 3. 4. 2003 July 0 1 Cash ............................................... Discount on Bonds Payable ......... Bonds Payable ....................... Dec. 31 Bond Interest Expense ($1,947,651 X 6%) ....................... Discount on Bonds Payable . Bond Interest Payable ($2,200,000 X 5%) ................. 2004 July 0 1 Bond Interest Expense [($1,947,651 + $6,859) X 6%] ....... Discount on Bonds Payable . Cash........................................ Dec. 31 Bond Interest Expense [($1,954,510 + $7,271) X 6%] ...... Discount on Bonds Payable . Bond Interest Payable ........... 1,947,651 252,349 2,200,000 116,859 6,859 110,000 117,271 7,271 110,000 117,706 7,706 110,000 (b) WAUBONSEE COMPANY LTD. Balance Sheet (Partial) December 31, 2004 Long-term liabilities Bonds payable......................................... Less: Discount on bonds payable ........ $2,200,000 230,513* * $252,349 – $6,859 – $7,271 – $7,706 = $230,513 16-54 $1,969,487 PROBLEM 16-5B (Continued) (c) Dear Waubonsee Company Ltd. In regards to your questions, interest expense for 2004 under the effective interest method is $234,977 ($117,271 + $117,706). The effective-interest method will result in less interest expense reported than the straight-line method in 2004 when the bonds are sold at a discount. Straight-line interest expense for 2004 is $245,234 ($110,000 + $12,617 = $122,617 X 2), compared to $234,977 ($117,271 + $117,706) under the effective-interest method. The total cost of borrowing over the life of the bonds will equal the total of all the interest payments plus the discount on the bonds: Semi-annual interest payments ($2,200,000 X 10% X 10) ........................................ Add: Bond discount .............................................. Total cost of borrowing........................................... $2,200,000 00,252,349 $2,452,349 Interest expense will be exactly the same regardless of the method of amortization used. The choice of amortization methods will determine the amount of the discount to be amortized each period. While the different methods will cause the amortization to be different in each period, the overall amount of amortization will be the same—it will always equal the amount of the discount. The advantage of the effective rate method is that it uses a constant rate of interest. The effective-interest method results in a varying amount of interest expense but a constant rate of interest on the balance outstanding. Accordingly, it results in a better matching of expenses with revenues than the straight-line method. However, the straight-line method is simpler and easier to apply. 16-55 PROBLEM 16-6B (a) $90,000 X 2 6% $3,000,000 (b) July 1 Bond Interest Expense ......................... Premium on Bonds Payable ($200,000 ÷ 5 X 6/12) .......................... Cash ($3,000,000 X 3%) ......... 70,000 20,000 90,000 (c) Percentage of bonds redeemed = $1,200,000 ÷ $3,000,000 = 40% July 01 Bonds Payable ........................................ 1,200,000 Premium on Bonds Payable [($200,000 – $20,000) X 40%] ............... 72,000 Gain on Bond Redemption ............. Cash ($1,200,000 X 99%) ................. (d) Dec. 31 Bond Interest Expense ........................... Premium on Bonds Payable ................... Bond Interest Payable ($1,800,000 X 3%) ......................... 84,000 1,188,000 42,000 12,000** 54,000 **$200,000 – $20,000 – $72,000 = $108,000; $108,000 9 periods = $12,000 16-56 PROBLEM 16-7B (a) Semi-annual Interest Period Dec. 31, 2003 June 30, 2004 Dec. 31, 2004 June 30, 2005 Dec. 31, 2005 Cash Payment $44,000 042,800 041,600 040,400 Interest Expense Reduction of Principal $24,000 022,800 021,600 020,400 $400,000 0380,000 0360,000 0340,000 0320,000 $20,000 20,000 20,000 20,000 (b) 2003 Dec. 31 Cash ........................................................... Mortgage Note Payable ..................... 400,000 2004 June 30 Interest Expense ....................................... Mortgage Note Payable ............................ Cash ................................................... 24,000 20,000 Dec. 31 Interest Expense ....................................... Mortgage Note Payable ............................ Cash ................................................... Principal Balance 400,000 44,000 22,800 20,000 42,800 (c) ELITE ELECTRONICS Balance Sheet (Partial) December 31, 2004 Current liabilities Current portion of mortgage note payable ..... Long-term liabilities Mortgage notes payable .................................. $ 40,000 320,000* * $360,000 - $40,000 = $320,000 or see Dec. 31, 2005 balance 16-57 PROBLEM 16-8B (a) Choi Inc. should record the SameDay Delivery lease as a capital lease because (1) the lease term is greater than 75% of the estimated economic life of the leased property and (2) the present value of the lease payments is 90% or more of the fair market value of the computer. It should be noted that only one condition need be met to require capitalization. Both the Duncan Co. and Riverview Auto leases should be reported as operating leases, because none of the conditions is met to require treatment as a capital lease. (b) The SameDay Delivery lease is a capital lease. The entry to record the capital lease on January 1, 2003 therefore is as follows: Leased Asset—Computer ............................................ Lease Liability ....................................................... 31,000 31,000 The Duncan Co. lease is an operating lease. The entry to record the lease payment in 2003 therefore is as follows: Rent Expense ................................................................ Cash ....................................................................... 4,200 4,200 This entry would be made on the date the rental payment is due. The Riverview Auto lease is an operating lease. The entry to record the lease payment in 2003 therefore is as follows: Rent Expense ................................................................ Cash ....................................................................... 3,700 This entry would be made on the date the rental payment is due. 16-58 3,700 PROBLEM 16-8B (Continued) (c) Since the Duncan Co. lease and Riverview Auto lease do not qualify as a capital leases, nothing would appear on Choi’s balance sheet regarding either the delivery equipment or the automobile. As well, no amount payable under the terms of the lease arrangement will appear on Choi’s balance sheet. The annual rental fees would simply be charged to expense when they are paid each year. The SameDay Delivery lease is a capital lease. Therefore, the computer would be recorded as an asset on Choi’s balance sheet. A corresponding liability for leased assets would also be recorded. 16-59 PROBLEM 16-9B (a) ($ in thousands) 1. Debt to total assets = Total debt ÷ Total assets 2000 1999 $2,073,335 ÷ $2,890,999 = 71.7% $2,128,828 ÷ $2,878,817 = 73.9% 2. Interest coverage = EBIT ÷ Interest expense 2000 1999 ($80,246 + $77,541 + $88,875) ÷ $88,875 = 2.8 times [($8,074) + ($10,197) + $46,301] ÷ $46,301 = 0.6 times 3. Cash interest coverage = EBITDA ÷ Interest expense (b) 2000 $80,246+$77,541+$88,875+$98,055 3.9 times $88,875 1999 ($8,074)+($10,197)+$46,301+$72,415 2.2 times $46,301 Sears is financing over 70% of their assets with debt instead of equity. This is very high. Their solvency has improved over the past year because they had net income in the current year versus a loss last year. 16-60 BYP 16-1 FINANCIAL REPORTING PROBLEM (a) Long-term debt as at June 24, 2000 is $10,250,000. This is a decrease of $9,050,000 from the 1999 proforma numbers. (b) Second Cup’s current portion of long-term debt is $3,000,000. (c) The long-term debt consists of a non-revolving term facility secured by the Company’s investment in Diedrich Coffee, Inc. (d) The company has no capital leases but does have commitment under operating leases. Per Note 12 to the 2000 financial statements, these commitments total $3,761,000. 16-61 BYP 16-2 INTREPRETING FINANCIAL STATEMENTS (a) ($ in thousands) Reitmans La Senza Debt to assets Total debt ÷ Total assets $59,728 23.5% $253,849 Interest coverage Cash interest coverage $108,588 48.8% $222,590 EBIT ÷ Interest expense $51,707+$20,159+$608 $608 119.2 times $6,070+$4,855+$486 $486 23.5 times EBITDA ÷ Interest expense EBITDA ÷ Interest expense $51,707+$20,159+$608+$12,371 $6,070+$4,855+$486+$15,284 $608 $486 139.5 times 54.9 times Reitmans has much less debt in relation to its assets than does La Senza. Accordingly, it has much less interest on a percentage basis. This makes Reitmans more comfortable with regards to the ability to remain solvent. However, even though La Senza carries more debt, it appears to be more than able to meet its interest requirements. Therefore, any additional returns accrue to the shareholders. Using debt to finance assets can be a benefit to the existing shareholders so long as the company can afford to pay its interest and principal payments which it appears is the case with both Reitmans and La Senza. (b) If the company has obligations under lease, this reduces the cash available to repay interest and principal payments on their debt. The company is therefore at a greater risk of becoming insolvent. 16-62 BYP 16-3 INTREPRETING FINANCIAL STATEMENTS (a) Coupon is the contractual rate; yield is the market (effective) rate. (b) The coupon rates have the widest range. They are set by the issuers of the bonds. The effective rates, on the other hand, are set by market forces. (c) The yield rate gets higher as the term to maturity gets longer. This is logical because it requires more incentive to lend money for the longer term, since there is greater risk. (d) Government of Canada bonds have the lowest yield rates because they involve the least risk. (e) Most of the bonds listed are selling at a premium, because interest rates moved to lower levels after they were issued. 16-63 BYP 16-4 ACCOUNTING ON THE WEB Due to the frequency of change with regard to information available on the world wide web, the Accounting on the Web cases are updated as required. Their suggested solutions are also updated whenever necessary, and can be found on-line in the Instructor Resources section of our home page [www.wiley.com/canada/weygandt2]. 16-64 BYP 16-5 ACCOUNTING ON THE WEB Due to the frequency of change with regard to information available on the world wide web, the Accounting on the Web cases are updated as required. Their suggested solutions are also updated whenever necessary, and can be found on-line in the Instructor Resources section of our home page [www.wiley.com/canada/weygandt2]. 16-65 BYP 16-6 COLLABORATIVE LEARNING ACTIVITY (a) Discount calculation = $1,200,000 – ($1,200,000 X 97%) = $36,000 Amortization $36,000 ÷ 10 = $3,600 per period Unamortized discount = $36,000 – $14,400 ($3,600 X 4 periods) = $21,600 Carrying value of bonds = $1,200,000 – $21,600 = $1,178,400 (b) Jan. 1 1 Bonds Payable .............................. 1,200,000 Discount on Bonds Payable ........... Cash ........................................ Gain on Retirement of Bonds 21,600 1,000,000 178,400 Cash ................................................ Bonds Payable ....................... 1,000,000 16-66 1,000,000 BYP 16-6 (Continued) (c) MEMO To: From: Date: Re: Barbara Landry Student Bond Retirement In considering your repurchase proposal there are several economic factors you should consider. 1. You should consider what will happen with interest rates in the future. If interest rates are expected to fall further over the next several months you may want to consider delaying the refinancing. 2. You need to consider the cost of refinancing. There will be significant costs associated with the refinancing such as the issue costs related to the new bonds. You will need to ensure that the cost savings from the refinancing are sufficient to cover these additional costs. 16-67 BYP 16-7 COMMUNICATION ACTIVITY To: Finn Berge From: I. M. Student Subject: Bond Financing The advantages of bond financing over common share financing include: 1. 2. 3. 4. Shareholder control is not affected. Income tax savings result. Income to common shareholders may increase. Earnings per share may be higher. The types of bonds that may be issued include: 1. 2. 3. 4. 5. 6. Secured or unsecured bonds. Term or serial bonds. Term bonds mature at a single specified date, while serial bonds mature in instalments. Registered or bearer bonds. Registered bonds are issued in the name of the owner, while bearer bonds are not. Convertible bonds, which can be converted by the bondholder into common shares. Redeemable or callable bonds, which are subject to early retirement by the issuer at a stated amount. Retractable bonds, which can be redeemed prior to maturity at a stated amount, at the option of the bondholder. Provincial laws grant corporations the power to issue bonds after formal approval by the board of directors and shareholders. The terms of the bond issue are set forth in a legal document called a bond indenture. After the bond indenture is prepared, bond certificates are printed. Bonds which are to be sold to the public (rather than through a private placement) usually require the approval of a securities commission. 16-68 BYP 16-8 ETHICS CASE (a) The stakeholders in the Custom case are: Andy Vicks: president, founder, and majority shareholder. Jill Caterino, minority shareholder. Other minority shareholders. Existing creditors (debt holders). Future bondholders. Employees, suppliers, and customers. (b) The ethical issues: The desires of the majority shareholder (Andy Vicks) versus the desires of the minority shareholders (Jill Caterino and others). Doing what is right for the company and others versus doing what is best for oneself. Questions: Is what Andy wants to do legal? Is it unethical? Is Andy's action brash and irresponsible? Who may benefit/suffer if Andy arranges a high-risk bond issue? Who may benefit/suffer if Jill Caterino gains control of Custom? Note that Andy may genuinely believe that his retaining control of the company is in the best interests of others—such as employees—as well as serving his interests. (c) The rationale provided by the student will be more important than the specific position, because this is a borderline case with no right answer. 16-69