Forecasting returns I know you can`t forecast the future but what

advertisement

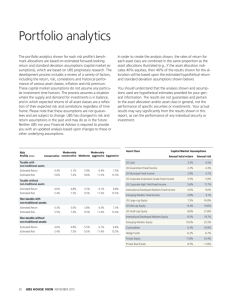

Forecasting returns I know you can’t forecast the future but what return can I reasonably expect from my investment? This is a question all of us would love to have an answer to. As you know, I am sceptical about short term forecasts. If you were asked what will the weather be like on 18 January you could make a guess. You might be lucky and be right. If you asked me what is Joburg’s climate like, using long term results I would have a better chance of guessing (estimating) how many sunny days we will have in 2014. If I look at investment returns since 1900 I can assume that equities will give you a better return than bonds or cash. I can also tell you that equity values will fluctuate much more than those of bonds or cash. While I can tell you what the average annual rates of return have been for each asset class, I can also safely predict that in no one year will you receive the average return. Like you, however, I would love to be able to know that over the next year I can anticipate a return of, say, 11 per cent. I can’t. What I can do is share with you the view of people who are much more courageous at forecasting future returns than I am. In the latest quarterly Stanlib publication there is an article by Vaughan Henkel, Investment Strategist at Stanlib and Olga Cukrawska, technical marketing manager at Stanlib, entitled “Offshore Equity Returns are More Attractive on a Four Year View”. In this article they look at possible returns for the different asset classes over the next four years. They also state the assumptions they are using to arrive at their conclusions and the returns they expect. When making forecasts it is essential to know the assumptions on which those forecasts are based. A change in any on of the assumptions can impact on the final estimate. Their assumptions and anticipated results are attached. Working on their assumptions I created 3 portfolios and calculated the expected return before costs. The asset mixes of 3 portfolios as well as the expected return are given in the table below. US Equity US Bonds SA Equity SA Bonds SA Property SA Cash Expected return before inflation Expected return after inflation 35% 0% 35% 10% 10% 10% 11.13% Percentage allocation 25% 0% 25% 20% 10% 20% 10.10% 15% 0% 15% 30% 10% 30% 9.11% 5.33% 4.30% 3.31% A few points need to be made. These returns do not take into account costs. They do not take into account that different portfolio managers will have different returns. We like to think that our managers will continue to outperform the average sufficiently to cover costs. Returns on equity are volatile. A good year can boost performance considerably, as it did in 2013. A poor year can have the opposite effect. The figures, however, are logical. If you want higher returns you will have a riskier portfolio than someone who has a lower tolerance for risk. Likewise, the lower the risk, the lower the return. Kind regards Brian