3_sc_c_2_thalassinos-muratoglu

advertisement

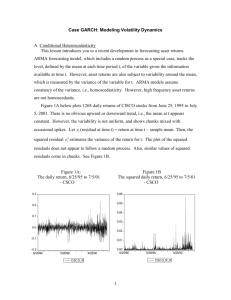

Comparison of Forecasting Volatility in the Czech Republic Stock Market EleftheriosThalassinos1Yusuf Muratoglu2ErginbayUgurlu3 Abstract This paper examined three GARCH models with three different distributions for comparing their forecasting power for volatility of the return of Czech stock market, PX index for the period 08.01.20001 -20.07.2012. We employ GARCH, GJR-GARCH and EGARCH modelsagainst Normal, Student-t and Generalized Error distributions. Then we forecast stock market volatility for Czech Republic by its return using GARCH, GJR-GARCH and EGARCH model and compare their forecasting performance. The results show that return volatility can be characterized by significant persistence and asymmetric effects. We estimate estimated variance for all models for full sample period using static forecast. After comparing the forecast performance of all nine models, it was found that the EGARCH model has the best forecast performance comparing other models. 1. Introduction Financial data mostly have some features which are leptokurtosis, volatility clustering or volatility pooling and leverage effects.Linear structural (and time series) models are unable to explain a number of the important features. Leptokurtosis, volatility clustering or volatility pooling and leverage effects are tendency for financial asset returns. The tendencies of these features are defined as; to have distributions that exhibit fat tails and excess peakedness at the mean, to have volatility in financial markets to appear in bunches which means large returns (of either sign) are expected to follow large returns, and small returns (of either sign) to follow small returns and to have volatility tends to rise more following a large price fall than following a price rise of the same magnitude respectively (Brooks, 2008:380) The most popular non-linear financial models are the Autoregressive Conditional Heteroscedastic (ARCH) or Generalized Autoregressive Conditional Heteroscedastic (GARCH) models used for modeling and forecasting volatility that are proposed by Engle (1982) and Bollerslev (1986) . In this paper, we investigate stock market volatility for Czech Republic by its return using GARCH, GJR-GARCH and EGARCH model and compare their forecasting performance. The authors would like to thank Prof. Ph.D. BurcUlengin for useful comments. All remaining errors are solely ours 1Professor, Department of Maritime Studies, University of Piraeus,Chair Jean Monnet, e-mail:thalassic@unipi.gr 2 Research Assistant, Gazi University FEAS, Department of Economics,email:yusufmuratoglu@hitit.edu.tr 3 Instructor Ph.D., Hitit University FEAS, Department of Economics, e-mail:erginbayugurlu@hitit.edu.tr 1 The rest of the paper is organized as follows. The next section is literature review of related subject of GARCH models and stock market volatility. The third section gives brief information about ARCH/GARCH models and the estimation results are presented in the fourth section. The five section summarizes and concludes the paper. 2. Literature Review Andersen et al.(1999) stated that the expected future volatility of financial market returns is the main ingredient in assessing asset or portfolio risk and plays a key role in derivatives pricing models. Emerson et al. (1996) investigate Bulgarian stock market and Scheicher (1999) studies Polish stock returns, Shields (1997) modeling returns for the Warsaw and Budapest stock exchanges returns. Also Scheicher(2001) analyses the movements of the short rates of emerging markets in Central and Eastern Europe.Scheicher (2001) calledHungary, Poland and Czech markets as a principal emerging stock markets in Europe. The author estimate a VEC model and modeling its volatility with a Multivariate GARCH (M-GARCH) model. The findings shows that countries which are investigated have limited interaction and their volatility have a regional character. Vošvrda and Žıkeš (2004) study the behavior of volatility and the distributional properties of the Czech, Hungarian and Polish stock markets data for the period 1996- 2002 period using weekly data. They use PX-50 index for Czech Republic and find that statistically significant results for GARCH (1,1) model and conclude that the volatility of the returns on PX-50 is very persistent. Syriopoulos (2007) investigates the relationships between Czech Republic, Hungary, Poland, Slovakia as a emerging stock markets and Germany, US as a developed stock markets over the period 1997-2003.Haroutounian and Price (2010) investigate Czech Republic, Hungary, Poland and Slovakia using both univariate and multivariate GARCH models that are GARCH, NGARCH, EGARCH, GJR-GARCH, AGARCH, NAGARCH and VGARCH. Paper has two parts which are univariate models part and multivariate models part. Based on the univariate models they conclude that strong GARCH effects are apparent for all four markets with exception of Czech Republic where the coefficient of the lagged squared returns is not significant in three out of seven specifications of conditional volatility. Hajek (2007) tests the Efficient Market Hypothesis on the Czech capital market for 1995–2005 period for monthly, weekly and daily data.. The author analyses efficiency and linear dependency of several index closing values and stock closing prices on the Prague Stock Exchange and concludes that both daily stock returns and daily index returns are significantly linearly dependent and the heteroskedasticity-consistent methodology must be therefore applied to avoid significant biases. Rockinger and Urga (2012) investigate two groups of country which are transition economies and established economies. Transition economies are; CzechRepublic, Poland, Hungary and Russia, established economies are USA, Germany and UK. Although they focus on a sample of Central and Eastern European Financial Markets (CEEFM)4 they only use these four countries. The model results are very similar for the Czech Republic, Hungary, and Polandand for all countries investigated there exist significant GARCH effects. 3. Methodology We use three different types of GARCH models which are GARCH, GJR-GARCH and EGARCH model. 4 Czech Republic , Poland, Hungary, Russia, Bulgaria, Slovenia, Romania, Croatia and Estonia 2 ARCH Model ARCH models based on the variance of the error term at time t depends on the realized values of the squared error terms in previous time periods. The model is specified as: yt u t (1) u t ~ N0, h t q h t 0 j u 2t i (2) t 1 This model is referred to as ARCH(q), where q refers to the order of the lagged squared returns included in the model. If we use ARCH(1) model it becomes h t 0 1 u 2t 1 (3) Since h t is a conditional variance, its value must always be strictly positive; a negative variance at any point in time would be meaningless. To have positive conditional variance estimates, all of the coefficients in the conditional variance are usually required to be nonnegative. Thus coefficients must be satisfy and . GARCH Model Bollerslev (1986) and Taylor (1986) developed the GARCH(p,q) model . The model allows the conditional variance of variable to be dependent upon previous lags; first lag of the squared residual from the mean equation and present news about the volatility from the previous period which is as follows: q p i 1 i 1 h t 0 i u 2t i i h t i (4) In the literature most used and simple model is the GARCH(1,1) process, for which the conditional variance can be written as follows: h t 0 1 u 2t 1 1 h t 1 (5) Under the hypothesis of covariance stationarity, the unconditional variance h t can be found by taking the unconditional expectation of equation 5. We find that h 0 1h 1h (6) Solving the equation 5 we have h 0 1 1 1 (7) For this unconditional variance to exist, it must be the case that 1 1 1 and for it to be positive, we require that 0 0 . GJR GARCH The GJR model is a simple extension of GARCH with an additional term added to account for possible asymmetries (Brooks, 2008:405).Glosten, Jagananthan and Runkle 3 (1993) develop the GARCH model which allows the conditional variance has a different response to past negative and positive innovations. q p i 1 i 1 ht 0 i ut2i i ut2i d t 1 j ht j where (8) is a dummy variable that is: 1 if u t 1 0, bad news d t 1 0 if u t 1 0, good news In the model, effect of good news shows their impact by i , while bad news shows their impact by . In addition if 0 news impact is asymmetric and 0 leverage effect exists. To satisfy non-negativity condition coefficients would be 0 0 , i 0 , 0 and i i 0 . That is the model is still acceptable, even if i 0 , provided that i i 0 (Brooks, 2008:406). Exponential GARCH Exponential GARCH (EGARCH) proposed by Nelson (1991) which has form of leverage effects in its equation. In the EGARCH model the specification for the conditional covariance is given by the following form: log ht 0 j log ht j i q p j 1 i 1 u t i ht i r k k 1 ut k ht k (9) Two advantages stated in Brooks (2008) for the pure GARCH specification; by using log ht even if the parameters are negative, will be positive and asymmetries are allowed for under the EGARCH formulation. In the equation k represent leverage effects which accounts for the asymmetry of the model. While the basic GARCH model requires the restrictions the EGARCH model allows unrestricted estimation of the variance (Thomas and Mitchell2005:16). If k 0 it indicates leverage effect exist and if k 0 impact is asymmetric. meaning of leverage effect bad news increase volatility. The Applying process of GARCH models to return series, it is often found that GARCH residuals still tend to be heavy tailed. To accommodate this, rather than to use normal distribution the Student’s t and GED distribution used to employ ARCH/GARCH type models (Mittnik et al. 2002:98). 4. Empirical Application We use daily data in stock exchanges of Czech Republic PX5 for the period 08.01.20001 -20.07.2012. Data collected from Reuters.We use return, which is in Yu (2002), defined as follows: 5 See: http://www.pse.cz/dokument.aspx?k=Exchange-Indices for description of PX 4 x r log t x t 1 where as a RPX. (10) is capital index. Figure 1 shows graph of PX and its return which is defined .15 2,000 .10 1,600 .05 1,200 .00 -.05 800 -.10 400 -.15 1/2/12 1/3/11 1/1/10 1/1/09 1/1/08 1/1/07 1/2/06 1/3/05 1/1/04 1/1/03 1/2/12 1/3/11 1/1/10 1/1/09 1/1/08 1/1/07 1/2/06 1/3/05 1/1/04 1/1/03 1/1/02 1/1/02 -.20 0 RPX PX Table 1: Descriptive Statistics RPX Mean 0.000210 Median 0.000721 Maximum 0.123641 Minimum -0.161855 Std. Dev. 0.015431 Skewness -0.524060 Kurtosis 15.43870 Jarque-Bera 18821.75 Probability 0.000000 Sum 0.609240 Sum Sq. Dev. 0.690062 Observations 2899 Table 1 summarizes descriptive statistics of PX, RPX have negative skewness and high positive kurtosis. These values signify that the distributions of the series have a long left tail and leptokurtic. Jarque-Bera (JB) statistics reject the null hypothesis of normal distribution at the 1% level of significance for the variable. Table 2 shows Augmented Dickey-Fuller (ADF) test results and concludes that RPX is stationary. 5 Table 2: ADF Test Results Without Trend ADF stat p -39.7972*** 0.0000 Variable RPX With Trend ADF stat p -39.8306*** 0.0000 Note: *** denotes significant at the 1% level We test mean model for the ARCH effect by ARCH-LM Test. Table 3 shows ARCHLM test results. If the value of the test statistic is greater than the critical value from the distribution, the null hypothesis is rejected. Table 3 : ARCH (1) Test Results Dependent Variable of Model RPX ARCH(1)LM Stat 429,7907*** P 0.0000 Note: *** denotes significant at the 1% level. The hull hypothesis, there is no ARCH effect is rejected. It is stated in We employ GARCH, GJR-GARCH and EGARCH model using both Student-t and Generalized Error distributions additional to Normal distribution. Results show that (Appendix: Table1, Table 2, Table 3) that strong GARCH and GJR-GARCH effects are apparent for returns. The sum of coefficient of and less than one in GARCH and GJRGARCH model for all distribution. Nevertheless the estimate of is smaller than the estimate of in both cases that is to show negative shocks haven’t a larger effect on conditional volatility than positive shocks of the same magnitude. In GJR-GARCH model 0 the news impact is asymmetric on the other words bad news increase volatility. In the E-GARCH model negative and significant leverage effect parameter indicating the existence of the leverage effect in returns. If GED parameter (r)equals two it means normal distribution if it is less than two it means leptokurtic distribution. In all models r is less than two and statistically significant which indicate that RPX is leptokurtic. This result is consistent with the skewness values shown in Table 1 . After all model are estimated ARCH effect is tested and except GJR-GARCH model in normal distributionis rejected in %10 level, the null hypothesis that there is no ARCH effect cannot be rejected for all models (see: Appendix) . The in-sample evidence provides the history performance of models. We estimate estimated variance for all models for full sample period using static forecast. Then we compare forecasting performance of models which are used in this paper. We consider four statistics as the forecasting error criterions which are employed in Wang and Wu(2012 ). Four measures are used to evaluate the forecast accuracy for full samplenamely, Mean Square Error (MSE) andMean Absolute Error (MAE): n MSE1 n 1 2t ˆ 2t 2 (11) t 1 6 MSE 1 n 1 t ˆ t n 2 (12) t 1 n MAE 1 n 1 2t ˆ 2t (13) t 1 n MAE 2 n 1 t ˆ t (14) t 1 2 ˆ2 where, n is the number of forecasts, t is the actual volatility and t is the volatility forecast at day t. Table 4 reports the forecasting performance of the GARCH, GJR-GARCH and EGARCH models. Generally, we find that EGARCH model have the greatest forecasting accuracy according to MSE2, MAE1 and MAE2, only MSE1 shows GJR-GARCH is better performance. Table 4:ComparisonForecasting Performance of GARCH Models Normal Distribution Student t Distribution GED GJRGJRGJRGARCH GARCH EGARCH GARCH GARCH EGARCH GARCH GARCH EGARCH MSE1 6.30E-07 6.05E-07 6.25E-07 6.31E-07 6.08E-07 6.29E-07 6.31E-07 6.06E-07 6.27E-07 MSE2 0.000480 0.000478 0.000460 0.000478 0.000477 0.000459 0.000478 0.000476 0.000459 MAE1 0.000243 0.000239 0.000234 0.000242 MAE2 0.015476 0.015387 0.015342 0.015447 Note: The values in bold face refer to smallest loss. 0.000239 0.000234 0.000242 0.000239 0.000234 0.015398 0.015321 0.015439 0.015387 0.015315 5. Conclusion This paper examined three GARCH models namely GARCH, GJR-GARCH and EGARCH model with three differentdistributionswhich are Normal, Student-t and Generalized Error distributions for comparing their forecasting power for volatility of the return of Czech stock market, PX index. All models are employed and their coefficients are interpreted. The results show that significant ARCH and GARCH effects are present in the data indicates that return volatility can be characterized by significant persistence and asymmetric effects consistent with papers Rockinger and Urga (2012), Haroutounian and Price (2010), Vošvrda And Žikeš (2004) which has GARCH type models to Czech stock market. Finally we compare the insampleforecasting performance of all nine models. The evidence shows that the EGARCH model has a best forecast performance under most of the loss criterions 7 REFERENCES Andersen T. G.,Bollerslev T., Lange S.(1999), “Forecastingfinancial market volatility: Samplefrequencyvis-a-visforecasthorizon”, Journal of Empirical Finance,Volume 6, Issue 5, 457-477. Bollerslev, T., (1986) “GeneralizedAutoregressiveConditionalHeteroskedasticity”. Journal of Econometrics, Vol. 31, issue 3, pages 307-327 . Bollerslev, T., (1987). “A ConditionalHeteroskedastic Time Series Model ForSpeculativePricesAndRates Of Return”. Review of EconomicsandStatistics 69, 542–547. Brooks C.,(2008) “IntroductoryEconometricsFor Finance: Second Edıtıon ” CambrıdgeUnıversıtyPress Emerson, R.,Hall, S. andZelweska-Mitura, A. (1997) “Evolving Market Efficiencywith an Application toSomeBulgarianShares” , Economics of Planning, Volume 30, 75-90 Engle, R.F., (1982) “AutoregressiveConditionalHeteroskedasticityWithEstimates of TheVariance Of UK İnflation”, Econometrica 50, 987–1008. Glosten, L.R.,Jagannathan, R. AndRunkle, D. (1993) “On TheRelationBetweenTheExpectedValuesAndTheVolatility Of The Nominal Excess Return On Stocks”, Journal of Finance 48, 1779–1801. Hájek J. (2007), “CzechCapital Market Weak-Form Efficiency, SelectedIssues” , PragueEconomicPapers, 4, 303-318 Haroutounıan M. K. andPrice S. (2001) “Volatility İn TheTransitionMarkets of Central Europe”, Applied Financial Economics, 11, 93-105 Mittnik S.,Paolella M.S. Rachev S.T (2002) “Stationarity Of StablePowerGARCH Processes”, Journal Of Econometrics, 106, 97–107 Nelson, D. B. (1991). ConditionalHeteroscedasticity İn AssetReturns: A New Approach. Econometrica, 59(2), Rockinger, M.,Urga, G., (1999) Time VaryingParameters Model To Test ForPredictabilityAndİntegration İn StockMarkets Of TransitionEconomies”. Cahier De RechercheDuGroupeHec 635/1998. Scheicher, M. (1999). ”ModelingPolishStockReturns.” in Helmenstein, C., ed., CapitalMarkets in TransitionEconomies. Cheltenham, UK : Edward Edgar, pp. 417–437. 8 Scheicher , M., (2001). “TheComovements Of StockMarketsInHungary, Poland AndTheCzechRepublıc” InternatıonalJournal Of FınanceAndEconomıcsInt. J. Fin. Econ. 6: 27–39 Shields K., ( 1997) “Stock Return Volatility On EmergingEasternEuropeanMarkets”, The Manchester School Supplement: 118– 138. Syriopoulos, T., (2007) DynamicLinkagesBetweenEmergingEuropeanAndDevelopedStockMarkets: Has TheEmuAnyİmpact? “, International Review Of Financial Analysis 16, 41-60. Taylor, S. J. (1986), Modelling Financial Time Series, John Wiley&Sons, Chichester. Thomas S. andMitchell H. (2005) “GARCH Modeling of HighFrequencyVolatility in Australia’sNationalElectricity Market”, DiscussionPaper. Melbourne Centrefor Financial Studies, Vošvrda M. andŽıkeš F. (2004). “An Applıcatıon Of TheGarch-t Model On Central EuropeanStockReturns” PragueEconomıcPapers, 1, 26-39 Wang, Y.,Wu, C.(2012). “ForecastingEnergy Market Volatility Using GARCH Models: Can MultivariateModelsBeatUnivariateModels?”, EnergyEconomics. Yu , J., (2002). “ForecastingVolatility in the New ZealandStock Market”, Applied Financial Economics, 2002, 12, 193-202 9 APPENDIX Table 1: Normal Distribution GARCH(1,1) GJR-GARCH E GARCH Value p Value p Value p 0.0009 0.0000 0.0006 0.0023 0.0005 0.0055 0 4.69E-06 0.0000 6.07E-06 0.0000 -0.5147 0.0000 0.1318 0.0000 0.0727 0.0000 0.2531 0.0000 - - 0.1036 0.0000 -0.0687 0.0000 0.8496 0.0000 0.8441 0.0000 0.9636 0.0000 AIC -5.9192 -5.9291 -5.9282 SIC -5.9110 -5.9188 -5.9179 DW-stat 1.8863 1.8888 1.8890 Meanequation 0 Variationequation ARCH-LM (1) Test p-value of ChiSq Obs. 0.306626 0.0846 0.1493 2899 Table 2: Student’s T Distribution GARCH(1,1) GJR-GARCH E GARCH Value p Value p Value p 0.0009 0.0000 0.0008 0.0000 0.0008 0.0001 4.34E-06 0.0000 5.36E-06 0.0000 -0.4700 0.0000 0.1192 0.0000 0.0696 0.0000 0.2354 0.0000 - - 0.0895 0.0000 -0.613 0.0000 0.8617 0.0000 0.8563 0.0000 0.9673 0.0000 Meanequation 0 Variationequation 0 AIC -5.9526 -5.9583 -5.9577 SIC -5.9423 -5.9459 -5.9453 DW-stat 1.8855 1.8872 1.8873 0.3879 0.1387 0.2596 ARCH-LM(1) Test p-value of ChiSq. Obs. 2899 10 Table 3: GeneralizedError Distribution(GED) GARCH(1,1) GJR-GARCH E GARCH Value p Value p Value p 0.0009 0.0000 0.0007 0.0001 0.0007 0.0002 4.56E-06 0.0000 5.72E-06 0.0000 -0.4947 0.0000 0.1256 0.0000 0.0712 0.0000 0.2446 0.0000 - - 0.0960 0.0000 -0.0646 0.0000 0.8546 0.0000 0.8495 0.0000 0.9653 0.0000 r 1.5083 0.0000 1.534154 0.0504 1.5329 0.0498 Meanequation 0 Variationequation 0 AIC -5.9427 -5.9493 -5.9484 SIC -5.9324 -5.9369 -5.9360 DW-stat 1.8856 1.8876 1.8878 ARCH-LM (1) Test p-value of ChiSq. 0.2896 0.074 0.1979 Obs. 2899 11