Civil Service CSRS/FERS Benefits Presentation

advertisement

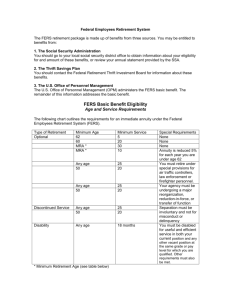

CIVIL SERVICE CSRS/FERS BENEFITS PRESENTATION Presented by: Cherie L. Anderson, LUTCF, ChFEBC℠ Of MetLife L1011212126[exp1212][AL,FL] WHAT IS A CHFEBC℠ PROFESSIONAL? A ChFEBC℠ (Chartered Federal Employee Benefits Consultants) is a prestigious designation for Financial Advisors, CPAs, Attorneys, and certain employees of the Federal Government, who have successfully completed an intensive training course and passed a rigorous examination covering all federal employee benefits. The training consists of a 16 module assignment curriculum. All types of federal employees are covered (such as CSRS, FERS, CSRS Offset, FERS Transferees, Law Enforcement, fire fighters, air traffic controllers, etc. ) The course is available by independent study or a twoday course on-site conducted by a qualified instructor. FERS SYSTEM Basics Retirement Requirements Annuity Survivor Benefits Disability Federal Group Life Insurance TSP Social Security LTC FEHB FERS BASICS Program began 1/1/1987 and continues today Is a three-benefit system Participants contribute 6.2% to social security and .8% to their retirement annuity Typically receive both a retirement annuity and a social security payment CREDITABLE SERVICE Hire date to retirement date if contributions are made. Leave w/o pay up to 6 months in 1 calendar year Workers Comp when returned to work Part-time Service Intermittent when actually employed for days worked, 260 max Break in service up to 3 days Buy back time (deposit service) Before 1/1/89 = 1.3% deposit and full E + C After 1/1/89 or no deposit = No E and No C Redeposit of contributions withdrawn Before 4/7/86 = Full Eligibility and Computation On or After 4/7/86 = Full eligibility, prorated annuity computation Redeposit = Full E and C No redeposit = No E and No C Military Service For service before 1/1/1957 no deposit needed For service after 1/1/57: deposit made = E + C For service after 1/1/57: No deposit made = No E and No C RETIREMENT REQUIREMENTS (AGE)/(YEARS OF SERVICE) Non-Reduced: 62/5, 60/20, MRA+30 Early Out: Any Age w/25- 2% permanent reduction for every year < 55* Reduction in Force (RIF): 50/20 DCS Separation: 50/20, Any Age/25, 2% reduction for every year < 55* Disability: Any Age w/5 Deferred: 62 w/5 * Reduction may be waived FERS ANNUITY Under 62 with less than 20 yrs (1% x Hi- 3 x yrs of service ) Age 62 with more than 20 yrs (1.1% x Hi- 3x yrs of service) Special Retirement Supplement: MRA + 30yrs. or 60/20 FERS will receive their age 62 S.S. benefit until they reach 62 Earnings test: 0-$14,160 @ no penalty, $1 reduction for every $2 over. Early out or involuntary also receive the supplement if they have reached MRA No matter when FERS retires, the annuity begins on the first of the next month COLAs begin at age 62 FERS SURVIVOR BENEFIT Cost 10% of annuity and provides a 50% survivor benefit Partial Survivor Benefit cost 5% and provides a 25% benefit At least some benefit must be kept to maintain FEHB Children’s benefit is reduced by any SS received Death < 10 yrs. of service, spouse gets $15,000 adjusted by 12/1/87 dollars ($29,722 in 2010) + 50% of salary or High-3, whichever is greater. More than10yrs, Lump Sum same as above + 50% of basic annuity without reduction and the special retirement supplement if spouse is younger than 60. FERS DISABILITY Must apply for SSI prior to applying for DI. 1st year disability is 60% of High 3 reduced by 100% SSI 2nd year until Age 62 is 40% of High 3 reduced by 60% of SSI At age 62 the benefit is recomputed to include all yrs worked plus all yrs on disability with COLAs FEGLI Basic: Present salary rounded up to the next $1,000 + $2,000 Extra benefit: Same as basic and is free, but reduces by 10% per year at 35. Option A: $10,000 (includes AD&D) Option B: 1-5 x Salary Option C: $2,500 child/$5,000 spouse x 1-5 BASIC LIFE INSURANCE IN RETIREMENT: Option A 1% reduction per month at retirement or at 65, whichever is later, until it reaches 50% of the Basic amount. Has only one option in retirement At 65 will decrease until there is only 25% remaining There is no cost after age 65 $.60/$1000 cost per month after age 65 No reduction $1.83/$1000 per month after age 65 OPTION B AND C Option B: Reduces after age 65 until there is nothing left No premiums after age 65 or retirement, whichever is later Keep coverage for life, Premiums increase at age intervals Option C: Employee must keep basic coverage Coverage reduces at 2% per month at age 65 Premiums stop at age 65 or retirement, whichever is later If the retiree chooses to continue the coverage Premiums will increase at age intervals TSP FERS can contribute $16,500 per year, $5,500 extra if over 50 1% government contribution regardless of individual participation Up to 5%of the FERS contributions matched FERS must work for 3 years to be vested FERS are immediately vested in their own contributions TSP FUND CHOICES G – Government Securities F – Fixed Income C – Common Stock S – Small Cap I – International There are 5 Lifecycle funds: Rebalanced daily and adjusted quarterly to maximize return for given risk. They are managed by Mercer Investment Consulting with a combination of the 5 TSP funds. L Income – For those taking current income or planning retirement within 2 years. L 20XX – Investment mix that reflects a time horizon for retirement near this date. TSP WITHDRAWAL OPTIONS While working, after age 59 ½ you may make a 1 time in service withdraw. At age 55 or older, there will not be a 10% penalty for any withdrawals if retired or separate from service simultaneously. TSP may be transferred to a Traditional IRA. Lump sump distribution – taxes paid at time of withdrawal. Purchase an annuity through TSP. Take equal monthly payments. Choose amount to be paid. May adjust annually. Use the IRS’s calculation of payments, ie.RMD IN-SERVICE WITHDRAWALS If an employee makes an in-service withdrawal, they may continue to contribute and FERS will match – but their withdrawal options will be limited in retirement. Additional Withdrawal Options: Less than $200 = automatic cash out. If withdrawn before age 55, there is a 10% penalty for early withdrawal plus taxes unless a 72(t) (equal and substantial or life annuity) If funds are withdrawn, other than a transfer, 20% is withheld for taxes. FERS spouse has rights as to how contributions are withdrawn. Spouse must sign a waiver. Former spouse, due to court order, may need a waiver also. SOCIAL SECURITY Calculating S.S. is a 4-steps process: If born between 1929 and 1978 – must earn $50 per quarter. After 1978 - $4,360 at any point = 4 credits for the year Born before 1929 need less than 40 credits After 1929 need 40 credits Once someone has 40, they are eligible for some SS You cannot buy credits, borrow, or inherit them. Determine full SS: Year of birth determines eligibility for full retirement at 65, 66, or 67 All may take a reduced amount at 62 if they have 40 quarters If deferred until age 70, SS will be higher SS tax income limits: Single AGI: $25K - $35K = 50% tax, $35K+ = 85% tax Joint AGI: $32K – $44K = 50% tax, $44K+ = 85% tax. PRIMARY INSURANCE AMOUNT A spouse at full retirement (65-67) may take 100% of their SS or 50% of their spouse’s, whichever is greatest A spouse age 62 may take 80% of PIA or 37.5% of their spouses, whichever is greater A spouse, at any age, caring for children under 16yrs may take 50% of spouse’s PIA A child, unmarried, under age 19 if in high school, or any age if disabled before age 22 may take 50% of worker’s PIA LONG TERM CARE INSURANCE John Hancock is the Federal LTC provider Benefit levels are $100-$450 daily in increments of $50 with benefit periods of 2,3,5 and lifetime Elimination period is 90 days and inflation riders are 4% compound, 5% compound, and GPO Tax qualified, so premiums are deductible if they exceed 7.5% of AGI Available only during open enrollment HEALTH CARE FEDVIP Dental and Vision is available to employees, retirees, and family members FSA: $5,000 medical, $5,000 dependent, use it or lose it March 15. Pre-tax dollars HSA: Must have HDHP. FEHB member owns the account. Unused rolls over HRA: Must be enrolled in HDHP and not HSA No individual contributions allowed. Credits carry over, but are forfeited if member leaves MEDICARE TWO MAIN PARTS: Hospital: Part A Deductible of $1,100 and no premium 1.45% deducted out of each paycheck while working Medical and Doctor:Part B Deductible of $135 and 20% copay The premium $110.50 for new enrollees and $96.40 for current If retired must enroll 3 months prior or 3 months after 65th birthday(7mo. window) General Enrollment January1-March 31 10% penalty for each 12-months late If retired after 65, you have 8 months to enroll with no penalty