pptx - jimakers.com

Chapter 8

1

1.

Understand the various types of common project costs.

2.

Recognize the difference between various forms of project costs.

3.

Apply common forms of cost estimation for project work, including ballpark estimates and definitive estimates.

4.

Understand the advantages of parametric cost estimation and the application of learning curve models in cost estimation.

5.

Discern the various reasons why project cost estimation is often done poorly.

6.

Apply both top-down and bottom-up budgeting procedures for cost management.

7.

Understand the uses of activity-based budgeting and time-phased budgets for cost estimation and control.

8.

Recognize the appropriateness of applying contingency funds for cost estimation.

2

From PMBOK Guide

2004

3

Cost management

has been defined to encompass data collection, cost accounting, and cost control.

Cost accounting

and

cost control

serve as the chief mechanisms for identifying and maintaining control over project costs.

Cost estimation

processes create a reasonable budget baseline for the project.

4

Involves taking financial report information and applying it to projects

Creates an accountability to maintain a clear sense of money management

Encompasses data collection, cost accounting and cost control

Cost a.k.a expenses

5

Labor

◦ Total cost associated with the hiring and paying of various personnel

Materials

◦ Supplies needed during project execution

Subcontractors

◦ Cost for subcontracted labor and services

Equipment & facilities

Travel

6

Direct vs. Indirect

◦ Direct cost are clearly assigned to a specific aspect of the project

◦ Indirect cost are overhead cost of the project including general administration

Recurring (RE) vs. Nonrecurring (NRE)

◦ Recurring are ongoing expenses (i.e. labor)

◦ Nonrecurring are typically a onetime expense (i.e. training)

Fixed vs. Variable

◦ Fixed cost are cost that do not change based on volume usage (i.e. rental rate on a copy machine)

◦ Variable cost do change based on usage (i.e. paper for the copy machine)

Normal vs. Expedited

◦ Normal are expected as part of the routine process

◦ Expedited are unplanned cost to speed up the project execution

7

Name Hours

Needed

Overhead

Charge

Personal

Time Rate

Hourly

Rate

Total Direct

Labor Cost

John

Bill

J.P.

Sonny

40

40

60

25

X 1.80

X

1.80

1.35

1.80

1.12

1.12

1.05

1.12

X $21/hr.

= $1,693.44

$40/hr.

$10/hr.

3,225.60

850.50

$32/hr.

1,612.80

Total Direct Labor Cost =

$7,382.34

8

Costs Examples

Direct Labor

Building Lease

Expedite

Material

X

X

X X

X X

X

X

X

X

X

X X

X

X

X

Other project cost?

9

The first step in determining if a project can be done profitably

Creates a reasonable budget baseline

Identifies needed resources

Creates a time based budget for the needed resources

10

The more clearly you can define the projects’ cost categories in the beginning, the less need there is for estimation

It is best to cost out each work package individually, rather than creating an overall project cost

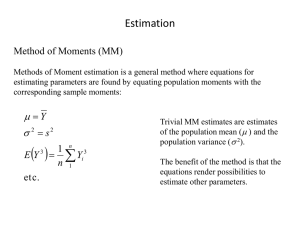

Methods of cost estimation

◦ Ballpark - gueestimate ±30% accuracy

◦ Comparative – based on history ±15% accuracy

◦ Feasibility – based on standard tables ±10% accuracy

◦ Definitive – once uncertainty is removed ±5% accuracy

When should each of these be used?

11

Cost estimating typically assumes a steady rate at which work is done

◦ Time activity 1 = Time activity 2 = Time activity n

Experience teaches us that repetition of activities often leads to a reduction of needed time to complete a future task

Research shows that performance improves by a constant fixed percentage each time production doubles

Ultimately, project budgets must be adjusted since learning curves are likely to occur

12

Each doubling of output results in a reduction in time to perform the last iteration.

Y x

aX b

Where :

Y = time required for the x unit of output x a = time required for the initial unit of output

X = the number of units to be produced b = learning curve slope = log(learning %)/log(2)

13

Your customers expect deflationary pricing

14

Example 1

◦ Assume you are a project cost engineer calculating the cost of a repetitive activity for your project.

◦ The initial output time for the first unit produced is 12 hours and the second unit is 10 hours.

◦ There are a total of 20 iterations of this activity required for the project.

◦ Determine learning rate and the steady state rate. learning rate

10

.

83333

12

Y

aX b x

Example 2

12

20

◦ Problem 7 page 270 log

10

12 log

12

20

.

07918

.

30103

12

.

45476

5 .

457

See learning curve example.xls

15

In spite of the best laid plans, various issues can affect accurate project estimates

Low initial estimates

Unexpected technical difficulties

Lack of project scope definition

Specification changes

External factors

16

WBS

Project

Plan

Scheduling Budgeting

Top-down

Bottom-up

Activity-based costing (ABC)

The budget, is a plan that identifies the resources, goals, and schedule that allows a firm to achieve those goals.

17

An approach that seeks to get top management input first to create an overall project cost

Cost allowances are passed down level-by-level, broken into allocated pieces for each task

Advantage: History shows that top management typically estimates pretty well and causes good budgetary discipline and cost control

Disadvantage: All successive levels need to fit their expenses within the allowable spend already chosen

Aggregate level of safety factor

18

Starts with the WBS to apply direct and indirect cost to specific project activities

Cost allowances are aggregated level-bylevel, until a total project budget is determined

Advantage: Emphasizes the need to create detailed project plans to be able to acquire necessary resources

Disadvantage: Reduces top management control to an oversight function

Safety factor at each detailed step

19

A budgeting method that assigns cost first to activities and then to the project based on each project’s use of the resources.

1.

Assign costs to activities that use resources

2.

Identify cost drivers associated with this activity

(i.e. material, labor)

3.

Compute a cost rate per cost driver unit or transaction (i.e. labor rate/hour)

4.

Multiply the cost driver rate times the volume of cost driver units used by the project (the more a resource is used, the more it drives cost)

20

Activity

Survey

Design

Clear Site

Foundation

Framing

Plumb & Wire

Cumulative

Direct Cost

3,500

7,000

3,500

6,750

8,000

3,750

Budget Overhead Total Cost

500

1,000

500

750

2,000

1,250

4,000

8,000

4,000

7,500

10,000

5,000

38,500

21

Months

Activity

Survey

Design

Clear Site

Foundation

Framing

Plumb & Wire

Monthly Planned

January February March April May Total by

Activity

4,000 4,000

5,000 3,000

4,000

8,000

4,000

4,000

7,500

8,000

1,000

2,000

4,000

9,000 10,500 9,000 6,000

7,500

10,000

5,000

45 000

40 000

35 000

30 000

25 000

20 000

15 000

10 000

5 000

0

Jan Feb Mar Apr May

Cumulative 4,000 13,000 23,500 32,500 38,500 38,500

22

Activity

Survey

Design

Clear Site

Foundation

Framing

Plumb & Wire

Total

Planned Actual Variance

4,000 4,250

8,000 8,000

4,000 3,500

7,500 8,500

10,000 11,250

5,000 5,150

38,500 40,650

250

0

(500)

1,000

1,250

150

2,150

23

The allocation of extra funds to cover uncertainties and improve the chance of finishing on time.

(safety factor)

Contingencies are needed because

Project scope may change

Murphy’s Law is always present

Cost estimation must anticipate task interaction costs

Normal conditions are rarely encountered

Access to these funds should serve as your first warning of project troubles. Cost control needs to be employed.

24

1.

Describe an environment in which it would be common to bid for contracts with low profit margins. What does this environment suggest about the competition levels?

2.

How has the global economy affected the importance of cost estimation and cost control for many project organizations?

3.

Why is cost estimation such an important component of project planning? Discuss how it links together with the Work Breakdown

Structure and project schedule?

4.

Imagine you were developing a software package for your company’s intranet. Give examples of the various types of costs

(labor, materials, equipment and facilities, subcontractors, etc.) and how they would apply to your project.

25

5.

Give reasons both in favor of and against the use of personal time charge as a cost estimate for a project activity.

6.

Think of an example of parametric estimating in your personal experience, such as the use of a cost multiplier based on a similar, past cost. Did parametric estimating work or not? Discuss the reasons why.

7.

Put yourself in the position of a project customer. Would you accept the cost adjustments associated with learning curve effects or not? Under what circumstances would learning curve costs be appropriately budgeted into a project?

8.

Consider the common problems with project cost estimation and recall a project with which you have been involved. Which of these common problems did you encounter most often? Why?

26

9.

Would you prefer the use of bottom-up or top-down budgeting for project cost control? What are the advantages and disadvantages with each approach?

10.

Why do project teams create time-phased budgets? What are their principle strengths?

11.

Project contingency can be applied to projects for a variety of reasons. List three of the key reasons why a project organization should consider the application of budget contingency.

27