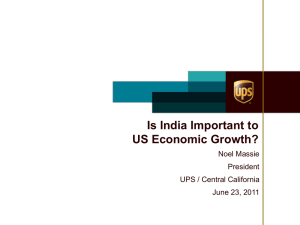

United Parcel Service (UPS)

advertisement

")

Recommendation: BUY United Parcel Service (UPS); Sell NG, JOYG, BHP Industry Overview Industry demand drivers: • E-commerce • Emerging economies • Trade 2 Company Profile UPS is the world's largest express carrier, specializing in time-definite package delivery and a growing presence in specialized transportation and logistics services. UPS delivers packages for more than 1.1 million shipping customers to 7.4 million consignees each day in over 220 countries and territories, using a network of 99,800 delivery vehicles, 527 planes, and 400,600 employees as of December 31, 2010. In 2010, UPS delivered 15.6 million pieces per day and recorded $49.5 billion in revenue. 3 Investment Information 4 UPS v. FDX In Search of Superior riskadjusted returns UPS Outguns FDX: 1. Lower volatility (beta) 2. Higher yield 3. Stronger profitability 5 UPS v. FDX UPS FDX Total Returns 24% 42% Standard Deviation 7.53 17.55 Risk-adjusted returns 3.20 2.37 Notes: • Returns since January 1, 2003 • Adjusted for dividends • Risk adjusted returns = (TotalReturns%*100)/standard deviation • Past performance does not guarantee future results 6 Chart: Buy the Dip 7 Chart: Oversold and Bottoming 8 Key Investment Points #1: Pricing power – domestic duopoly, international oligopoly #2: E-commerce tailwind for long-term growth #3: Return of capital to shareholders 9 Source: Company reports, BofA Merrill Lynch Global Research estimates. #1: Pricing Power As shown in Chart 3, margins are stalled halfway rebounding from its prior peak owing to the volume shortfall, despite the recent pickup in pure pricing (see Chart 1). Chart 3: Corporate EBIT margins still well off peak as volumes remain shy 15.0% 14.0% Room to go on corporate margins to return to peak 14.1% 14.0% 13.5% 12.7% 13.0% 11.6% 11.8% 12.0% 11.0% 10.0% 8.8% 1. DHL competition 2. Oil price spike 3. Recession / avg weight down 9.0% 8.0% 2006 2007 2008 2009 2010 2011e 2012e Source: Company reports, BofA Merrill Lynch Global Research estimates. 10 UPS noted that domestic operating margins in 3Q would begin to slow as it laps cost cutting and restructuring benefits from 2010. As average daily ground volumes remain 400,000 below peak levels (3.4% shy) at 11.2 million daily Ground packages per day, it has latent capacity which compresses its margin potential. #1: Pricing Power Chart 2: Ground volumes still below peak levels – leaves room for margin upside as volumes fill fixed cost network Still 400,000 shy of 2007 peak (3.4%) 11,800 11,622 11,600 11,546 11,522 11,463 11,400 11,199 11,150 11,200 10,914 11,000 10,800 10,600 10,400 2006 2007 2008 Source: Company reports, BofA Merrill Lynch Global Research estimates. 2009 2010 2011e 2012e 11 #1: Pricing Power 4 competitors: UPS, FDX, DHL, USPS • DHL: Low cost provider exited domestic express land/air market in 2009 • DHL continues to offer international and heavy weight shipping • USPS considering more limited services • UPS and FDX now have greater pricing power 12 #1: Pricing Power 13 #2: E-commerce: US 14 #2: E-commerce: US 15 #2: E-commerce: China 16 #3: Return of Capital Diluted Shares Outstanding 1,200,000 1,150,000 1,100,000 1,050,000 1,000,000 950,000 900,000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 Reduced share count by >2% per year since 2005 TTM 2011E 17 #3: Return of Capital Dividend $2.50 $2.00 $1.50 $1.00 $0.50 $2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Dividend CAGR 10% for the last decade 18 SWOT Analysis Strengths Strong competitive position – duopoly International growth, esp. Asia Scale / profitability Strong cash flow, financial flexibility Opportunities USPS cutbacks Price increases Increase buy backs, dividends New distribution partnerships Weaknesses Capital intense Unionized labor force (agreement runs through July 2013) Threats Labor strike Oil prices Recession Price war with FedEx, USPS Mkt decline / pension funding 19 Valuation Dividend Discount Model Beta Rf MRP Required Return 5-yr Dividend Growth Rate Dividend Fair Value DCF Model 0.89 2.33% 8% 9.5% 7.30% 2.08 $96.74 P/E Price Target 2012E EPS $5.16 1-yr average forward P/E 17.0x Price Target $87.72 Terminal growth rate 2.50% Terminal FCF $3,986 /(r-g) Discount factor $83,562 $1.45 PV TV $57,480 + PV of FCF $12,867 = Enterprise Value $70,347 less debt $12,170 add cash $5,640 = Equity Value / Shares Fair Value $63,817 981 $65.07 Note: UPS' FCF potential is likely understated as margins have fallen. 20 UPS - Fwd P/E Average 8/26/11 8/12/11 7/29/11 7/15/11 7/1/11 6/17/11 6/3/11 5/20/11 5/6/11 4/22/11 4/8/11 3/25/11 3/11/11 2/25/11 2/11/11 1/28/11 1/14/11 12/31/10 12/17/10 12/3/10 11/19/10 11/5/10 10/22/10 10/8/10 9/24/10 9/10/10 8/27/10 Valuation UPS Forward P/E 20.00 19.00 18.00 17.00 16.00 15.00 14.00 13.00 12.00 21 Valuation: Which Method? • Given the company’s record of consistent dividend increases, DDM appears most appropriate • However, each valuation method in sensitive to the assumptions used to derive the inputs • An average of the methods yields a more conservative 12-month price target. Valuation Summary Dividend Discount Model P/E Price Target DCF Model Average Current Price Upside $96.74 $87.72 $65.07 $83.18 $64.70 29% 22 Portfolio Recommendation BUY 150 shares of UPS at a limit price of $64 ($9,600, 2.1% of portfolio) Sell 100 JOYG @ Market (~$83.45, $8,345) Sell 125 BHP @ Market (~$85.17, $10,646) Sell 400 NG @ Market (~$10.30, $4,121) 23 Portfolio Recommendation Industrials Target Sector Allocation: 7.3%, Current Sector Allocation: 3.3% Allocation after sale: 1.6% Allocation after purchase: 3.7% 24 Portfolio Recommendation Materials Target Sector Allocation: 2.4%, Current Sector Allocation: 5.4% Allocation after sales: 2.2% 25 Sell Rationale Materials BHP: Levered to China, fairly valued in an uncertain market = sell JOYG: Similar to BHP. Repurchase if the stock falls to $55 or below. Expect the stock to fall no further than the upper $40s. I would highly recommend a repurchase. NG: Will need to raise funds by issuing stock. We can repurchase after the secondary if we so desire. 26

![6. Unit 13 Command and Control Chains of[...]](http://s2.studylib.net/store/data/005232084_1-44f6fe20f659f6d5a7ee6394b58542c9-300x300.png)