Module2.3

advertisement

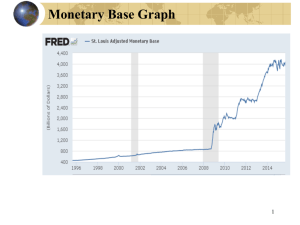

Mortgage Backed Security (MBS) An MBS is a security whose cash flows are derived from a pool of mortgages. Two types of MBSs: mortgage bonds (created from a pool of mortgages) CDOs (created from a pool of mortgage bonds) MBSs can get extremely complicated. ABS (asset backed security) is same as MBS but cash flows are from a pool of home equity loans, auto loans, student loans, credit card receivables, . . . Now over $1.2 trillion in student loans (but not all have been securitized, i.e., made into ABSs). 1 Monetary Base Graph 2 M1 Graph 3 Money Supply Comments • Money supply is believed to be important. • While Fed is in entire control of the monetary base, M1 and M2 are considered more useful in controlling the real sector. • Note that most of the money supply aggregates that comprise M1 and M2 are determined by private decisions which the Fed can’t precisely control (but can influence via the monetary base). • Thus, the Fed, via the monetary base, can only imprecisely control M1 and M2. 4 Hedge Funds Hedge -- an investment intended to offset adverse price movements in another investment. A basic hedging strategy is pair trading. Involves matching a long position with a short position. Funds use math and statistics to identify pairs with good spread reversion characteristics. Done with stocks, options, commodities, currencies, etc. By law, hedge funds only offered to institutional investors or individuals of substantial wealth. Government then doesn’t regulate much. 5 Actual Fed Funds Rates 1954-2008 6 Fed Funds Rates 2004-2008 7 Target Rate vs. Actual Sep07 to Sep08 8 Monetarist Economists • Monetarists believe – key explanatory variable is the money supply – people will buy more if feel they have “more money,” and spend less if feel they have “less money.” – idea is to use monetary policy to influence the money supply. – in this way, adding reserves should promote economic growth, reducing reserves should slow the economy. 9 Keynesian Economists • Keynesians believe – key explanatory variable is the interest rate – John Maynard Keynes was influential British economist of 1930s. – money supply does not make that much difference – believe economic growth is stimulated by falling interest rates, and slowed by rising rates 10 Dates stocks bonds 03/17/08 Bear Stearns (taken over by JP Morgan Chase and government guarantees) 09/07/08 Fannie Mae / Freddie Mac (conservatorship) 09/15/08 Lehman Brothers (bankruptcy) 09/16/08 AIG (kept alive by US government and Federal Reserve) 09/21/08 Goldman Sachs & Morgan Stanley become bank holding companies 09/25/08 Washington Mutual (receivership by FDIC and then bankruptcy, formerly 6th largest US bank) 12/31/08 Wachovia (taken over by Wells Fargo, formerly 4th largest US bank) 01/01/09 Merrill Lynch (saved from failure by being purchased by Bank of America) -90% -98% safe safe -100% part loss -95% safe -100% part loss -90% safe -60% safe 11 Fed Balance Sheet (millions), April 2009 Assets Liabilities & Capital Gold & Coin 15,107 Federal Reserve Notes Loans to depository institutions - Rev Repurchase agreements Repurchase agreements 0 Deposits US treasury securities Agency securities 534,969 64,511 862,960 64,681 Depository inst balances 915,773 US Treasury 295,399 MBS 367,590 Other 13,456 Term Auction Facility (TAF) 455,799 Capital 46,000 CP Facility 242,431 Maiden Lane & related 72,163 Other loans 102,988 Foreign currency 282,863 Other 2,198,269 59,849 2,198,269 9/26 12 Term Auction Facility As subprime problem arose in late 2007, banks began to encounter liquidity problems. Overwhelmed discount window. In Dec 2007, Fed suspended traditional discount window operations in favor of Term Auction Facility (TAF): • rather than just overnight, made 28 and 84-day loans • accepted other securities, rather than just Treasuries and agency securities, as collateral. • originally for depository institutions, extended to nonbank financial institutions. • no new loans after March 2010 13 Commercial Paper • Unsecured promissory notes that mature before nine months (270 days). • Proceeds can only be used for operating purposes (inventories, receivables) and not for fixed assets (land, buildings, machinery). • Issued by 600 to 800 corporations. • Sold at discount, mature at par. • Some sold by direct placement, but most sold through dealers . • Dealers charge something like one-tenth to one-eighth of a percent of face value to underwrite an issue for a firm. 14 CP Backup Lines of Credit • Except for a few highly-rated firms, usually not possible for an issuer to sell CP without a backup line of credit. • Backup line of credit is agreement by which a bank will lend an issuer, if needed, the money necessary to redeem maturing paper. • Makes purchasers feel more secure in the event issuer is not able to “roll over” maturing CP (i.e., sell new CP to pay off old CP). • Banks charge 10 to 12.5 basis points (on an annual basis) of par amount for backup lines of credit, then market interest rate if money is actually borrowed. • Average CP maturity is about 30 days • In financial crisis, were difficult to roll over 15 CP • Rated: prime, desirable, satisfactory. P-1, P-2, P-3 (Moody’s) A-1, A-2, A-3 (S&P’s) • Virtually impossible to sell unrated commercial paper • Advantage of CP: low interest rates • About 30 commercial paper dealers. • There is a secondary market and issuers sometimes buy back their commercial paper. Transaction costs in range of about one-eighth of one percent per annum. • Normal US CP: up to $1 trillion outstanding at any moment. 16 Asset-Backed Commercial Paper • In addition to normal commercial paper, there is asset-backed commercial paper (ABCP). • Typical maturities of ABCP a little longer: 90 to 180 days • In run up to financial crisis, issued by up to 1,000 special purpose vehicles to help buy pools of mortgages, car loans, student loans, credit card receivables, etc., but mostly mortgages. • Before financial crisis struck, up to $1 trillion of US ABCP outstanding. • Then couldn’t roll over, so Fed had to step in. 17 Fed Balance Sheet, September 25, 2014 Assets Gold & Coin Loans to depository institutions Repurchase agreements US Treasury securities Agency securities MBS Liabilities & Capital 11,041 330 0 2,447,066 40,006 1,708,147 Term Auction Facility (TAF) - CP Facility - Maiden Lane & related Other loans Foreign currency Other Federal Reserve Notes Rev Repurchase agreements 1,288,293 270,542 Deposits Depository inst balances US Treasury 2,732,580 114,828 Other 32,766 Capital 63,656 4,502,665 1,664 22,560 271,851 4,502,665 18 Open Market Injection of $30 Billion k = 10% 10/3 19 Technical Factors Cash drains – increased cash holdings by public decrease banking system reserves. Example: People take money out of their checking accounts in advance of a big weekend. Reduces vault cash Banks have harder time meeting RRs Puts upward pressure on Fed Funds rate Fed does Repurchase Agreement to increase temporarily depository institution reserves Puts downward pressure on Fed Funds rate US Treasury transactions -- many such transactions cause shifts in reserves. Fed often offsets with carefully calibrated open market transactions (typically with repos and reverse repos) 20 Velocity of Money • Velocity is annual money supply turnover rate. • Velocity * Money supply = GDP • Velocity is difficult to predict. • For given change in money supply, the Fed can expect direction of change in economy, but cannot ensure the degree. 21