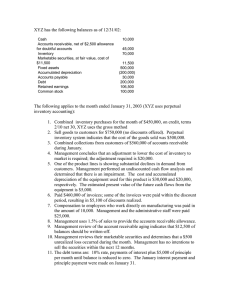

UOG- Intermediate Accounting I NAME: STUDENT ID: IMPORTANT: 1. 2. 3. 1. A. B. C. D. The exam consists of 40 multiple choice questions. Make sure that you have a complete exam. To receive credit for your answers on the problems you must show and clearly label all of your computations. Your grade will be influenced by the orderliness and clarity of your answers. When you finish the exam, please turn it in to the teacher. Which of the following statements is/are incorrect? Uniform accounting standards make financial statements comparable across firms. Uniform accounting standards satisfy all different needs of accounting information users. Uniform accounting standards save transaction and search costs. Uniform accounting standards benefits all preparers (i.e., companies rely on external financing) 2. A. B. C. D. Which of the following entities enforce the compliance of accounting standards? Financial Accounting Standards Board (FASB) Securities and Exchange Commission (SEC) American Institute of Certified Public Accountants (AICPA) International Accounting Standards Board (IASB) 3. A. B. C. D. Which groups are the primary users FASB has in mind? Regulators, such as SEC and IRS. Existing investors and creditors. Potential investors and creditors. Suppliers and customers. 4. A. C. D. Which of the following statements is/are correct? Predictive value means accounting information coupled with other sources of information is used by investors to forecast future events. Predictive value means how precise accounting information can predict a future outcome. Historical accounting information has predictive value. Historical accounting information has no predictive value. 5. A. B. When is revenue generally recognized? When cash is received. When the warranty expires. B. UOG- Intermediate Accounting I C. D. When production is completed. When the company satisfies the performance obligation. 6. A. B. C. D. Which of the following is a real (permanent) account? Goodwill Service Revenue Accounts Receivable Cost of goods sold 7. The income statement of Dolan Corporation for 2014 included the following items: Interest revenue $121,000 Salaries and wages expense 180,000 Insurance expense 18,200 The following balances have been excerpted from Dolan Corporation's balance sheets: December 31, 2014 December 31, 2013 Interest receivable $18,200 $15,000 Salaries and wages payable 17,800 8,400 Prepaid insurance 2,200 3,000 The cash received for interest during 2014 was A. $102,800. B. $117,800. C. $121,000. D. $124,200. 8. Olsen Company paid or collected during 2014 the following items: Insurance premiums paid $25,800 Interest collected 62,800 Salaries paid 260,400 The following balances have been excerpted from Olsen's balance sheets: December 31, 2014 December 31, 2013 Prepaid insurance $ 2,400 $ 3,000 Interest receivable 7,400 5,800 Salaries and wages payable 24,600 21,200 The insurance expense on the income statement for 2014 was A. $20,400. B. $25,200. C. $26,400. D. $31,200. UOG- Intermediate Accounting I 9. Chen Company's account balances at December 31, 2014 for Accounts Receivable and the Allowance for Doubtful Accounts are $480,000 debit and $900 credit. Sales during 2014 were $1,650,000. It is estimated that 1% of sales will be uncollectible. The adjusting entry would include a credit to the allowance account for A. $17,400. B. $16,500. C. $15,600. D. $4,800. 10. Lopez Company received $14,400 on April 1, 2014 for one year's rent in advance and recorded the transaction with a credit to a nominal account. The December 31, 2014 adjusting entry is A. debit Rent Revenue and credit Unearned Rent Revenue, $3,600. B. debit Rent Revenue and credit Unearned Rent Revenue, $10,800. C. debit Unearned Rent Revenue and credit Rent Revenue, $3,600. D. debit Unearned Rent Revenue and credit Rent Revenue, $10,800. 11. A material item which is unusual in nature or infrequent in occurrence, but not both should be shown in the income statement Net of Tax Disclosed Separately A. No No B. Yes Yes C. No Yes D. Yes No Which of the following is an example of managing earnings down? A. Changing estimated bad debts from 3 percent to 2.5 percent of sales. B. Revising the estimated life of equipment from 10 years to 8 years. C. Not writing off obsolete inventory. D. Reducing research and development expenditures. 12. At Ruth Company, events and transactions during 2014 included the following. The tax rate for all items is 30%. (1) Depreciation for 2012 was found to be understated by $90,000. (2) A strike by the employees of a supplier resulted in a loss of $75,000. (3) The inventory at December 31, 2012 was overstated by $120,000. (4) A flood destroyed a building that had a book value of $1,500,000. Floods are very uncommon in that area. The effect of these events and transactions on 2014 income from continuing operations net of tax would be A. ($52,500 B. ($115,500). UOG- Intermediate Accounting I C. ($199,500). 13. Which of the following assets is not recognized on balance sheet according to the current U.S. GAAP? A. A building used for drug research and development labs B. A building used to demonstrate patent drugs C. A building used to train sales representatives D. A building used for customer services 14. A generally accepted method of valuation is 1. trading securities at market value. 2. accounts receivable at net realizable value. 3. inventories at current cost. A. 1 B. 2 C. 3 D. 1 and 2 15. A. B. C. D. Making and collecting loans and disposing of property, plant, and equipment are operating activities. investing activities. financing activities. liquidity activities. 16. A. B. C. D. Which of the following is an example of managing earnings down? Changing estimated bad debts from 3 percent to 2.5 percent of sales. Revising the estimated life of equipment from 10 years to 8 years. Not writing off obsolete inventory. Reducing research and development expenditures. 17. Marle Construction enters into a contract with a customer to build a warehouse for $850,000 on March 30, 2014 with a performance bonus of $50,000 if the building is completed by July 31, 2014. The bonus is reduced by $10,000 each week that completion is delayed. Marle commonly includes these completion bonuses in its contracts and, based on prior experience, estimates the following completion outcomes: Completed by Probability July 31, 2014 65% August 7, 2014 25% August 14, 2014 5% August 21, 2014 5% The transaction price for this transaction is: A. $895,000 B. $850,000 C. $552,500 D. $585,000 UOG- Intermediate Accounting I 18. P & G Auto Parts sells parts to AAA Car Repair during 2014. P&G offers rebates of 2% on purchases up to $30,000 and 3% on purchases above $30,000 if the customer’s purchases for the year exceed $100,000. In the past, AAA normally purchases $150,000 in parts during a calendar year. On March 25, 2014, AAA Car Repair purchased $37,000 of parts. The journal entry to record the purchase includes a: A. debit to Accounts Receivable for $37,000. B. debit to Accounts Receivable for $36,400. C. credit to Sales Revenue for $36,190. D. credit to Sales Revenue for $36,400. 19. On August 5, 2014, Famous Furniture shipped 20 dining sets on consignment to Furniture Outlet, Inc. The cost of each dining set was $350 each. The cost of shipping the dining sets amounted to $1,800 and was paid for by Famous Furniture. On December 30, 2014, the consignee reported the sale of 15 dining sets at $850 each. The consignee remitted payment for the amount due after deducting a 6% commission, advertising expense of $300, and installation and setup costs of $390. The total profit on units sold for the consignor is: A. $11,295 B. $4,695 C. $6,045 D. $9,945 20. Botanic Choice sells natural supplements to customers with an unconditional right of return if they are not satisfied. The right of returns extends 60 days. On February 10, 2014, a customer purchases $3,000 of products (cost $1,500). Assuming that based on prior experience, estimated returns are 20%. The journal entry to record the return of $200 of merchandise includes a: A. credit to Refund Liability for $200. B. credit to Returned Inventory for $100. C. credit to Estimated Inventory Returns for $100. D. debit to Estimated Inventory Returns for $100. 21. On the December 31, 2014 balance sheet of Vanoy Co., the current receivables consisted of the following: Trade accounts receivable $ 60,000 Allowance for uncollectible accounts (2,000) Claim against shipper for goods lost in transit (November 2014) 3,000 Selling price of unsold goods sent by Vanoy on consignment at 130% of cost 26,000 UOG- Intermediate Accounting I Security deposit on lease of warehouse used for storing some inventories 30,000 Total $117,000 At December 31, 2014, the correct total of Vanoy's current net receivables was: A. $61,000. B. $87,000. C. $91,000. D. $117,000. 22. Sun Inc. factors $3,000,000 of its accounts receivables with recourse for a finance charge of 3%. The finance company requires Sun to retain an amount equal to 10% of the accounts receivable for possible adjustments. Sun estimates the fair value of the recourse liability at $150,000. What would Sun record as a gain (loss) on the transfer of receivables? A. Gain of $90,000. B. Loss of 240,000. C. Gain of $540,000. D. Loss of $150,000. 23. Geary Co. assigned $800,000 of accounts receivable to Kwik Finance Co. as collateral for a loan of $670,000. Kwik charged a 2% commission on the amount of the loan; the interest rate on the note was 10%. During the first month, Geary collected $220,000 on assigned accounts after deducting $760 of discounts. Geary accepted returns worth $2,700 and wrote off assigned accounts totaling $5,960. The amount of cash Geary received from Kwik at the time of this assignment was: A. $603,000. B. $654,000. C. $656,600. D. $670,000. 24. Elmer Corporation has $1,800,000 of short-term debt it expects to retire with proceeds from the sale of 50,000 shares of common stock. If the stock is sold for $20 per share subsequent to the balance sheet date, but before the balance sheet is issued, what amount of short-term debt could be excluded from current liabilities? A. $1,000,000 B. $1,800,000 C. $800,000 D. $0 25. A company gives each of its 50 employees (assume they were all employed continuously through 2014 and 2015) 12 days of vacation a year if they are employed UOG- Intermediate Accounting I at the end of the year. The vacation accumulates and may be taken starting January 1 of the next year. The employees work 8 hours per day. In 2014, they made $21 per hour and in 2015 they made $24 per hour. During 2015, they took an average of 9 days of vacation each. The company’s policy is to record the liability existing at the end of each year at the wage rate for that year. What amount of vacation liability would be reflected on the 2014 and 2015 balance sheets, respectively? A. $100,800; $140,400 B. $115,200; $144,000 C. $100,800; $144,000 D. $115,200; $140,400 26. A company buys an oil rig for $2,000,000 on January 1, 2014. The life of the rig is 10 years and the expected cost to dismantle the rig at the end of 10 years is $400,000 (present value at 10% is $154,220). 10% is an appropriate interest rate for this company. What expense should be recorded for 2014 as a result of these events? A. Depreciation expense of $240,000 B. Depreciation expense of $200,000 and interest expense of $15,422 C. Depreciation expense of $200,000 and interest expense of $40,000 D. Depreciation expense of $215,422 and interest expense of $15,422 27. Black Corporation uses the FIFO method for internal reporting purposes and LIFO for external reporting purposes. The balance in the LIFO Reserve account at the end of 2014 was $140,000. The balance in the same account at the end of 2015 is $210,000. Black’s Cost of Goods Sold account has a balance of $1,050,000 from sales transactions recorded internally during the year. What amount should Black report as Cost of Goods Sold in the 2015 external income statement? A. $ 980,000. B. $1,050,000. C. $1,120,000. D. $1,260,000. 28. Milford Company had 400 units of “Tank” in its inventory at a cost of $6 each. It purchased 600 more units of “Tank” at a cost of $9 each. Milford then sold 700 units at a selling price of $15 each. The LIFO liquidation overstated normal gross profit by A. $ -0B. $300. C. $600. D. $900. UOG- Intermediate Accounting I 29. RF Company had January 1 inventory of $200,000 when it adopted dollar-value LIFO. During the year, purchases were $1,200,000 and sales were $2,000,000. December 31 inventory at year-end prices was $286,720, and the price index was 1.12. What is RF Company’s ending inventory? A. $200,000. B. $256,000. C. $262,720. D. $286,720. 30. Ryan Distribution Co. has determined its December 31, 2014 inventory on a FIFO basis at $490,000. Information pertaining to that inventory follows: Estimated selling price $510,000 Estimated cost of disposal 20,000 Normal profit margin 60,000 Current replacement cost 450,000 Ryan records losses that result from applying the lower-of-cost-or-market rule. At December 31, 2014, the loss that Ryan should recognize is A. $0. B. $10,000. C. $20,000. D. $40,000. Use the following information for questions 1 and 2. 31. Eaton Company uses the retail LIFO method to determine inventory cost and has provided the following information for 2014 (please round the cost-to-retail ratio to XX.XX% or 0.XXXX): Cost Retail Inventory, 1/1/14 $ 188,000 $280,000 Net purchases 756,000 1,124,000 Net markups 136,000 Net markdowns 60,000 Net sales 1,060,000 Assuming stable prices (no change in the price index during 2014), what is the cost of Eaton's inventory at December 31, 2014? A. $347,983. B. $310,183. C. $272,383. D. $224,503. 32. Assuming that the price index was 105 at December 31, 2014 and 100 at January 1, 2014, what is the cost of Eaton's inventory at December 31, 2014 under the dollar-value-LIFO retail method? A. $267,372. UOG- Intermediate Accounting I B. $279,691. C. $286,002. D. $263,592. 33. During 2014, Bass Corporation constructed assets costing $3,000,000. The weighted-average accumulated expenditures on these assets during 2014 was $1,800,000. To help pay for construction, $1,320,000 was borrowed at 10% on January 1, 2014, and funds not needed for construction were temporarily invested in short-term securities, yielding $27,000 in interest revenue. Other than the construction funds borrowed, the only other debt outstanding during the year was a $1,500,000, 10-year, 9% note payable dated January 1, 2008. What is the amount of interest that should be capitalized by Bass during 2014? A. $180,000. B. $90,000. C. $175,200. D. $283,200. 34. Dodson Company traded in a manual pressing machine for an automated pressing machine and gave $24,000 cash. The old machine cost $279,000 and had a net book value of $213,000. The old machine had a fair value of $180,000. This exchange lacks commercial substance for Dodson. Which of the following is the correct journal entry to record the exchange? a. Equipment (new) 204,000 Loss on Disposal 33,000 Accumulated Depreciation 66,000 Equipment 279,000 Cash 24,000 b. Equipment (new) 204,000 Equipment 120,000 Cash 24,000 c. Cash 24,000 Equipment (new) 180,000 Loss on Disposal 33,000 Accumulated Depreciation 66,000 Equipment 303,000 d. Equipment (new) 369,000 Accumulated Depreciation 66,000 Equipment 279,000 Cash 24,000 Answer: A 35. Hardin Company received $80,000 in cash and a used computer with a fair value of UOG- Intermediate Accounting I $240,000 from Page Corporation for Hardin Company's existing computer having a fair value of $320,000 and a net book value of $300,000. The transaction has no commercial substance. How much gain should Hardin recognize on this exchange, and at what amount should the acquired computer be recorded, respectively? A. $0 and $220,000 B. $5,000 and $225,000 C. $20,000 and $240,000 D. $80,000 and $300,000 36. Norton, Inc. purchased equipment in 2013 at a cost of $800,000. Two years later it became apparent to Norton, Inc. that this equipment had suffered an impairment of value. In early 2015, the book value of the asset is $520,000 and it is estimated that the fair value is now only $320,000. The entry to record the impairment is A. B. C. D. No entry is necessary as a write-off violates the historical cost principle. Retained Earnings .................................................................. 200,000 Accumulated Depreciation—Equipment ......................... 200,000 Loss on Impairment of Equipment ........................................ 200,000 Accumulated Depreciation—Equipment ......................... 200,000 Retained Earnings .................................................................. 200,000 Reserve for Loss on Impairment of Equipment ............... 200,000 37. Barton Corporation acquires a coal mine at a cost of $1,500,000. Intangible development costs total $360,000. After extraction has occurred, Barton must restore the property (estimated fair value of the obligation is $180,000), after which it can be sold for $510,000. Barton estimates that 5,000 tons of coal can be extracted. If 900 tons are extracted the first year, which of the following would be included in the journal entry to record depletion? A. Debit to Accumulated Depletion for $275,400 B. Debit to Inventory for $275,400 C. Credit to Inventory for $270,000 D. Credit to Accumulated Depletion for $459,000 38. Blue Sky Company’s 12/31/15 balance sheet reports assets of $6,000,000 and liabilities of $2,400,000. All of Blue Sky’s assets’ book values approximate their fair value, except for land, which has a fair value that is $360,000 greater than its book value. On 12/31/15, Horace Wimp Corporation paid $6,120,000 to acquire Blue Sky. What amount of goodwill should Horace Wimp record as a result of this purchase? A. $ -0B. $120,000 UOG- Intermediate Accounting I C. $2,160,000 D. $2,520,000 39. General Products Company bought Special Products Division in 2014 and appropriately recorded $750,000 of goodwill related to the purchase. On December 31, 2015, the fair value of Special Products Division is $6,000,000 and it is carried on General Product’s books for a total of $5,100,000, including the goodwill. An analysis of Special Products Division’s assets indicates that goodwill of $600,000 exists on December 31, 2015. What goodwill impairment should be recognized by General Products in 2015? A. $0. B. $300,000. C. $150,000. D. $450,000. 40. Riley Co. incurred the following costs during 2015: Significant modification to the formulation of a chemical product $160,000 Trouble-shooting in connection with breakdowns during commercial production 150,000 Cost of exploration of new formulas 200,000 Seasonal or other periodic design changes to existing products 185,000 Laboratory research aimed at discovery of new technology 325,000 In its income statement for the year ended December 31, 2015, Riley should report research and development expense of A. $685,000. B. $835,000. C. $870,000. D. $1,020,000.