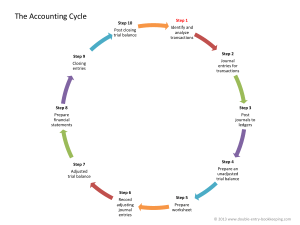

A good accounting system must be able to handle transactions in order, even if they are happening at a rapid pace. The chronological journal is a centuries-old device that keeps track of business transactions Is a book in which the accounting entries for all transactions are first recorded, before they are recorded in the ledger accounts. Transactions are recorded in the order of their occurrence. The simplest form is the two-column general journal (see Figure 6.1) A journal entry is made up of all of the accounting changes for one transaction, in the form in which they are written in the general journal The debited account and amount are recorded first. The credited account and amount are recorded second and are indented. Debits = Credits Each journal entry ends with a brief explanation 1. The year: Enter the year in small figures on the first line of each page. Not repeated for each entry. Enter a new year at the point on the page where it occurs 2. The month: Same rules as year 3. The day: Enter the day on the first line of each journal entry. Day is always written. 1. 2. 3. 4. The date Debit account(s) Credit account(s) Explanation Chief purpose is to provide a continuous record of the accounting entries Accounting entries come from source documents The entry clerk should see that each entry balances and generally that everything is in order If entered properly it reduces errors and prevents problems from occurring later Useful for reference of transactions Every accounting entry is recorded first in the journal The financial position provided by a balance sheet would be your opening entry The journal entry that starts the books off, or “opens” them, is known as the opening entry