1.1 In February 2012 the Council approved the budget for 2012/13... time it considered the forward financial projections for the following...

advertisement

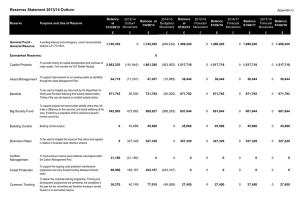

FINANCIAL STRATEGY 2013/14 – 2015/16 1. INTRODUCTION 1.1 In February 2012 the Council approved the budget for 2012/13 and at the same time it considered the forward financial projections for the following three years (2013/14 to 2015/16). The budget for 2012/13 includes savings and additional income totalling over £1.2 million (consisting of service savings/income of £897,096 and corporate savings of £375,446). After factoring these in for future years and making assumptions around inflation, income and grant funding levels, the forecast budget gap for the following three years was projected to be £267,000 in 2013/14 increasing to £1.072million in 2014/15 and to £1.232million by 2015/16. 1.2 This document now seeks to update these financial projections and sets out the financial strategy for the next three years in line with the current Corporate Plan 2012-15, which covers the same period. 1.3 Reductions in grant funding for local government were announced back in October 2010 as part of the Comprehensive Spending Review 2010 (CSR 2010). This covered the period 2011/12 to 2014/15 and essentially set out the Governments departmental spending plans for the four years until 2014/15. The current financial year of 2012/13 is the second year of the current spending review period and the final year for which provisional figures have been published for individual authorities. The timing of the next spending review has not been confirmed, although it is expected to be sometime during 2013 and is likely to cover the final year of the current spending review, i.e. 2014/15. 1.4 From 2013/14 local authorities are facing a significant change to their system of financing. This is discussed in more detail within section 2, but essentially there is a fundamental shift from a formula grant system to one financed by locally retained business rate income plus grant. 2. BACKGROUND AND CONTEXT 2.1 There are a number of current issues facing the public sector in terms of financing. Each of the following are discussed in more detail: • • • • • • • Economic Outlook Local Government Finance Bill Business Rates Retention New Homes Bonus Council Tax Support Scheme Council Tax Reforms Welfare Reform Bill 2.2 Economic Outlook 2.2.1 Economic output in the UK had weakened for three consecutive quarters with a contraction of 0.5% in the second quarter of 2012. The third quarter however, showed the economy coming out of recession and growing by an estimated 1.0%. This was much stronger than forecast and was affected by the Olympic and Paralympic Games, and the additional holiday for the Queen’s Diamond Jubilee in the second quarter. The outlook for growth in the near term does remain weak though, particularly whilst uncertainty in the Euro zone countries persists. 2.2.2 A gradual strengthening in the growth of households’ incomes, together with the combined stimulus from the Bank of England’s asset purchase programme (Quantitative Easing) and the Funding for Lending Scheme (which provides Financial Strategy 2013/14 to 2015/16 October 2012 Page 1 of 26 incentives to banks and building societies to lend more to UK households and businesses),should prompt a gradual pickup in economic activity. 2.2.3 Despite the poor growth resulting in much weaker public finances than had been forecast, the Government is expected to stick to its deficit-cutting strategy. 2.2.4 The financial markets are anticipating a further 0.25% cut in official interest rates by the end of this year. It could be 2016 before interest rates begin to rise again. 2.2.5 Consumer Price Inflation decreased to 2.2% year-on-year to September 2012, from 2.5% a month earlier. 2.3 Local Government Finance Bill 2.3.1 The Local Government Finance Bill (the bill) was introduced by the Secretary of State in December 2011. The Bill included a number of proposals designed to encourage local economic growth, reduce the financial deficit and drive the decentralisation of control over local government finance. 2.3.2 This bill represents a major change to the way that local government will be financed from 2013/14 onwards. In particular the Bill includes the following changes: • Business Rate Retention (para 2.4) - Enabling local authorities to retain a proportion of the business rates generated in their area, providing them with strong financial incentive for them to promote local economic growth; • Localised Council Tax Support Scheme (para 2.6) - Providing a framework for the localisation of council tax support to replace the current council tax benefit system, which alongside other council tax measures, will give councils increased financial autonomy and a greater stake in the economic future of their local area, while providing continuation of council tax support for the most vulnerable in society, including pensioners. The savings nationally from the localisation of council tax support is expected to be £500m; • Council Tax Reforms (para 2.7) –Provide further flexibility on the council tax local authorities can charge on empty properties, and other small changes aimed at modernising the system. 2.3.3 Each of these are discussed in the following sections of the document. 2.4 Business Rates Retention 2.4.1 In December 2011 the Government published its proposals for the introduction of a business rates retention scheme (BRRS). Their response to this was subsequently published in May 2012 and a technical consultation was then launched in July which closed in September 2012. The timing of the final scheme announcement has not yet been confirmed. 2.4.2 The overriding principal of the BRRS is to incentivise growth at a local level and implement a funding regime that replaces the current complex and centralised formula grant system with a simple and transparent system that is related to growth at a local level. The incentive to local authorities is that a share of any growth in business rate income is retained locally. 2.4.3 From April 2013, a portion of local authorities’ income will change with business rates growth, rather than being determined by complex formulae. Moving from the current complicated arrangements inevitably means there is a degree of complexity to the transitional arrangements which will apply on introduction of the new scheme. Once the new scheme is established, authorities will know what proportion of business rates they can keep, how much they are to pay as a “tariff” Financial Strategy 2013/14 to 2015/16 October 2012 Page 2 of 26 or receive as a “top-up”, the rate at which their growth will be levied and the floor below which the safety net will prevent their income from falling. These parameters will be fixed until 2020. 2.4.4 Due to the significant changes, the transition from the current system to the new system from 2013/14 will involve a degree of complexity, yet in the longer term the new system is expected to have less complexity. 2.4.5 Under the current formula grant system the Council receives (government) funding from a Revenue Support Grant (RSG) and an allocation of redistributed business rate (i.e. total business rates collected are paid over to government centrally and then reallocated to individual authorities). Under the new system funding to the Council will comprise of a local retained business rate income and a RSG. 2.4.6 The main elements of the new scheme are: a) The starting point for the new scheme from 2013/14 (baseline funding) will be based on how much authorities would receive under the existing scheme, subject to updating and changing many of the details of the existing formula and the initial amount available to be shared between authorities being reduced in line with current Government plans, i.e. those outlined in the 2010 spending review. b) The proposals for the new scheme focus on the distribution of business rates revenues, rather than changes to the system of business rates taxation. Businesses (ie non domestic rate payers) will see no change to the way their rates are paid or set and increases in the rates will remain under the control of central government. The revaluation process will be unchanged. c) Business rates collected will be split 50/50 between central and local shares. d) Central share will be used to fund the RSG element for the new scheme. e) Local shares will be split 80/20 between the district and the county councils (for two tier authorities). f) Local shares will be subject to tariffs and top-ups to reflect the local spending needs. Authorities with a high business rates base compared to their funding level would pay a tariff (Districts), and those with a higher spending need compared to retained business rates will receive a top-up payment (Counties). g) A reset period is proposed after seven years (2020), at which time new baseline funding, base rate baselines (and therefore tariffs and top ups) are set. h) The Business rates baseline (i.e. income generated) will be calculated from the national aggregated level forecast for 2013/14 and then apportioned to each authority. i) The difference between funding and baseline determines a tariff or top up position. 2.4.7 Appendix A provides an overview of the system graphically. 2.4.8 The main elements of the scheme in relation to business rate growth are: a) Local Authorities will be able to retain a proportion of business rate growth or conversely if there is decline Local Authorities will see a reduction in their income. Financial Strategy 2013/14 to 2015/16 October 2012 Page 3 of 26 b) Authority’s that experience disproportionate growth will be required to pay a levy and this will be used to provide a safety net for authorities experiencing little or negative growth. The calculation of levy and safety net payments (as outlined within the consultation document) indicates that the safety net will fall within the 7.5%-10% range and funded by a 1:1 levy as already announced. Essentially a Local Authority could have a reduction in income of up to 10% before safety net funding would be applied. c) The levy will limit disproportionate benefit from growth in an authority’s business rates base. For every 1% increase in business rates baseline, an authority will only see a 1% increase in its funding level. d) The following provides an illustrative example of how the levy payment might work for NNDC: Table 1 £000 Business Rates Baseline A 22,000 1% Growth B = 1% of A 220 Local Share (50%) C = 50% of B 110 District Share (80% of the 50%) D = 80% of C 88 Levy payment * E = 67% of D 59 Additional Income Retained by District D minus E 29 *Levy calculation based on available modeling suggests in range of 64% to 67% for NNDC e) Local Authorities will receive a RSG and the baseline funding level and RSG (less tariff) will determine the startup funding allocation for the Council. The RSG will be the share of additional money that is returned to authorities to make the retained amount of business rates up to the national total set out by the Treasury and will be in proportion to the individual funding targets. The distribution of RSG is to enable some stability within the overall funding system. 2.5 New Homes Bonus 2.5.1 Within the Comprehensive Spending Review the government announced plans for funding to be made available for the New Homes Bonus Scheme. The New Homes Bonus was a new scheme designed to incentivise and reward councils and communities who wished to build new homes in their area. 2.5.2 The key features of the scheme were as follows: a) The bonus would be paid as a grant, which in summary will from 2011/12 match fund the additional council tax for each new home and property brought back into use, for each of the 6 years after that home is built with an additional amount (£350) for affordable homes. The growth in the number of properties each year is calculated as new dwellings less any demolitions plus or minus the net change in empty dwellings. b) The match funding is split between upper and lower tier authorities on a 20/80 ration. Financial Strategy 2013/14 to 2015/16 October 2012 Page 4 of 26 c) The value of the bonus should increase for at least six years. The payment for 2011/12 was based upon the growth in new homes in the year to October 2010. The 2012/13 bonus reflects growth in the two years to October 2011. In the third year, the bonus will be based on the growth in the first, second and third years of the scheme and. d) Local authorities are able to spend the funding in line with local community wishes. This may have related specifically to the new development or more widely to the local community. For example, they may have wished to support frontline services like bin collections, or improve local facilities like playgrounds and parks. e) The government set aside nearly £1 billion over the Comprehensive Spending Review period for the scheme, including nearly £200 million in 2011/12 (year 1) and £250 million for each of the following three years. Funding beyond those levels would come from reductions in formula grant. National funding allocated for years 1 and 2 of the scheme are as follows: f) Year 1 Allocations - £199 million g) Year 2 Allocations - £431 million including, the second year one installment of £199 million and the first year two installment of £233 million. h) The bonus is paid through section 31 of the Local Government Act 2003 as an un-ringfenced grant. The New Homes bonus has now been operational for two years, the allocation for 2012/13 of £611,678 is made up of the following: 2.5.3 Allocation 2011/12 Allocation £ 2012/13 Allocation £ Year 1 349,762 349,762 Year 2 N/a 261,916 Total 349,762 611,678 The base budget for the current financial year assumed the total would be transferred to an earmarked reserve pending further decision about it’s use. 2.5.4 The technical consultation on the Business Rates Retention Scheme included implications to the NHB and future funding. Essentially the key points from the consultation documents was that £2billion would be taken out of each year’s spending control total (upto 2020 reset year) to fund the NHB. The Government’s aim is that NHB payments will be announced with the provisional Local Government Finance Settlement. 2.5.5 A policy on the use of the NHB which supports the government’s intention will be developed. 2.6 Local Council Tax Support Scheme (LCTSS) 2.6.1 Within the CSR 2010 the Government announced its intention to localise support for Council Tax from 2013/14 with an expectation that expenditure on the scheme would reduce by 10%. A detailed report was presented to Cabinet on 16 July 2012 outlining the changes to the scheme along with the detailed financial implications. 2.6.2 On 16 October 2012 the Department for Communities and Local Government (DCLG) announced transition grant funding of £100million being made available to encourage best practice in designing local schemes. Further details on the Financial Strategy 2013/14 to 2015/16 October 2012 Page 5 of 26 implications to Local Schemes of the funding is still to be announced and quantified although it is expected that applications for the funding will need to be made after 31 January 2013. The implications of the additional funding are being considered by the Council Tax Support Working Group. For information and background the following paragraphs provide an overview of the original scheme. 2.6.3 In summary, the new scheme is moving from a national system of council tax benefit which is currently budgeted to be funded 100% from Central Government via the Department for Work and Pensions (DWP), to a local support scheme for which the major preceptors and billing authorities will receive grant funding but at a level1 that is less than the current costs of the scheme in order to deliver the savings required by the Government. 2.6.4 The total cost of Council Tax Benefit in 2011/12 for NNDC was £8.2million (unaudited), the budgeted figure for 2012/13 is £8.1 Million. Based on the indicative grant funding that has been announced savings of £1.17m are required against the current scheme in order for a fully funded scheme to be implemented, i.e. with no impact on the Council’s budget from 2013/14. A draft scheme has been developed which is currently being consulted upon. The consultation period runs until 14 October 2012. The final scheme must be approved by January 2013 for implementation from April 2013. 2.6.5 Whilst it is a localised scheme the Government has set rules to protect pensioners on low incomes and also outlined some key principles of the scheme: 2.6.6 • Being means tested with most income taken into account and most outgoings not taken into account • Provide support for those who work so that they are better off than if they had relied on public funds • Protect those of pension age and protect if agreed, other residents who are considered could not be expected to work • Be seen to be a fair and reasonable use of public funds • Feature rules that are similar to those for other state benefits, to make the scheme easier to understand • Be operationally efficient and within budget. There is a risk that expenditure under the scheme being designed and implemented is greater than the amount of central Government funding for the scheme. This would mean that the costs of the scheme will fall to the major preceptor and billing authority in proportion to their respective shares of the council tax. Table 2 illustrates the position based on the indicative grants. Table 2 Average Band 2012/13 £ D % Saving Required £000 Norfolk County Council 1,145.07 75.43 887 Norfolk Police Authority 196.92 12.97 152 North Norfolk District Council 138.87 9.15 108 1 Based on indicative funding announcements. Financial Strategy 2013/14 to 2015/16 October 2012 Page 6 of 26 2.6.7 Local Precepting Authorities 37.20 2.45 28 Total 1,518.06 100 1,175 Reductions will be applied to council tax bills for CTSS in the form of a discount. This will mean the tax base for the authority will reduce. There is also expected to be a reduction in the collection rate as Council Tax will be payable by tax payers who previously would have received full benefit and no charge would be payable. These two factors will feed through to the Collection Fund accounting arrangements and will impact on the major preceptors and billing authority. The following illustrates the implications; figures included illustrate the current position for 2012/13: Council Tax Requirement (£5.745 million) Band D = Council Tax (£138.87) (Will be reduced as billing and major precepting authorities receive new funding, reducing the amount they need to raise through Council tax) Collection Rate (98.5%) X (Proportion of council tax which the billing authority thinks it will collect Number of Equivalents Band D (41,996.2) (Will be reduced because more dwellings will be eligible for reductions under the new scheme) 2.6.8 The impact on the Local Preceptors (Parishes) has recently been negated in terms of the tax base, the current consultation regarding this is recommending that two tax bases be maintained so that the Parishes will see no impact from the new scheme. The overall impact from the reduction in tax base is currently forecast to be offset by the grant for the scheme assuming that a fully financed scheme is implemented from April 2013. 2.6.9 Whilst the consultation has negated the impact to the parishes, it does create a risk to the major billing authority in terms of funding any scheme shortfall (relating to the parish element). 2.7 Council Tax Reforms 2.7.1 Councils currently have the discretion to reduce the amount of council tax payable for certain classes of dwelling for example second homes. For other classes of dwellings, in the past legislation has been prescriptive in terms of the lowest level of discount that the billing authority (i.e. NNDC) can make. Legislation for the new discretions is still to be passed and therefore this section provides an overview only of the proposed changes and the estimated financial implications to the Council. 2.7.2 The Government consulted on Technical Reforms to Council Tax in 2011 and published their response in May 2012. The changes include giving authorities new flexibilities on the level of discounts on second homes and empty dwellings. 2.7.3 There are essentially two drivers for the changes: Financial Strategy 2013/14 to 2015/16 October 2012 Page 7 of 26 (a) Local authorities will be given more local control to help them keep council tax down; (b) Providing authorities with stronger levers to encourage the effective use of housing stock, i.e. managing second home ownership and encouraging owners to bring empty dwellings back into use promptly. 2.7.4 Essentially while there are increased discretions that are being made available to Local Authorities in determining council tax discounts, they should not be seen as an additional income generation opportunity alone. The level of additional funding that could be made available to the authority from its share of the funds collected (9.1% of the total council tax bill), by changing levels of discounts needs to be considered alongside the additional resources in terms of administration, collection and system software updates that will be required to implement the changes. The following outlines the changes proposed and Appendix B provides a summary of each and the potential additional income available from the districts share of the council tax bill that could be generated from a number of the options. It should be emphasised that the estimates do not take account of non-collection. 2.7.5 Second Homes - The Government’s intention is that billing authorities are allowed to levy up to full council tax on second homes. There will be no duty imposed on a taxpayer to declare that a dwelling is a second home, therefore if the discount is removed completely there will be no incentive for taxpayers to let billing authorities know the status of a dwelling. If a discount is offered the Council will be able to seek information supporting a claim for discount, and require the taxpayer to notify the Council if they later cease to qualify for the any discount that has been given. The discretionary element of the second homes council tax is currently 40% on top of the 50% charge. The Council has an annual agreement with the County Council whereby 50% of the discretionary element (ie 50% of the 40% charge) is returned to the District and is used to fund the Big Society Fund. 2.7.6 Uninhabitable Dwellings - The Government’s intention is to abolish the Class A Exemption. This enables a taxpayer to claim a 100% reduction for an unoccupied property undergoing or needing major structural repair work. The property can be exempt for up to 12 months. Billing authorities will be allowed to give a discount which they can set at any amount up to 100%, for up to 12 months for such dwellings. 2.7.7 Vacant Dwellings - The Government’s intention is to abolish the Class C Exemption. An unoccupied and unfurnished property (including newly built properties), can currently be exempt for up to six months. Billing authorities will be allowed to give a discount for any amount up to 100% up to 6 months for such dwellings. 2.7.8 Empty Homes Premium - The Government’s intention is to allow billing authorities to levy a premium of up to 50% which can be added to the council tax charge for a dwelling that has been empty and unfurnished for two years. There is a current consultation on the Empty Homes Premium outlining proposals on dwellings which will not be liable for the premium. Essentially the consultation is recommending that where a dwelling is genuinely on the market for sale or letting then a premium should not be applied. 2.7.9 Long-term Empty Properties - The Government is not proposing any changes to existing legislation that currently allows billing authorities to grant a discount of between 0% and 50% on properties which have been vacant for more than 6 months (i.e. following the current class C exempt period). The Council allows no discount on properties more than 6 months. Financial Strategy 2013/14 to 2015/16 October 2012 Page 8 of 26 2.7.10 Other issues that need to be considered are the implications of implementing the changes in terms of software costs, administration and collection costs. Also there could be movements between classifications of properties for the home owner to benefit from the lowest Council tax charge which will reduce the level of additional income. 2.7.8 Discussions have been held on a county wide level in terms of setting a consistent discounts policy and options around returning a share of any additional revenues to the billing authorities. These are yet to be finalised and could be used to inform the local discounts policy. 2.8 Welfare Reform Bill 2.8.1 In February 2011 the Welfare Reform Bill was published which contained provisions for the replacement of Council Tax Benefit with a new localised scheme as outlined within the spending review. Consultation on the proposals for the localisation of council tax support from 2013/14 was launched on 2 August 2011. The Government published their response to the outcome of the consultation in December 2011 alongside the Local Government Finance Bill which contained the legislative provisions for the establishment of the localised council tax support schemes. 2.8.2 On 8 March 2012 the Welfare Reform Act received Royal Assent. The Act legislates a significant change to the welfare system by implementing a number of reforms to the benefits and tax credits systems with the aim of making the system fairer and simpler by: 2.8.3 • creating the right incentives to get more people into work • protecting the most vulnerable • delivering fairness to those claiming benefit and to the taxpayer. The main elements of the Act are: • the introduction of Universal Credit to provide a new single payment that supports people of working age who are looking for work or on a low income and will help claimants and their families to become more independent, • simplifying the current the benefits system by bringing together a range of working-age benefits (including Job Seeker’s Allowance, Income Support, Child Tax Credits, and Working Tax Credits and Housing Benefit) into a single streamlined payment that will improve work incentives • a stronger approach to reducing fraud and error with tougher penalties for the most serious offences • a new claimant commitment showing clearly what is expected of claimants while giving protection to those with the greatest needs • reforms to Disability Living Allowance, through the introduction of the Personal Independence Payment to meet the needs of disabled people today • creating a fairer approach to Housing Benefit to bring stability to the market and improve incentives to work • driving out abuse of the Social Fund system by giving greater power to local authorities • reforming Employment and Support Allowance to make the benefit fairer and to ensure that help goes to those with the greatest need Financial Strategy 2013/14 to 2015/16 October 2012 Page 9 of 26 • changes to support a new system of child support which puts the interest of the child first. 2.8.4 The main impact to NNDC is that housing benefit will no longer be administered by Local Authorities. There will be a long transition to the new system which is anticipated to be operational from 2017 although the intention is that new cases will be paid under the new system from October 2013. 3. FINANCIAL FORECAST UPDATE 3.1 The 2012/13 budget report as presented to Members in February 2012 identified a budget gap for 2013/14 of £266,508, increasing to £1,072,432 in 2014/15 and to £1,232,022 in 2015/16. This was based on a number of assumptions about future levels of external grant, spending plans, delivery of savings and additional income and a zero increase in council tax for the same period. 3.2 As already mentioned within the report, from 2013/14 there are significant changes to the financing of Local Authorities, moving from a system of government support allocated via redistributed business rates and Revenue Support Grant (RSG) to a system of localised business rates and RSG, with the new RSG largely being funded through the central share of business rates. 3.3 The principles of the new system include providing incentives for growth at a local level and a funding system that is simple and transparent. Year one (2013/14) of the new system will however involve the transition to the new scheme and will involve a degree of complexity. 3.4 The technical consultation on the Business Rates Retention scheme has now closed and following the decisions on the consultation the Provisional Local Government Finance Settlement (LGFS) for 2013/14 will be consulted on in the autumn2, although the exact timing has not been confirmed. The provisional LGFS will depend upon the content of the Chancellor’s Autumn Statement (date confirmed as 5 December 2012), and therefore the Council could expect to receive provisional grant figures not long before Christmas. 3.5 Taking into account the significant changes to the funding regime and the later notification of grant funding does make the budget setting process for 2013/14 onwards even more challenging. However the financial projections have been updated to reflect known spending pressures and also revised the income forecasts. 3.6 Resource Projections – the original forecast budget gap had assumed grant reductions over the spending review period from 2011/12 to 2014/15 of 24.3%, reducing by 5.2% in 2013/14 and to a further 7.7% in 2014/15 (Table 3 below). The original assumptions from the initial CSR2010 announcements were that grant reductions would be front loaded, i.e. in the first two years of the spending review period, i.e. 2011/12 and 2012/13. From 2010/11 to 2012/13 the Council has experienced grant reductions of £2 million, equating to nearly 25%3. 2 3 As outlined in the Consultation document 2010/11 £8.227 million to 2012/13 £6.225million Financial Strategy 2013/14 to 2015/16 October 2012 Page 10 of 26 Table 3 - Current 2010/11 Actual Funding £’000 Forecast Total Government Funding £000 2011/12 Actual £’000 8,227 Reduction £000 Reduction % 2012/13 Actual £’000 2013/14 Forecast £’000 2014/15 Forecast £’000 2015/16 Forecast £’000 7,202 6,225 5,903 5,451 5,451 1,025 977 322 452 0 12.5 13.6 5.2 7.7 0.0 3.7 More recent discussions at a national level have suggested that the reductions in 2013/14 and 2014/15 could be similar to those already experienced in the first two years. 3.8 Modelling of the impact of the new funding regime has been carried out using forecasting tools produced by SPARSE and the LGA. Initial results suggest that the overall funding reductions for NNDC for 2013/14 compared to the current funding for 2012/13 could be in the region of 6% to 8%. This is based on a number of local and national assumptions built into the model and excludes funding from the New Homes Bonus. Although there is a caveat in that this is not the final allocation method as the criteria has not yet been finalised. It would however be prudent to update the funding forecast to reflect reductions above those previously forecast and also carry out sensitivities analysis around these reductions. Table 4 – Grant Forecast (Updated) Total Government Funding £000 Reduction £000 Reduction % Additional to be factored into projection 3.9 2012/13 Actual £’000 6,225 977 13.6 2013/14 Forecast £’000 5,665 560 9.0 2014/15 Forecast £’000 5,155 510 9.0 2015/16 Forecast £’000 4,743 412 8.0 N/A 238 296 708 Sensitivity Analysis – the following illustrates the impact of a further 3% reduction in grant funding above the assumption in Table 4 above. 2012/13 Actual £’000 6,225 977 13.6 2013/14 Forecast £’000 5,478 747 12.0 2014/15 Forecast £’000 4,821 657 12.0 2015/16 Forecast £’000 4,291 530 11.0 Additional to be factored into N/A projection (compared to original) 425 630 1,160 Additional compared to Table 4 187 334 452 Table 5 - Sensitivity Analysis Total Government Funding £000 Reduction £000 Reduction % Financial Strategy 2013/14 to 2015/16 N/A October 2012 Page 11 of 26 3.10 Current Savings Programme – As previously mentioned the current budget anticipated ongoing savings and additional income totalling £1.2 million will be delivered increasing to £1.5 million from 2013/14. As previously reported in the budget monitoring report to Members in September there are a number of service and corporate work streams that are not being delivered as previously anticipated when the 2012/13 budget was set. The service savings and income have been assumed to be back on target from 2013/14 onwards as the impact in the current financial year is largely due to a delay in the implementation of the saving. The revised position is shown in Table 6 along with the additional costs which need to be factored into the future projections, mainly in relation to the impact of the corporate work stream financial implications. Table 6 - Updated Savings and Income Service Savings & Additional Income Corporate Workstreams: Management Restructure Pay and Grading Car Allowances Total Original Total Movement compared to Original* 2012/13 £ 2013/14 £ 2014/15 £ 2015/16 £ 862,147 923,277 920,501 920,501 250,000 77,000 0 1,189,147 1,272,542 83,395 250,000 62,000 245,000 1,480,277 1,517,723 37,446 250,000 62,000 245,000 1,477,501 1,510,947 33,446 250,000 62,000 245,000 1,477,501 1,510,947 33,446 * Additional cost to factor into projections 3.11 The latest forecast of corporate savings in relation to the management restructure now reflects the recruitment to all Heads of Service. Final service structure below the Heads of Service are still to be finalised, however additional savings of approximately £100,000 (above the original savings target of £150,000) are now anticipated. 3.12 The implications from the pay and grading review assumed a saving from the implementation date of 1 April 2012 of an earlier version of the pay model. Following the approval of an amended version of the pay scales model, a later implementation date of October 2012 and also the results of appeals the original level of savings will not be achieved. An earmarked reserve has been maintained to fund one-off costs associated with the review including the payment of arrears entitlement. The balance in the reserve at 1 April 2012 was £494,488 and it has been assumed that this will cover the one-off costs. 3.13 Investment Income – The current projections already take account of a fall in investment income over the next three years reflecting a reduction in the average balance available for investment along with a reduction in the average rate of interest. 3.14 Other Service Pressures and Savings – there are a number of service pressures and savings identified as part of the budget monitoring process that will have an impact on the current budget and future projections, the more significant items that are expected to have an ongoing impact include: • External Audit Fees – saving of £50,000 per annum from 2012/13 as a result to the changes from external auditing arrangements nationally following the demise of the audit commission. Financial Strategy 2013/14 to 2015/16 October 2012 Page 12 of 26 • • • • • 3.15 Administrative Buildings – business rates reduction following from a revaluation of the Cromer and Fakenham offices is anticipated to deliver ongoing savings of £25,000 per annum from 2014/15. Sports halls and Leisure Complexes – the impact of a reduction in income from sports halls and contract inflation in respect of the leisure complexes is estimated to be £27,000 per annum. IT – Savings from system changes in the year are anticipated to deliver an ongoing saving from licences of £20,000 per annum Non Distributed Costs – ongoing impact of inflationary increases to pension payments in respect of past employees, previously this cost has been covered by natural turnover in the pension scheme, annual cost of approximately £10,000. Pensions – Auto enrolment for the Local Government Pension scheme comes into operation from 2014. There will potentially be a cost implication associated with this if individuals that were previously not part of the pension scheme decided to join. Based on initial estimates the cost implication could be as much as £100k per annum, although not all may elect to remain in the scheme. It would still be prudent to factor in an estimate of the implications of this and at this time and therefore within the current projections £60,000 has now been included. There are also other service developments which will potentially have a financial impact and although have not been reported as part of the budget monitoring process need to be considered within the future finance projections. These include: • Investment in pooled property funds – a report was presented to Cabinet in October outlining the implications of investing in pooled property funds. The return on these types of investments is expected to deliver a higher return than the current average of less than 1%. Although there is an increased volatility of these returns it would however be prudent to factor additional investment income into the future projections of £150,000. In order to smooth the impact of the volatility of these returns on the revenue account year on year the use of reserves would provide a mechanism to cushion the impact. 3.16 Annex Building – Office moves are planned for the lower ground floor that will include relocating of services from the annex building. The removal of the annex will deliver annual revenue savings of approximately £20,000 from premises related expenditure including business rates, energy and cleansing costs. 3.17 Council Tax - An announcement has recently been made on funding a council tax freeze for 2013/14. National funding of £450 million has been announced and Councils who freeze their council tax next year will be eligible for a share of the funding over two years. Funding for the current year’s tax freeze grant totalled £850 million and equated to £143,613 for NNDC. The DCLG are due to announce further details of the scheme along with indicative break downs of the grant. As a guide for NNDC this would equate to £50,000 grant payable in 2013/14 and 2014/15. In addition announcements on the level of council tax increases that would trigger a referendum have been made, these thresholds have been reduced from 3.5% to 2%. The forward projection currently assumes a tax freeze for the duration of the forecast, as a guide a 1% increase in the current band D equivalent will generate additional resources of £50,000 per annum (this does assume a lower Council Tax base due to the implications of the LCTS on the as outlined at 2.6.7). Financial Strategy 2013/14 to 2015/16 October 2012 Page 13 of 26 3.18 Planning Fees - In recent years the economic recession and downturn in the construction industry have greatly affected the level of income generated from planning application fees. In 2011/12 the Council generated planning fee income of £429,455, the lowest level of income since 2002/03. The budget (for 2011/12) estimated £525,000 leaving a shortfall of £95,545 at the year end. Part of this shortfall was due to the inclusion of £50,000 which related to the anticipated introduction of a locally set fee structure although this never took place. Instead in July 2012 a ministerial statement was released which included notice that planning application fees will be increased by 15%. These changes were laid before parliament in July and are due for debate in both the House of Commons and the House of Lords in October. The exact date for the introduction of these increases is still unknown but it is expected to be late October/early November. 3.19 The Government has also subsequently announced a relaxation to planning regulations on a temporary basis (3 years) with the aim of stimulating the construction industry. The effect of this has not been fully quantified but the planning department do not consider that the negative effect to the Council’s budget will be material. 3.20 The base budget for fee income is currently £525,000 which as previously mentioned already includes £50,000 for fee increases, the proposed increase does provide a potential to increase the base budget, although this would need to allow for the additional staffing costs as agreed by Cabinet in September 2012. Pending the outcome of the peer review on the service no additional costs/savings have been factored into the budget forecast at this time. 3.21 Table 7 below provides a summary of the revised position taking account of the factors previously identified. These are subject to a number of caveats in relation to the grant forecast. Table 7 - Updated Financial Forecast Forecast Gap (Jan/Feb 2012) Revised Savings Plans (Table 6) Interest (3.13) Service Pressures/Savings (3.14) Other Service Savings/Additional Income (3.15) Revised Gap (before grant revisions) Grant Projections (Revision) (Table 4) Forecast Budget Gap Council Tax Freeze Grant (Estimate) Forecast Budget Gap (after Freeze Grant) 3.22 2013/14 £000 267 37 0 (55) (170) 79 238 317 (50) 267 2014/15 £000 1,072 33 0 5 (170) 940 296 1,236 (50) 1,186 2015/16 £000 1,232 33 0 5 (170) 1,100 708 1,808 0 1,808 The financial forecast as outlined in table 7 is dependent on a number of key assumptions which are not directly within the control of the Council. The most significant are: • Employee inflation – currently no decision has been made on future pay awards. The Council is part of a national pay agreement for which there has been a pay freeze since April 2009. As a guide a 1% increase equates to approximately £90,000 per annum. Financial Strategy 2013/14 to 2015/16 October 2012 Page 14 of 26 • External Funding – the uncertainty and sensitivity around the government grant has been outlined as a guide, compared to the current year a 1% reduction equates to approximately £60,000. • Inflation including contract inflation – inflation has been provided for within the projections for current service contract, fluctuations in the rate of 0.5% would equate to approximately £30,000 per annum. • Economic climate including bank base rate and investment interest rates. • Demand for services for which a fee or charge is made – car parking and planning fees are the council’s largest demand led income generating services are influenced by a number of external factors, including the weather and economy. • Council Tax – the current council tax base is 41,366, as previously mentioned this will change as a result of the LCTSS from 2013/14. Currently the overall impact has been assumed to be negated by the grant funding for the new scheme. In addition within the collection fund (council tax account) any surplus or deficit is shared amount the major preceptors and billing authority, when setting the council tax the anticipated surplus/deficit is taken into account. No growth in the tax base has been assumed as this is likely to be offset by a reduced surplus/deficit position on the collection fund due to uncertainties around council tax collection and the introduction of the new LCTSS. 4. CAPITAL 4.1 The capital programme is updated on a regular basis as part of the budget monitoring reports to Cabinet. A copy of the current capital programme is included within the period 6 Budget Monitoring report included within the November Cabinet Agenda. 4.2 The following table provides a summary of the current approved capital programme for 2012/13 plus the current forecasts for 2013/14 and 2014/15 along with a breakdown of relevant financing. NNDC funding includes capital receipts, contributions from revenue and reserves, external funding refers to grants and external contributions. Financial Strategy 2013/14 to 2015/16 October 2012 Page 15 of 26 Table 8 - Current Approved Capital Programme 2012/13 Updated Budget £ Jobs and the Local Economy Housing and Infrastructure Coast, Countryside and Built Heritage Localism Delivering the Vision Total Capital Expenditure Financing: Non NNDC NNDC Total Capital Financing 4.3 2013/14 Forecast 2014/15 Forecast £ £ 785,857 5,403,565 1,655,000 - 7,408,313 561,837 1,026,325 15,185,897 5,100,000 6,755,000 443,000 443,000 6,431,888 8,754,009 15,185,897 5,443,000 1,312,000 6,755,000 443,000 443,000 The table above reflects the recent restructuring of the capital programme to align with the new corporate priorities as contained within the Corporate Plan 20122015. Capital Resources 4.4 The current capital programme is funded from the following sources of finance: • • • • • Capital Receipts – generated from asset disposals and preserved tight to buy (both new and existing within the capital receipts reserve) Grants and contributions received from external sources including third parties and government Revenue – making a revenue contribution to capital VAT Shelter Receipts Earmarked reserves for example the capital projects reserves. 4.5 The VAT shelter and Preserved Right to Buy (PRTB) receipts are two sources of funding that relate to the transfer of the housing stock to Victory Housing that took place in 2006. The VAT shelter arrangement is a procedure agreed by HM Revenues and Customs and the DCLG to ensure no overall impact on taxation post transfer. If the Council retained the stock and carried out the maintenance works on the properties the VAT would have been recovered. The Housing Trust are unable to recover VAT, but the VAT shelter arrangement allows VAT to be recovered on qualifying works (which totalled approximately £50million) and the VAT on the element that is recovered is shared between NNDC and the Trust. The amount received by the Council under this sharing arrangement is limited to a value, and based on the current forecast is expected to end in 2014/15. This is when the total value of qualifying works as agreed as part of the stock transfer in 2006 will have been completed. 4.6 Under the PRTB arrangement the Council receives a share of the capital receipt generated from a right to buy sale. 4.7 Following the housing transfer the receipts generated from the VAT shelter and PRTB’s have been used for the financing of the capital programme. Since 2008/09 the VAT receipts has been payable as a revenue receipt and has been transferred to the Capital Projects Reserve. Payment as a revenue receipt provides greater flexibility in terms of funding spend, revenue receipts can be Financial Strategy 2013/14 to 2015/16 October 2012 Page 16 of 26 used to fund capital, however capital receipts cannot be used to fund revenue expenditure. 4.8 Another source of funding for capital expenditure is prudential borrowing. Prudential borrowing to fund capital expenditure can only be undertaken when an authority can demonstrate a need. The need to undertake prudential borrowing is demonstrated through its capital financing requirement which is driven by the balance sheet of the authority and takes into account reserves (including general and earmarked). Financing costs of the borrowing would be a charge to the revenue account. 4.9 The housing capital programme has been historically financed from government grant (mainly in relation to the disabled facility grants scheme), capital receipts (both retained from previous asset disposals and receipts generated from the PRTB’s) and VAT shelter receipts. Both of these sources of funding are diminishing in terms of the level of receipts generated annually and by 2014/15 the VAT shelter receipts will come to an end. 4.10 After taking into account the planned spend within the current capital programme for the period 2012/13 to 2014/15 and the anticipated resources, i.e. new capital resources4 for the same period there is currently an unallocated balance of just under £3 million. Although this does include £1.3 million within the capital projects reserve which is a revenue or capital resource. This is illustrated in the following table. Table 9 - Capital Resources Capital Receipts £ Balance at 31/3/12 Total £ 9,062,451 1,819,469 10,881,920 New Receipts 2012/13 Capital Financing 2012/13 406,000 (7,806,568) 429,180 (932,441) 835,180 (8,739,009) New Receipts 2013/14 Capital Financing 2013/14 390,000 (912,000) 413,340 (400,000) 803,340 (1,312,000) New Receipts 2014/15 Capital Financing 2014/15 390,000 0 256,709 (256,709) 646,709 (256,709) 1,529,883 1,329,548 2,859,431 Estimated Balance at 31/3/15 4.11 Capital Projects Reserve £ The housing strategy (2012/15) has been presented to Members, the following is an extract from the strategy in relation to its Local Investment Strategy. Action Outcome We will seek to maximise reinvestment in Use of investment income and capital receipts the delivery of affordable housing in the by Registered Providers to deliver affordable District by Registered Providers using housing investment income and capital receipts e.g. 4 New Capital Resources – Asset disposals, preserved right to buy and VAT shelter receipts. Financial Strategy 2013/14 to 2015/16 October 2012 Page 17 of 26 Action Outcome from the use of Affordable Rent tenancies, disposals, Right to Buy receipts We will explore opportunities to invest in Consideration of legal and financial the delivery of affordable housing in the implications and risks of investing in the District e.g. through the provision of loan provision of affordable housing. finance to Registered Providers 4.12 Currently delivery of affordable housing through the capital programme is by providing grants to housing associations. This is treated as one-off capital expenditure in that once the grant has been paid, it’s gone, i.e. there is no recycling of funding back to the authority. At a time when new capital resources are diminishing alternative options to deliver affordable housing need to be considered, including the provision of loans as an alternative to the payment of grant. 4.13 Under the current Regulations5, the loan would be capital expenditure, assuming the loan was for a purpose which, if the Council had incurred the expenditure directly, it would have been treated it as capital expenditure. 4.14 The loan would need to be financed using capital receipts (or other capital financing resources). If sufficient receipts are not available, the expenditure on the loan would cause the Council’s Capital Financing Requirement to increase, and it would be necessary to make an MRP (Minimum Revenue Provision) charge to the Revenue Account for the repayment of the loan. Repayment of the loan would generate a capital receipt. 4.15 Loans to Registered Providers are not covered by the Councils current Treasury Strategy and this would need to be amended. The loans would not, for example, meet the minimum credit rating requirement for an approved counterparty, which is one of the factors used to judge the security of funds invested. Interest earned on the loans would be a revenue income receipt. 4.16 The opportunities for the provision of loans in this way are being considered by Finance Officers along with the Council’s Treasury advisors. In principle it is moving from a system of providing grants from a fixed sum of available capital resource to a system where resources can be reused through a loan mechanism. 4.17 Alternative methods of delivering affordable housing and increasing the return on capital resources needs to be explored, moving from a system where capital receipts (or capital resources) are being used once to fund grants, to a system where capital resources can be recycled through the provision of loans where by future capital receipts would be generated for the authority. It is recognised that there is a risk of default and the loan may not be repaid, but this must be weighed against the payment of a non-repayable grant. 5. RESERVES 5.1 As part of the budget and council tax setting process each year the Chief Financial Officer must report on the adequacy of the reserves that the Authority 5 Regulation 25 (1) (d) of the Local Authorities (Capital Finance and Accounting) (England) Regulations 2003 (SI 2003 No. 3146) Financial Strategy 2013/14 to 2015/16 October 2012 Page 18 of 26 holds. This is informed by the Policy Framework for Reserves which is presented alongside the budget (annually)6. 5.2 5.3 5.4 The Council holds a number of ‘useable’ reserves both for revenue and capital purposes and generally fall within one of the following three categories, each as discussed in the following sections: • General Reserve • Earmarked Reserves • Capital Receipts Reserve The General Reserve is held for two main purposes: • To provide a working balance to help cushion the impact of uneven cash flows and avoid temporary borrowing • a contingency to help cushion the impact of unexpected events or emergencies Alongside setting the budget each year, the adequacy of reserves needs to consider the optimum level of general reserve that an authority should hold. The optimum level of the general reserve will take into account a risk assessment of the budget and the context within which it has been prepared taking into account a number of factors including: • • • • • • the level of savings that have been factored into the budget and the risk they will not be delivered as anticipated; sensitivity to pay and price inflation; sensitivity to fluctuations in interest rate; potential legal claims where earmarked funds have not been allocated if applicable; level of earmarked reserves held; a level of reserve that is within a 5% to 10% of net expenditure 5.5 The current level for NNDC is a minimum of £950,000 in the general reserve. The level of the general reserve from 2013/14 will be reviewed as part of the budget process over the coming months. Bearing in mind the uncertainty of the new funding regime that has been discussed earlier in this report, there could be an argument for at least maintaining the general reserve at its current recommended level or in fact increasing the recommended minimum balance at least in the short term to mitigate the impact in year one of the new funding regime. 5.6 Earmarked Reserves provide a means of building up funds to meet known or predicted liabilities and are typically used to set aside sums for major schemes, such as capital developments or asset purchases, or to fund major reorganisations. Earmarked reserves can also be held for service projects and business units which have been established from surpluses to cover potential losses in future years, or to finance capital expenditure. Earmarked reserves also provide a mechanism to carry forward underspends at the year-end for use in the following financial year where no separate budget exists. 5.7 For each earmarked reserve a number of principles should be established: • the reasons for or the purpose of the reserve • how and when the reserve can be used – short to long term • procedures for the reserve’s management and control. 6 Full Council 22 February 2012, Budget and Council Tax Report 2012/13 Financial Strategy 2013/14 to 2015/16 October 2012 Page 19 of 26 5.8 The establishment and use of earmarked reserves is reviewed at the time of budget setting, throughout the year as part of the regular budget monitoring processes and also as part of the year-end reporting. Review of earmarked reserves throughout the year takes into account the continuing relevance and adequacy of the reserve. 5.9 The Capital Receipts Reserve includes the balance of receipts generated from asset disposals. Capital receipts are generated when an asset is disposed of and can only be used to fund expenditure of a capital nature, i.e. not for on-going revenue expenditure. The balance of capital receipts is used to fund the capital programme. The balance of capital receipts at 31 March 2012 was £9.063 million. 5.10 Details of the current capital programme that are being financed from capital receipts were included in section 4 of the report which highlights the reducing available balance within this reserve over the next three years. 5.11 An updated reserves statement (general and earmarked) is included at Appendix C. This reflects the latest position for planned use of the earmarked reserves in the current and future financial years where known. There is still some uncertainty around the exact timing of the use of a number of the reserves, for which some are held as a contingency to mitigate a potential liability although the timing and likelihood of this is depended upon future event, these are outlined below: 5.12 • New Homes Bonus - The New Homes Bonus was a new scheme announced as part of the Comprehensive Spending Review and is designed to incentivise and reward councils and communities who wish to build new homes in their area. The reserve includes the allocation for the 2012/13 year. As mentioned earlier a policy will be developed for use of the New Homes Bonus. • Benefits - The Benefits reserve was established to mitigate any claw back by the DWP following audited subsidy determinations. The subsidy claim for 2011/12 is still to be audited. The level of this reserve has been maintained as the authority has introduced a new Revenues and Benefits computer system as part of its partnership with Kings Lynn and West Norfolk Borough Council. The reserve will be used to offset any loss of subsidy due to problems and delays in processing during the implementation stage. • LSVT - This reserve was established following the Large Scale Voluntary Transfer of the Councils Housing Stock to Victory Housing in 2006 when the council provided the trust with a number of warranties, guarantees and indemnities. • Big Society Fund - This reserve has been established as part of the councils approach to Localism and is being funded from 50% of County’s share of the discretionary element (40%) of second homes council tax charge which is returned to the district to be allocated to communities that identify where they will make a difference to the social wellbeing of the area via the Big Society Fund. Future contributions to and from this reserve are dependent upon the sharing arrangement with the County Council and will be determined annually as part of setting the budget. Whilst the balance is included within the Council’s accounts, it is held for the purpose of the Big Society Fund and Localism. In the short to medium term there is a need to critically review the minimum balance held in the General Reserve to reflect the uncertainty around a number of current and impending issues, namely: Financial Strategy 2013/14 to 2015/16 October 2012 Page 20 of 26 • Uncertainty of the new funding regime both for the first year (2013/14) and the ongoing impact in that there will almost certainly be variances between the budgeted level of external support (government grant and retained business rates) and the actual year end position; • The new system of localised council tax support. • Investment in pooled property funds and establishing a reserve or an element of the general reserve to even out the fluctuations in interest received year on year, and volatility in the value of the investment. 5.13 All reserves (general and earmarked) will be reviewed over the coming months as part of setting the detailed budgets for 2013/14 with a view that where commitments have not been identified funds or reserve balances are no longer required these are re-allocated to specific reserves to address the requirements identified at 5.12. 6 FINANCIAL STRATEGY 6.1 Consolidating the detailed financial pressures discussed above the financial strategy sets out how the Council wishes to manage its finances over the medium term to ensure it supports the achievement of the Council’s Corporate Plan objectives. 6.2 The base position for the strategy is the current 2012/13 base budget set last February against the backdrop of the national economic position and the pressures being experienced in the delivery of local services. 6.3 Whilst the funding situation for the forward year (2013/14) from Central Government will not be confirmed until December 2012, the Council must ensure that both short term measures and medium/long term measures are in place to secure the overall financial viability of the Council. 6.4 The strategy sets in place a set of initiatives that will allow secure business planning by recognising the external financial landscape both in terms of Central Government financial support and the continuing pressures on service delivery. 6.5 In the short term Cabinet has instructed managers to review their base budgets and to identify any savings or additional income streams that could be included in the 2013/14 base budget to include: • No impact or an acceptable level of impact on service delivery. • Income that can be derived without a significant change in policy. • Savings that have previously been considered where there is some impact on service provision. • A review of the levels of working and earmarked reserves. 6.6 This work will secure a balanced position for the 2013/14 budget and the Cabinet will then focus its attention on delivering the work streams that support the corporate plan and for which work is already underway and being monitored through working parties or working boards. 6.7 There are two distinct aspects to this work which support the strategic direction of the Council: • Creating new revenue streams by increasing the Council’s tax base for housing and business rates Financial Strategy 2013/14 to 2015/16 October 2012 Page 21 of 26 • Efficiency savings Creating new revenue streams by increasing the Council’s tax base for housing and business rates 6.8 The shift in Central Government support for local authorities has moved to incentivise them in developing stronger income streams from their property bases. Growth in both domestic and non domestic properties will lead to increased levels of funding which directly rewards the Council. 6.9 A growth in both of these areas will support the corporate priorities and position the authority to take advantage of the new funding regime being introduced from April 2013 as well as maximise existing funding streams. 6.10 No assumptions have been made in the financial forecast for the following revenue streams. The New Homes Bonus (NHB) 6.11 This payment is based on a formula related to the number of new homes completed or empty properties brought back into use in a twelve month period ending in October each year. As well as the additional council tax such dwellings generate the Council will also receive a sum of money equivalent to six years council tax at the average national rate for a Band D property. 6.12 Planning permissions granted and turned into completed developments support the corporate priority for housing and infrastructure in respect of “increasing the number of new homes built within the District and reducing the number of empty properties”. 6.13 As an example fifty new houses would generate an additional £57,800 per annum for six years (totalling £346,800) in new homes bonus and £6,940 per annum in council tax income (based on the current band D equivalent of £138.87). 6.14 In 2012/13 the Council will receive an estimated £261k for the year which together with £350k for 2011/12 is a total of £611k. 6.15 It is important to recognise that the New Homes Bonus going forward is not “new money” from the Central Government but rather a top slice of the total financial support available to local government. As such it reflects the move to directly reward planning authorities and stimulate the domestic property market. Business rates 6.16 The detailed report, above, examines the changes in this area. Embracing these changes will generate an increased in the total rateable value of the District from which the Council will derive an increased share of the associated income to support its expenditure plans. 6.17 The Council has as its first corporate priority a commitment to increase the number of new businesses and support the growth and expansion of existing businesses. By delivering on this commitment it is anticipated that this will result in an increase in the rateable value of the District. Financial Strategy 2013/14 to 2015/16 October 2012 Page 22 of 26 6.18 In the past three years there has been a slow but significant increase in the overall rateable value across the District. By making a positive commitment through the current Corporate Plan to assist business to grow it is anticipated that such an increase will continue over the medium term. Such growth will provide the Council with additional revenue resources the extent of which will become clearer as the new arrangements announced in the Business Rates Retention Scheme develop. Community Infrastructure Levy (CIL) 6.19 The Community Infrastructure Levy allows local authorities to raise funds from developers who are undertaking new building projects in their area. The funds so raised can be used to pay for a wide range of infrastructure that will be needed as a result of the development. 6.20 The CIL guidance includes a wide definition of infrastructure which can include transport schemes, flood defences, schools, hospitals and other health and social care facilities, parks, green spaces and leisure centres. Income from Planning Fees 6.21 Recent budgets for planning fee income have been set against the proposal that the Government intended to decentralise responsibility for planning application fees to local authorities. However, in July 2012 a separate announcement by the Minister for Decentralisation and Cities indicated that planning fees would increase by 15%. 6.22 Regulations have been laid before Parliament and are due to be debated in October 2012. No date for the increase to come into effect has been announced. 6.23 It remains a possibility that there may be future flexibility in setting planning fees locally, in order that this service is not subsidised by the general tax payer. Efficiency savings 6.24 Whilst it is important to focus on an agenda that will generate income from growth in our economy there is, none the less, a continuing need for the Council to reduce overheads and provide services more efficiently. 6.25 There are seven work streams being developed by Officers to meet the objectives set by the Cabinet and the Council. These initiatives are part of the Corporate Plan in “Delivering the Vision” by looking for “year on year improvements in efficiency”. They are as follows: Management Restructuring 6.26 The new Corporate Leadership Team and Heads of Service structure is now complete with savings of £250k to be factored in the budget from April 2013. These have been included within the updated financial forecast. Shared Services 6.27 The Revenues and Benefits project has already delivered on-going savings through the procurement of a new IT system. However, due to operational issues Financial Strategy 2013/14 to 2015/16 October 2012 Page 23 of 26 regarding the hosting of the software there will be delays in moving towards a shared management structure which had originally been anticipated for 2013. 6.28 No savings have been included within the financial forecast from this piece of work due to the business case being reviewed. However, it is anticipated at least £100k would be achieved from 2014/15 compared to current service expenditure. 6.29 In addition the Council continues to review its building control function and will consider further options for partnership structures within Norfolk. 6.30 At the same time an innovative approach to selling services is being developed by the legal team through establishing a cost sharing group which would allow services to be competitively tendered to local organisations. 6.31 More detailed papers will follow as the budget for 2013/14 and 2014/15 are prepared. Peer Review Planning Service 6.32 A peer review is designed to help a service assess its current achievements and its capacity to change and continue to improve. To this end an initial meeting has been held with representatives from the Local Government Association and members of the Cabinet to inform the terms of reference for the review of the planning service. This will include reviewing the allocation of resources, service performance and the use of technology. Procurement 6.33 . 6.34 Following on from a Cabinet paper in February 2012 the Council is a partner in a County-wide tendering process to handle dry recyclable waste collected by the Council. The tendering process is due to be completed this financial year and it is anticipated that an improved income stream will be available from 2014/15.The current contract expires in March 2014 Officers have also started to scope a new sports and leisure contract which would be operable from 2014. The work could embrace all sports facilities including those which are currently outside the current contract. The overall budget here is in excess of £816k and it is anticipated that savings in this service area will result from this work. Customer Services/Web Strategy 6.35 As the new management structures begin to become established Officers are reviewing the approach to customer services. The Website is by far the most cost effective way of transacting business and in developing an access strategy it will become the focus of many of the customer transactions in the future. 6.36 This will require maximising the functionality of the website to provide a greater level of integration across all service areas. Following this investment the next stage is to migrate customers away from the more expensive traditional channels over to the web by enabling and promoting self-service on the website. If customers are empowered to manage their own enquiries, and are able to access services online, the need of human intervention for processing and service delivery is reduced and this is where considerable savings can be made. Financial Strategy 2013/14 to 2015/16 October 2012 Page 24 of 26 Administrative Buildings 6.37 The overall cost of the Council’s current administration centres is £598k per annum (including capital charges and other recharges). As noted in the main body of the financial forecast there is on-going work to remove the annex to the main offices in Cromer with commensurate savings to the Council. 6.38 At the same time the review will also examine the potential use of the existing facilities with a view to economising on space and potentially creating a rentable floor space that can generate income and reduce further the administrative overhead that the building imposes. Risks 6.39 The financial strategy is based on a number of assumptions contained in the main body of the report which include: Inflation rates • Interest rates • The level of Government financial support • The level of financial pressures facing the Council 6.40 However, although the Council faces risks from the assumptions and uncertainties outlined above, these have been mitigated by: • Adopting a prudent approach to financial forecasting which involves obtaining information from external professional sources • Continuous monitoring and review of the key factors which involves regular reports to Members on major issues. • Risk issues on both expenditure and income levels which have been highlighted in regular budget monitoring reports to Cabinet Conclusion 6.41 The overall planning framework ensures that the Council’s Financial Strategy is a corporate document. Fundamental to the effectiveness of the planning framework is the need to ensure that the Financial Strategy adopts a corporate approach to revenue and capital spending that is consistent with the Council’s corporate objectives and the Council’s key planning documents. 6.42 In preparation for the anticipated reductions in Central Government support from 2014/15 onwards the Cabinet will review all service provision across the Council and include public consultation to inform future decision making. Financial Strategy 2013/14 to 2015/16 October 2012 Page 25 of 26 Appendices A Business Rates Retention Scheme – Illustration B Savings – Current Programme C Reserves Statement Recommendations It is recommended that Members note: 1) the current financial forecast for the period 2013/14 to 2015/16; 2) the current capital programme and capital funding forecasts; 3) the revised reserves statement as included at Appendix C to the report. Financial Strategy 2013/14 to 2015/16 October 2012 Page 26 of 26