Appendix C Prudential Indicator Monitoring Period 4 (July) 2011/12

advertisement

2011/12")

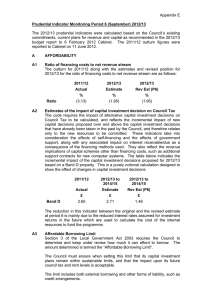

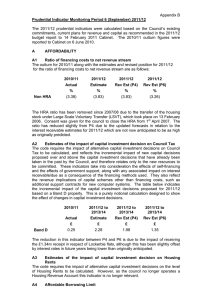

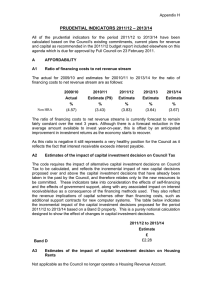

Appendix C Prudential Indicator Monitoring Period 4 (July) 2011/12 The 2011/12 prudential indicators were calculated based on the Council’s existing commitments, current plans for revenue and capital as recommended in the 2011/12 budget report to 14 February 2011 Cabinet. The 2010/11 outturn figures were reported to Cabinet on 6 June 2010. A AFFORDABILITY A1 Ratio of financing costs to net revenue stream The outturn for 2010/11 along with the estimates and revised position for 2011/12 for the ratio of financing costs to net revenue stream are as follows: Non HRA 2010/11 2011/12 2011/12 Actual Estimate Rev Est (P4) % % % (3.38) (3.83) (3.83) The HRA ratio has been removed since 2007/08 due to the transfer of the housing stock under Large Scale Voluntary Transfer (LSVT), which took place on 13 February 2006. Consent was given for the council to close the HRA from 1st April 2007. There have been no changes since the original 2011/12 estimate. A2 Estimates of the impact of capital investment decision on Council Tax The code requires the impact of alternative capital investment decisions on Council Tax to be calculated, and reflects the incremental impact of new capital decisions proposed over and above the capital investment decisions that have already been taken in the past by the Council, and therefore relates only to the new resources to be committed. These indicators take into consideration the effects of self-financing and the effects of government support, along with any associated impact on interest receivable/due as a consequence of the financing methods used. They also reflect the revenue implications of capital schemes other than financing costs, such as additional support contracts for new computer systems. The table below indicates the incremental impact of the capital investment decisions proposed for 2011/12 based on a Band D property. This is a purely notional calculation designed to show the effect of changes in capital investment decisions. Band D 2010/11 2011/12 to 2013/14 2011/12 to 2013/14 Actual Estimate Rev Est (P4) £ £ £ 0.25 2.28 1.98 The reduction on the original 2011/12 to 2013/14 estimate is due to a number of completed schemes underspending in 10/11 with no requirement for any carry forward. For example the budget for the contribution towards the replacement of the artificial pitch in Cromer was £66,000 but the final cost was nearly £8,000 less that this and, as the scheme was completed, there was no requirement to carry forward this budget to 2011/12. Similarly the purchase of the Splash invertors was £7,000 less than originally forecast. The income received from the disposal of the public convenience on Sheringham East Promenade was also more than 20% higher than anticipated. Appendix C Estimates of the impact of capital investment decision on Housing Rents The code requires the impact of alternative capital investment decisions on the level of Housing Rents to be calculated. However, as the council no longer operates a Housing Revenue Account this indicator is no longer relevant. A3 A4 Affordable Borrowing Limit Section 3 of the Local Government Act 2003 requires the Council to determine and keep under review how much it can afford to borrow. The amount determined is termed the “Affordable Borrowing Limit”. The Council must ensure when setting this limit that its capital investment plans remain within sustainable limits, and that the impact upon its future council tax and rent levels is acceptable. The limit includes both external borrowing and other forms of liability, such as credit arrangements (see note C2 below regarding debt redemption). Affordable Borrowing Limit B 2010/11 2011/12 2011/12 Outturn Estimate Rev Est (P4) £,000 £,000 £,000 9,100 9,325 9,325 PRUDENCE B1 Net borrowing and the Capital Financing Requirement The capital financing requirement measures the Council’s underlying need to borrow for a capital purpose. The Code states the following as an indicator for prudence: “In order to ensure that over the medium term net borrowing will only be for a capital purpose, the local authority should ensure that net external borrowing does not, except in the short term, exceed the total of capital financing requirement in the preceding year plus the estimates of any additional capital financing requirement for the current and next two financial years.” The Council met this indicator for 2010/11. It should be noted that, following the repayment of the council’s borrowing, the CFR has been reduced to zero. C CAPITAL EXPENDITURE C1 Capital Expenditure The capital expenditure estimates for the 2011/12 financial year for non-HRA takes into account current plans and future commitments as updated in the Final Accounts 2010/11 report as presented to Cabinet in June 2011, and the revised estimate therefore takes account of any slippage from the 2010/11 programme. Non HRA 2010/11 2011/12 2011/12 Actual Estimate Rev Est (P4) £,000 £,000 £,000 2,765 8,672 12,450 Appendix C C2 Capital Financing Requirement 2010/11 2011/12 2011/12 Actual Estimate Rev Est (P4) £,000 £,000 £,000 0 0 0 Non HRA The estimated capital financing requirement takes into account capital expenditure, the application of useable capital receipts, direct charges to revenue for capital expenditure, the application of capital grants and the use of third party contributions towards project costs. In summary, an increase in the capital financing requirement will reflect capital expenditure which is not resourced immediately representing an increase in the underlying need to borrow for capital purposes. Likewise a reduction in the capital financing requirement will reflect future applications of capital receipts or grants and contributions or future charges to revenue. Members should note that the Council repaid the principal element of its external debt on 17th May 2006 by using part of the receipt from the LSVT, effectively making the Council ‘debt free’. This repayment of debt has had the effect of reducing the CFR to zero. D EXTERNAL DEBT D1 External Debt – Authorised Limit The figures below are based on assumed actual borrowing, new supported debt, maturing and replacement debt. In addition, headroom for temporary borrowing and borrowing in advance of need has been incorporated. Authorised Limit 2010/11 2011/12 2011/12 Actual Estimate Rev Est (P4) £,000 £,000 £,000 9,100 9,325 9,325 The limit set for 2011/12 gives the Authority flexibility to borrow to finance possible short-term cash flow fluctuations and borrowing in advance of need if required. D2 External Debt – Operational Boundary The operational boundary is based on the same estimates as the authorised limit but reflects a more prudent additional headroom figure. Operational Boundary 2010/11 2011/12 2011/12 Actual Estimate Rev Est (P4) £,000 £,000 £,000 5,100 5,328 5,328 The limits for D1 and D2 will need to be reviewed in the future if the Authority decides to enter into any long-term borrowing. D3 Actual External Debt The Council’s actual external debt as at 31 July 2011 was zero, as highlighted in C2 above. This reflects the position at one point in time and is therefore not directly comparable to the authorised limit and operational boundary. Appendix C E TREASURY MANAGEMENT E1 Adopt the CIPFA Code of Practice for Treasury Management The Council has adopted the CIPFA Code of Practice for Treasury Management in the Public Services. E2 Interest Rate Exposure – Variable Rates It was recommended that the Council set an upper limit on its variable interest rate exposures for 2011/12 of 100% of its net outstanding principal sums (100% 2010/11). As the Authority is currently debt free and is not intending to enter into any long-term borrowing in the near future this indicator is not currently relevant. E3 Interest Rate Exposure – Fixed Rates It was recommended that the Council set an upper limit on its fixed rate exposures for 2011/12 of 100% of its net outstanding principal sums (100% 2010/11). However, as with E3 above, this indicator is not relevant at the present time. E4 Maturity Structure of Borrowing It was recommended that the Council set upper and lower limits for the maturity structure of its borrowings as follows: Amount of projected borrowing that is fixed rate maturing in each period as a percentage of total projected borrowing that is fixed rate Upper Limit Lower Limit Under 12 months 100% 0% 12 months and within 24 months 100% 0% 24 months and within 5 years 100% 0% 5 years and within 10 years 100% 0% 10 years and above 100% 0% These rates reflected the continuation of current practice but again the Authority’s debt free status makes this indicator irrelevant at present. E5 Total principal sum invested for period longer than 1 year. The indicator for the upper limit for longer-term investments is set at £15m for 2011/12. As at the end of July 2011 the Council had £6.0m invested for periods longer than 1 year.