A t a glance New in retirement

advertisement

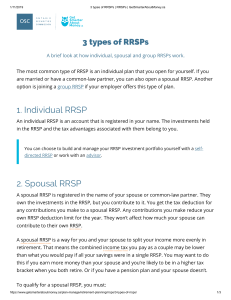

A t a glance Helping You Understand Financial Planning and Investments New income-splitting rules in retirement – still a role for the spousal RRSP Last October, the federal government announced a major change to how your pension income in retirement may be taxed. Spouses receiving pension income can now shift up to 50 per cent of this income from one to the other to minimize the overall income taxes they pay. New rules can save you money Shifting taxable income from a higher-income spouse to a lower-income spouse – often referred to as income splitting – is a significant tax saver, as a couple receiving two smaller incomes at retirement is taxed at a lower rate than one person receiving all of the household income. How significant are the savings? Here’s an example. If a couple has one spouse earning $60,000 in pension income, and the other earning no income, the spouse with the pension income could pay about $14,000 in federal and provincial income tax. But if this income is split between two spouses at $30,000 each, it can attract taxes of about $10,000 – a total tax savings of $4,000 each year (these figures will vary by province because of differences in provincial tax rates). The catch is that the new rules apply only to income that’s eligible for the pension tax credit. So if you’re age 65 or older, this includes income from: ■ pension plans ■ registered retirement income funds (RRIFs) ■ life income funds (LIFs) ■ locked in retirement income funds (LRIFs) ■ annuities purchased from RRSP or deferred profit sharing plan assets. If you are under age 65, the new income splitting rules apply only to income from pension plans, and some forms of annuity income. Continued ☛ A t a glance Helping You Understand Financial Planning and Investments The continuing role of spousal RRSPs Spousal RRSPs in action The traditional way of splitting retirement income in the past will still have a potential role to play since the new income splitting rules apply only to income eligible for the pension tax credit, and not to other income you may have in retirement, such as nonregistered investments or rental income. To recap on how spousal RRSPs work, when you contribute to a spousal RRSP, you get an immediate tax deduction, but the contributions are invested and controlled by your spouse. At retirement, when the spousal RRSP is converted to a RRIF or annuity, the income received is taxed in your spouse’s name, and usually at a lower tax rate. For this reason, you should still consider the potential benefits of a spousal RRSP used in combination with the new income-splitting rules. A spousal RRSP may be a good tax-saving strategy for you if: ■ you expect your spouse to be in a lower tax bracket during retirement ■ you expect to have a significant amount of investment, rental, or other non-pension income in retirement. In addition, your ability to split income before age 65 is limited to income from a registered pension plan. This means that if you retire at age 60, and are relying on income from a RRIF for example, you will not be able to split this income with a spouse until you are age 65. If you plan on retiring before age 65, setting up and contributing to a spousal RRSP today can be an excellent way to enjoy incomesplitting benefits in your early retirement years before the full income-splitting rules apply to you. Income split another way – contribute to an RESP Don’t forget – a spousal RRSP isn’t the only way you can split income and lower your family’s tax bill. If your child is likely to pursue post-secondary education, a Registered Educations Savings Plan (RESP) can be a valuable income-splitting tool. You can contribute up to $4,000 per year for each child, to a lifetime maximum of $42,000 for each child. While your contributions aren’t tax-deductible, all investment earnings within the plan accumulate tax-deferred. When the money is withdrawn from the RESP to pay for post-secondary education costs, it’s included in your child’s taxable income, not yours. Usually, that means there’s little or no tax to pay. In addition, the Canada Education Savings Grant program will match 20 per cent of RESP contributions per child each year to a maximum of $400 per year. Keep in mind, though, that spousal RRSPs are designed with retirement in mind. If your spouse withdraws funds from the RRSP in the year you make any contribution or the previous two calendar years, that income will be attributed back to you and included in your taxable income. The only exception is for Home Buyers’ Plan and Lifelong Learning Plan withdrawals. A first-time home buyer or individual pursuing post-secondary education may be able to withdraw funds from a spousal RRSP to fund these expenses. While the amounts must be paid back over time (by the spousal RRSP planholder, not the contributor), the spousal RRSP attribution rules do not apply to these withdrawals. i If you have a general question or suggestion about this newsletter, please send an e-mail to can_pencontrol@sunlife.com or write to At a Glance Newsletter, Group Retirement Services Marketing, Sun Life Financial, 225 King Street West, 14th floor, Toronto, ON M5V 3C5. Group retirement services are provided by Sun Life Assurance Company of Canada, a member of the Sun Life Financial group of companies. © 2007, Sun Life Financial. All rights reserved.