Document 11069597

advertisement

Contingent onvertibles. Solving or seeding the

next banking risis?

Christian Koziol∗

Johen Lawrenz

First draft: January 2010; This draft: February 2011

∗

Aknowledgment: We thank Manuel Ammann, Ken Behmann, Mark Grinblatt, Hendrik

Hakenes, Karl Ludwig Keiber, Jan Pieter Krahnen, Kolja Loebnitz, Kristian Miltersen, Alex

Mürmann, Stefan Pihler, Berend Roorda, Yves Shläpfer, Norman Shürho, and seminar

partiipants at the European Winter Finane Summit 2010, Symposium for International Corporate Finane and Governane in Twente 2010, University of Hannover, German Finane Assoiation Annual Meeting 2010 Hamburg, and the German Eonomi Assoiation of Business

Administration Frankfurt 2010. As always, all remaining errors are our own.

∗

Professor Dr. Christian Koziol, Chair of Risk Management and Derivatives, University of

Hohenheim, D-70593 Stuttgart, Germany, Email .kozioluni-hohenheim.de

Dr. Johen Lawrenz, Department of Banking & Finane, Innsbruk University, A-6020

Innsbruk, Austria, Email johen.lawrenzuibk.a.at, Phone +43-512-507-7582.

Contingent onvertibles. Solving or seeding the

next banking risis?

First draft: January 2010; This draft: Otober 2010

Abstrat

A reent proposal to enhane banking stability reommends the use of

ontingent onvertibles (CoCos). Sine these hybrid seurities are mandatorily onverted into equity when banks are in need of a reapitalization,

they are redited for reduing banks' likelihood of nanial distress. In this

paper, we show within a ontinuous-time framework that this allegedly

beneial impat hinges ritially on the assumption of omplete ontrats.

We show that although CoCos always distort risk taking inentives, CoCos an reate wealth for all involved investors. Our main ontribution is

to demonstrate that a higher investors' wealth from CoCo naning an

ause a higher bank's probability of nanial distress so that the banking

system as a whole will be destabilized. Thus, individually rational deisions an have systemially undesirable outomes. Further results indiate

that CoCos should be used only in onjuntion with devies to mitigate

risk shifting inentives. This objetive an be aomplished by a striter

regulation and a higher onversion ratio.

JEL lassiation: G32, G21, G28

Keywords:

Contingent apital ertiates, Reverse onvertibles, Restruturing

mehanisms, Regulatory hybrid seurity

1

Introdution

In the aftermath of the nanial market risis of 2008/09, several ulprits have

been named that ontributed to the near melt-down of the nanial system.

While still subjet to ongoing debate, there seems to be onsensus that one major

problem was related to the high leverage ratios of banks, whih left them with

severe problems of reapitalization when market onditions worsened abruptly.

One proposal, that has reeived muh attention in reent times to help alleviating the problem of exessive leverage ratios is to indue banks to issue so-alled

ontingent onvertible (CoCo) bonds, also known as enhaned apital notes or

ontingent apital. The key feature of these hybrid seurities is that they pay

oupons like normal bonds but are automatially onverted into ordinary shares

one the equity ratio falls below a predetermined threshold. This proposal has

gained momentum in November 2009 when Lloyds Banking Group launhed a

apital raising whih inluded the issuane of ¿7.5 billion in ontingent onvert-

1

ibles.

Governments as well as regulators seem to put muh hope in these new

2

seurities.

Only reently, the Bank for International Settlement announed that

as part of their reform pakage, they will review the role of ontingent apital

3

within the regulatory apital framework,

and in Switzerland, an expert group

reommended that banks will have to hold 19% apital, where nine perent are

required in ontingent apital.

4

Advoates of ontingent onvertibles onsider these hybrid seurities as a transparent, eient and less ostly resolution mehanism for distressed banks, beause

1 The ase of Lloyds has gained attention for two reasons. First, it was the biggest issuane

of CoCo bonds sofar and seond, the British government has a 43% stake in Lloyds. See

Finanial Times Lloyds to oer sweeteners to bondholders, November 1, 2009, and

Finanial Times UK experiment raises prospets of new asset lass, November 5, 2009.

e.g. the

2 As doumented in speehes by Ben Bernanke, hairman of the US Federal Reserve, Paul

Tuker, deputy governor of the Bank of England and Lord Turner, hairman of the Finanial

Servies Authority. See e.g. the speeh by Ben Bernanke to the US House Finanial Servies

Committee on Otober 1, 2009, the

2009 and

The Wall Street Journal

Finanial Times The sweet x of CoCos?, November 12,

Poliy Makers Disuss Bank Capitalization, November

17, 2009.

3 See the press release at January 11, 2010.

4 See e.g.

Capital proposal targets UBS and Credit Suisse, Otober 4, 2010.

Finanial Times

1

they provide an inrease of the equity ratio at pre-ommitted terms when the

bank is in a diult situation due to a severe loss of their asset value. Therefore,

this feature redues the danger of a ostly default or, alternatively, supervisory

intervention. At rst glane, the idea seems impeable. During good times, the

bank takes advantage of the benets of debt naning, suh as e.g. exploiting

naning and/or tax advantages, while in bad times, when debt obligations impose the risk of nanial distress, these seurities automatially onvert to equity

and mitigate the default risk.

In some sense, ontingent onvertibles seem to be the ake, one likes to have

and eat it too.

However, a fundamental doubt that CoCo bonds do the trik,

omes from theoretial onsiderations about the optimality of debt naning. A

large body of literature argues that within an inomplete ontrats setting, debt

is an optimal naning arrangement beause it oers xed payments in good

states, while in bad states it stipulates transfer of ownership. The threat of losing ownership, or more generally ontrol rights, exerts a disiplining eet on the

deision-makers of the rm. Hart and Moore (1998) undersore the important

distintion between ash ow rights and ontrol rights for the theoretial explanation of debt ontrats. However, by onstrution, CoCo bonds postpone the

transfer of omplete ontrol rights.

Thus, ontingent onvertibles may distort

deision-makers' inentives.

This paper is, to the best of our knowledge the rst theoretial ontribution that

tries to shed light on potential drawbaks of ontingent onvertibles due to distorted risk inentives. Within a ontinuous-time strutural model, we onsider

a ommerial bank engaged in the deposit taking business whih satises additional naning needs by aessing apital markets.

In line with the pratial

evidene from Lloyds, we analyze the impat of exhanging straight bonds with

ontingent onvertible bonds. In our analysis, we distinguish between two ases:

A omplete ontrat and an inomplete ontrat setting. In the former, we assume the investment poliy of the bank to be given (or to be ontratible), while

in the latter ase bank managers have disretion over the hoie of the bank's

investment risk. From our analysis, we nd that CoCo bonds are unambiguously

beneial if the bank annot hange its business risk. However, we also nd that

results hange dramatially if we onsider inomplete ontrats. We show that

2

CoCo bonds always distort risk taking inentives and indues deision-makers to

at less prudent. As a main result, we demonstrate that although CoCo bonds

are optimal in the sense that they are fairly pried and rm value maximizing,

the distorted risk-taking inentives an atually inrease the bank's probability

of nanial distress as well as the expeted distress osts substantially. Contrary

to the initial intention, CoCo bonds an reate negative externalities for the

eonomy in the sense that individually rational deisions may have systemially

undesirable outomes.

While normal onvertible bonds have been analyzed extensively in the literature (see e.g. Brennan and Shwartz, 1977; Ingersoll, 1977; Brennan and Shwartz,

1980; Brennan and Kraus, 1987; Nyborg, 1995), there are only few reent aademi ontributions dealing speially with

ontingent

onvertibility provisions.

Flannery (2005, 2009) argues that ontingent onvertibles are an eetive mehanism to exert market disipline, beause by issuing CoCo bonds shareholders

internalize, i.e. bear the full ost of their risk taking deisions rather than rely

on the (ostless) regulatory bail-out option. In a related analysis, Landier and

Ueda (2009) disuss several options for a bank restruturing, among whih they

mention onvertible debt. In line with the reasoning by Flannery (2009), they

onlude that onvertibles an derease the probability of default (see Landier

and Ueda (2009), p. 25). Aharya et al. (2009) simply state in their reent ontribution that assesses the strengths and weaknesses of the US nanial reform

legislation: Contingent apital is learly a good idea .5

More reently, Glasserman and Nouri (2010), Pennahi (2010), and Sundaresan

and Wang (2010) put forward theoretial models of CoCo bonds.

Glasserman

and Nouri (2010) and Pennahi (2010) both analyze the priing of CoCo bonds

when onversion an take plae ontinuously (Glasserman and Nouri, 2010) or

when the bank's asset value follows a jump-diusion proess and interest rates

are stohasti (Pennahi, 2010).

Sundaresan and Wang (2010) fous on the

design of the onversion trigger, and argue that for a wide lass of trigger mehanism there does not exist a unique equilibrium for equity and bond pries, thus

opening up the possibility of prie manipulation.

5 Aharya et al. (2009), p. 43.

3

The work by Flannery (2005, 2009) has reeived onsiderable attention and CoCo

bonds have been mentioned favorably in poliy reommendations by e.g. Stein

(2004), Kashyap et al. (2008), Kaplan (2009), and Due (2009). While ontingent onvertibles are welomed by pointing out their ability to overome problems

of high leverage, Hart and Zingales (2009) reognize that the proposal by Flan-

6

nery (2005) eliminates some of the disiplinary eets of debt.

However, sine

their fous is on the implementation of a new apital regulation for systemially

important banks, they do not explore that issue in detail. As a further poliy

reommendation, the so-alled Squam Lake Working Group on Finanial Regulation advoates the use of ontingent apital as a transparent, eient and less

7

ostly resolution mehanism for distressed banks.

One of the few onerns that have been raised against CoCo bonds so far points

towards a potentially destabilizing eet whih might our when large institutional investors, who are not allowed to hold shares, are fored to sell their

onverted bond position.

This eet might exaerbate the share prie deline

8

and spur doubts about the bank's stability.

With respet to a potential moral

hazard problem, the aademi literature so far seems to onsider risk-shifting

problems of CoCo bonds to be marginal at most.

Flannery (2005, 2009) on-

ludes from verbal reasoning rather than from a formal model-based approah

that risk-taking inentives an be ontrolled through the internalization of riskshifting osts.

Pennahi (2010) admits the presene of risk-shifting inentives

but argues that they are less pronouned as with subordinated debt. Glasserman

and Nouri (2010) analyze how higher risk impats the yield spread, but do not

explore the stability onerns of CoCo bonds.

Thus, to the best of our knowledge, our ontribution is the rst that fouses on

potentially adverse impliations of CoCo bonds from distorted risk-taking inentives. In the light of the reent banking risis, it need not be stressed that the

analysis of banks' risk taking behavior is of ruial importane. Our results are

6 See Hart and Zingales (2009), p. 5.

7 The Squam Lake Working Group resembles fteen distinguished aademis as e.g. Darrell

Due, Douglas Diamond, John Cohrane, Robert Shiller and Raghuram Rajan. See Squam

Lake Working Group (2010).

Finanial Times Stability onerns over CoCo bonds, November 5, 2009, and Finanial

Times Report warns on CoCo bonds, November 10, 2009.

8 See

4

an important warning signal that CoCo bonds may reate negative externalities,

in the sense that the (destabilizing) risk-shifting problem indued by CoCo bonds

may overompensate the (stabilizing) eet of providing a pre-ommitted reapitalization to banks.

The artile is organized as follows.

The next setion sets up the general

model framework and determines the optimal naning behavior with straight

bonds and CoCo bonds. In setion 3, we analyze the impat of CoCo naning

if omplete ontrats an be written, i.e. when the bank has no disretion over

the risk tehnology. Setion 4 analyzes the ase where ontrats are inomplete,

i.e. the bank an hange the investment risk. Setion 5 onludes.

2

General Model Framework

2.1

Initial Bank

In line with Bhattaharya et al. (2002), Deamps et al. (2004) and Rohet (2004),

we onsider a bank with assets in plae that ontinuously generate instantaneous

ash ows before taxes equal to

xt , whih are assumed to be driven by a Geometri

9

Brownian Motion

dxt = µxt dt + σxt dzt ,

where

µ and σ

are onstant drift and diusion parameters, and

(1)

zt

denotes a stan-

dard Wiener proess. We will apply the arbitrage-free valuation priniple where

(for priing purposes) the proess in (1) is onsidered under the risk-neutral measure

Q.

In the following setions, we will analyze both, the ase where the proess

of the ash ows governed by

µ

and

σ

is exogenously given, and the ase where

bank managers have disretion over the ash ow proess and an swith to a

9 While being a standard assumption in the literature, the assumption of Geometri Brownian

Motion implies that EBIT is always non-negative. However, this is no major restrition sine

it does not hange the general behavior of a bank as EBT (i.e. EBIT after interest payments)

an still beome negative, whih then requires outside naning. Furthermore, in pratie,

the EBIT of banks is virtually never observed to be negative.

5

dierent risk parameter

σ.

An inrease in the bank's ash ow risk an be inter-

preted either as a relaxation of monitoring ativities in the sense of less areful

risk management ativities (see e.g. Deamps et al., 2004), or as a shift in the

investment poliy towards more risky seurities as in the lassi asset substitution

problem (see e.g. Jensen and Mekling, 1976; Green, 1984; Leland, 1998).

As a seond salient harateristi, we adopt the frequently made assumption in

the nanial intermediation literature that banks' assets are sold at a signiant

disount when the bank is losed.

The disount may reet the illiquidity of

banks' assets due to speialized human apital (as e.g. argued in Diamond and

Rajan, 2000, 2001) or adverse seletion osts due to opaity, i.e. information

asymmetry.

10

In this sense, at the time of losure

to have a liquidation value of

11

rate.

xT

Λ = λ r−µ

,

where

We onsider a orporate tax rate equal to

12

the private level.

r

τ

T,

banks' assets are assumed

denotes the risk-free interest

and ignore additional taxes on

Sine the liquidation value annot exeed the after-tax risk-

less value of a perpetual ash-ow stream,

This formulation of

λ

λ

has to lie between zero and

omprises as a speial ase the frequently employed all

equity value after taxes and bankrupty osts whih is well-known as

λ = (1 − α) · (1 − τ )

(1 − τ ).

for proportionate bankrupty osts

xt

λ r−µ

with

α.13

On the liabilities side, the main harateristi of ommerial banks is their ability

to take deposits. We assume the bank to have a given volume of deposits that

require an aggregate ontinuous, instantaneous interest payment of

d

d.

We take

to be exogenous. The reasoning behind the fat that in our model, the bank

annot arbitrarily hoose the deposit volume is as follows. On the one hand, the

available amount of deposits is limited so that a given maximum amount an

hardly be exeeded without oering unreasonable high deposit rates.

On the

other hand, deposits are a possibility to reate a lose relationship to ustomers

10 See e.g. Stein (1998) for an adverse seletion model, and Morgan (2002) for evidene on the

opaity of banks' assets.

11 As it is standard, r is assumed to be onstant and µ < r to ensure nite solutions.

12 This is only for reasons of parsimony and does not hange subsequent results as long as there

is a tax advantage to debt naning after orporate and personal taxes. Furthermore, we

assume that losses ause immediate (negative) tax payments, whih ontrasts with a more

realisti asymmetri tax-regime, but whih is imposed for tratability reasons.

13 See e.g. Leland (1994), Goldstein et al. (2001), and Morelle (2004).

6

and an therefore be understood as an option to future valuable deals (e.g. after

investing into deposits, a ustomer might want to nane the aquisition of a

ostly good by a loan from the bank). Thus, the bank must keep the deposits on

a given level to avoid an ineient redution of the future business. As a result,

our model aounts for the fat that banks have a positive deposit volume with

an exogenous nature.

As long as the bank is solvent, depositors reeive their ontratual interest payment

d.

The residual ash ow

bank's equity holders. Sine

xt

(xt − d) (1 − τ )

is paid out as dividends to the

an be onsidered as the earnings before interest

and taxes (EBIT), the dierene

xt − d

denotes EBT, and thus

(xt − d) (1 − τ )

denotes the after tax dividend payment. We assume that total revenues are entirely paid out to investors.

debt struture.

Moreover, we do not allow for adjustments of the

With this stati view, we aount for the fat that espeially

during times of a banking risis, banks only have very limited possibilities to

adjust the apital struture. Given that the apital struture ould be arbitrarily

adjusted at no osts, a default ould be prevented in our model (see e.g. Koziol

and Lawrenz, 2009).

A typial approah within this model lass from the orporate nane literature (see e.g. Fisher et al., 1989; Leland, 1994; Goldstein et al., 2001) is to assume

perfet markets and unregulated rms. Therefore, equity holders are willing to

injet apital as long as they onsider it to be a worthwhile investment, and default of a rm an only our for reasons of indebtedness. The default event is

a result of the optimizing behavior of owners and therefore endogenous. While

this may be a reasonable approah for modeling the default deision of standard

non-nanial rms, it may be less appropriate for banks for basially two reasons.

First, banks are regulated and not at least due to mandatory minimum apital

requirements, the default deision is subjet to an exogenous onstraint.

This

is onsistent with e.g. Deamps et al. (2004). Seond, as witnessed during the

reent banking risis, banks in nanial distress fae various diulties or osts

in raising apital. Thus, severe nanial fritions in times of stress also impose

exogenous onstraints on the naning of banks, and an result in default for

reasons of illiquidity. The importane of the inability to raise apital in times of

7

stress need not to be emphasized in light of the reent turmoil on international

nanial markets and is the very reason that underlies the proposal for ontingent

onvertibles.

For these reasons, we onsider nanial distress as being triggered by an

ogenous onstraint

ex-

that may be interpreted in both ways. Either as regulatory

intervention, or as the inability to raise further apital. In tehnial terms, nanial distress is modeled as a stopping time, whih is dened as the rst time, the

xt

ash ow proess

hits the boundary

ξ

from above, i.e.

Tξ = inf{t; xt ≤ ξ}.

It is reasonable to expet that the nanial onstraint, i.e. the boundary

ξ

will

depend on the extent of the bank's debt liabilities. In terms of a regulatory intervention threshold, it is onsistent with a minimum apital requirement. Therefore,

we onsider the exogenous boundary to be related to the bank's debt liabilities

in a linear way:

ξ(π) = φ π,

where we use

π

(2)

to generally denote the bank's instantaneous payments to all

debt holders, and

φ>0

as a onstant that determines the severity of nanial

onstraints.

Note that in order to be binding, the exogenous threshold

as high as the endogenous default threshold

ξ ∗ (π)

ξ(π)

must be at least

that would be optimal for the

shareholders without any exogenous restritions.

Under the assumptions of the model, it is standard to show that the valuation

of equity holders' laim, denoted as

Q

St = E

Z

Tξ

−r(s−t)

e

t

= (1 − τ )

Note that

β

xt

ξ

St ,

is given by

14

(1 − τ )(xs − π) ds

xt

π

−

r−µ r

−

ξ

π

−

r−µ r

xt

ξ

β !

,

(3)

is to be interpreted as a probability-weighted disount fator, or

as the state prie of one unit of aount onditional on the event that

14 See e.g. Fisher et al. (1989), Mella-Barral (1999) and Deamps et al. (2004).

15 To ease notation, we will be sloppy sometimes, and write ξ without argument.

8

xt

hits

ξ .15

β

is the (negative) solution to the quadrati equation

given by

β = −(µ − σ 2 /2 +

q

σ2

β(β

2

2 r σ 2 + (µ − σ 2 /2)2 )/σ 2 .

− 1) + µβ − r = 0,

For ease of notation, we use the following onvention. Write V(y, π) = (1

β

y

τ ) r−µ

− πr , and D(y, y ′) = yy′ , then (3) is more ompatly expressed as

St = V(xt , π) − V(ξ, π)D(xt, ξ).

−

(4)

π

If the bank has only deposits, the total interest payment to debt holders,

equals

d.

We assume deposits to be insured, where the bank has to pay a fair

deposit insurane premium. Sine the work of Merton (1977), it is well known

that the value of the deposit insurane protetion orresponds to the value of a

orresponding put option, whih we denote by

I .16

For a given deposit volume

d,

the insurane premium is found to be

It = max

λ

d

ξ − , 0 · D(xt , ξ).

r−µ

r

(5)

Obviously, insurane makes deposits riskless. If depositors disount future interest payments at the risk-free rate

equals

D = d/r .

the aggregate deposit value, denoted as

Therefore, sine the bank pays

deposits for the bank is

2.2

r,

It

D,

for protetion, the value of

D − It .

Bank With Bond Finaning

While deposits are given, the bank an aess apital markets to satisfy additional naning needs. In the following, we will ompare two types of bonds, a

straight bond and bonds exhibiting the mandatory onvertibility feature.

For

tratability, we assume a straight bond to be a xed-oupon onsol bond that

promises a ontinuous instantaneous oupon payment

tal interest payment

π

of the bank is therefore:

debt liabilities will raise the default threshold

b

to bondholders. The to-

π = d + b.

ξ,

In general, the higher

sine due to the higher interest

payment obligation, the bank runs into nanial diulties already at higher ash

ow levels. In ase of default, most banking systems stipulate seniority among

debt laims for depositors with bondholders being subordinated. Aording to

16 An alternative onsideration of 'heap' deposits would not ruially aet our analysis beause the important relationship between the equity value and risk still remains.

9

this priority struture, the available reovery value should be split in a way that

bondholders obtain part of the liquidation value only if depositors have been

ompensated in full.

In pratie, absolute priority annot always be enfored,

and the atual split-up is often the result of a bargaining proess. It would be

straightforward to expliitly model the sharing rule as a (Nash) bargaining solution following e.g. Fan and Sundaresan (2000) and Mella-Barral and Perraudin

(1997). However, for our purposes, the preise sharing rule is not ruially important for the following reason. As long as equity holders' laim in default is

not aeted by the sharing rule,

17

the split-up among debt holders is irrelevant

to equity holders and therefore does not aet any deisions made by the bank

owners.

We take this fat as justiation to pursue a redued-form modeling

approah, and to assume that a ertain fration

θ

of the liquidation value

to bondholders. Similar to (3), the value of the straight bond at time

as

Bt ,

t,

λξ

goes

denoted

an be expressed as

b

b

Bt = + θλξb −

D(xt , ξb ).

r

r

Note that the knowledge of

total debt value

B0 + D − I0

θ

is not required for our analysis, beause only the

net of insurane osts will be required, whih is inde-

pendent of the distribution of the bank between the depositors and bondholders

in the ase of a default. The equity value an still be expressed as in (4), with

π = d + b,

b

and a presumably higher

ξb

whih we distinguish with the supersript

to indiate the straight bond ase.

While we take the deposit volume as exogenous, we assume the bank to optimally adapt their remaining naning needs by issuing a orresponding amount

of bonds (proxied by the aggregate oupon payment). Therefore,

variable, and the optimal bond oupon

b∗

b

is a hoie

is the result of the maximization of the

value of all laims net of the value of the deposit insurane premium

b∗ = arg max{Stb + Bt + D − It }

b

As usual, the maximization of the bank value

Stb + Bt + D − It

the maximization of the equity holders' wealth

Stb + Bt − It .

is onsistent with

This is a result of

17 This ondition is most obviously satised if priority between debt and equity holders is

enfored, and equity holders' laim in default is zero.

10

the notion that equity holders keep the stoks, pay the deposit insurane

ash injetions and reeive a speial dividend equal to the bond value

oupon

Bt .

with

(Sine

d/r

and is therefore independent of the

ξb = φ · (d + b),

the rst derivative of the bank value

the deposit value is insured,

D

It

equals

b.)

With the general onstraint

Vtb = Stb + Bt + D − It

with respet to

b

is

τ

ζ

∂ Vtb

= − D(xt , ξb ),

∂b

r

r

where

ζ =

(1−β)((r−µ)τ +φr((1−τ )−λ)

. From the properties

r−µ

λ ≤ (1 − τ ) < 1,

for

it follows that

D(xt , ξb) → 0,

that

(6)

D(xt , ξb)

ζ >τ >0

ξb

and

D(xt , ξb ) → 1.

The fat

(i.e. in the debt level) onrms the

existene of an optimal debt level. Solving the rst order ondition yields

xt

b =

φ

∗

0 ≤

whih implies a positive derivative

while the derivative is negative for

inreases monotonially in

β < 0, φ > 0

−1/β

τ

− d.

ζ

b∗

as

(7)

The rst term on the right-hand side of (7) determines the debt apaity of the

bank whih depends upon its growth potential, risk, urrent ash ow level, the

liquidation osts

λ

and the strength of nanial onstraints

veried from (7), high liquidation osts (small

onstraint (high

λ)

φ) urtail the bank's debt apaity.

φ.

As it an be

as well as a strong nanial

Note that in the optimum, a

bank issues less bonds if it has already a high volume of deposits. We assume that

the exogenously given deposit volume is suh that the bank has not exhausted

its debt apaity, i.e.

2.3

b∗ > 0.

Bank With CoCo Finaning

As an alternative to raise apital with a straight bond, the bank an issue ontingent onvertible (CoCo) bonds. Before onversion, CoCo bonds are equivalent

to ordinary straight bonds in that they pay a xed oupon rate. We denote the

ontinuous instantaneous oupon payment of CoCo bonds as

c.

The main dif-

ferene to straight bonds is the onversion feature. The ontrat of CoCo bonds

stipulates that onversion will take plae one the (ore) apital ratio of the bank

falls below a ertain threshold.

Upon onversion the former bondholders will

11

hold an equity laim, i.e. they reeive newly issued shares, whih entitles them

to a fration of the bank's prot. In our model setup this is neatly reeted by

introduing the parameter

γ,

whih denotes the fration of the bank's after-tax

prots that goes to former CoCo bondholders. If the number of shares (after onversion) is normalized to 1,

γ

is also neatly interpreted as the number of shares

going to former CoCo bondholders. The fat that former equity holders reeive

the remaining fration

1 − γ,

whih is less than before onversion, is onsistent

with the dilution eet of a seasoned new issue. Obviously, former bondholders

also reeive proportionate voting rights.

To formalize the onversion feature, we dene the ash ow barrier

χ

as the

threshold at whih the bond is onverted into equity. Sine after onversion, the

debt only onsists of deposits, the bank has a smaller interest payment obligation.

The redued debt obligations lower the default threshold

supersript

c

to indiate the ase of the CoCo bond.

threshold denition in (2), we have

of

χ

χ = φ · (d + c)

ξc ,

where we add the

By applying the general

and

ξc = φ · d.

This hoie

ensures that a onversion takes plae at a time when the bank would fae

nanial distress if it had not issued bonds with a mandatory onvertibility fea-

χ

ture. Furthermore, the hoie of

shields for given interest payments

CoCo bonds at time t, denoted by

also ensures that the highest volume of tax

d+c

18

an be generated.

The valuation for

Ct , and the value of initial (old) equity holders

is given by

c

(1 − D(xt , χ)) + γ D(xt , χ) (V(χ, d) − V(ξc , d) D(χ, ξc))

r

= V(xt , d + c) − V(χ, d + c) D(xt , χ) +

Ct =

Stc

(1 − γ) D(xt , χ) (V(χ, d) − V(ξc , d) D(χ, ξc))

As

xt → ∞, D(xt , χ) → 0,

and

Ct

approahes

c/r ,

(9)

i.e. for very high ash ow

levels, the value of the CoCo bond approahes its risk-free value.

χ, D(xt , χ) = 1,

(8)

At

xt =

and CoCo bondholders are holding an equity laim worth

γ (V(χ, d) − V(ξ, d) D(χ, ξc)),

i.e. a fration

γ

of total equity.

Eventually, we are interested in evaluating if a CoCo bond is an attrative

alternative for the bank.

At rst glane, it seems meaningful to ompare the

18 We explore the impliations of dierent hoies for the onversion threshold in setion 4.3.

12

bank's equity value when it has a straight bond outstanding to the ase when it

raises the

same amount of debt with a CoCo bond.19

However, suh an approah

ignores the fat that a CoCo bond issue an hange the overall debt apaity

of the bank. Therefore, we need to solve a related maximization problem as in

the previous setion, i.e. the optimal CoCo bond oupon

where

Vtc = Stc + Ct + D − It

c∗

has to solve

maxc Vtc ,

is the bank value (inluding the deposit insur-

ane obligation) under CoCo naning. Plugging in from (8) and (9), the rst

derivative of

Vtc

with respet to

c

is

τ

ζc

∂ Vtc

= − D(xt , χ),

∂c

r

r

where

ζc =

τ (π−c β)

. Again,

π

be veried that for

as

c

∗

D(xt , χ)

ζc > τ > 0

D(xt , χ) → 0,

(10)

so that as in the previous setion, it an

the derivative is positive, while it hanges sign

tends to one. Thus, a maximum in the oupon

c

exists. Although

annot be determined analytially, we will show in the next setion, that the

optimal oupon of a CoCo bond will be higher than the optimal oupon of a

straight bond.

3

CoCos as Solution Against Banking Crises Complete Contrats

With the framework set up in the previous setion, we an now address the issue

whether a CoCo bond is an attrative alternative for banks and has the potential

to mitigate future banking rises.

We analyze this issue along two dimensions.

First, we onsider whether the use of CoCo bonds is worthwhile for bank owners.

Seond, we analyze whether the use of CoCo bonds is beneial to the eonomy

in the sense that it dereases the risk that a bank runs into nanial distress

measured by both the default probability and the osts of distress.

19 For the analysis of rating-trigger step-up bonds, Bhanot and Mello (2006) take suh an

approah. For a disussion, see also

?.

13

3.1

Inentive Compatibility

As a rst result, we show that for a given deposit volume, the bank has a higher

debt apaity if it issues CoCo bonds relative to straight bonds. In other words,

the optimal oupon of a straight bond issue is lower than the optimal oupon of

a CoCo bond. To derive this result, we establish the following laim.

For a given ash ow level x0 , deposit volume d, all admissible parameter values (i.e. 0 < µ < r, β < 0, 0 < φ, 0 < τ < 1, and λ < (1 − τ )), and

any given oupon level k suh that ξ = φ · π < xt , it holds

Lemma 1

∂ Vtc ∂ Vtb <

.

∂ b b=k

∂ c c=k

The proof is in appendix A.1.

From lemma 1, two important onlusions an

∂ Vtc

be drawn. Sine the slope

of the bank value with CoCo bond naning is

∂c

∂ Vtb

positive for a given oupon k for whih the orresponding slope

= 0 of the

∂b

bank value under straight bond naning is zero, it immediately follows that the

optimal oupon

c∗

of the CoCo bond must be larger than

b∗

of the straight bond.

Seond, the bank's rm value under the optimal oupon hoie is higher for CoCo

bonds than for straight bonds, i.e.

V b (b∗ ) < V c (c∗ ).

This inequality is a result of the fat that for

c = 0, Vtb

must equal

Vtc

sine

χ = ξ.

Thus, both rm value funtions originate in the same point. By integrating, we

obtain

hold

V b (k) < V c (k) from lemma 1 for any given oupon k

b

∗

c

∗

V (b ) < V (c )

due to

∗

∗

c >b

and therefore it must

.

Eonomially, the higher bank value is a result of the fat that bonds with a

higher oupon an be issued that reate additional tax shields. For the ase of a

CoCo bond, this advantage of debt is not ountered by the typial disadvantage

of higher expeted distress osts, beause due to the onvertibility feature, a

onversion takes plae before the bank will run into nanial distress.

As a

result, additional tax shields are reated by CoCos without inreasing the default

probability. It is worth noting, that the same qualitative result will also hold, if an

14

alternative trade-o model for debt naning is onsidered. Thus, the assumption

of a tax shield is not ruial, and ould be substituted by some other advantage

of debt naning.

3.2

Severity of Finanial Distress

From the systemi perspetive that a regulator will take on, two aspets of nanial distress are interesting. On the one hand, the severity of nanial distress

an be evaluated as the expeted (present value of ) distress osts. On the other

hand, it is also important to quantify the likelihood that a distress event will

our within a given time period. Formally, the bank enters nanial distress in

xt

our setup when the ash ow

hits the distress threshold, whih is

ase of straight bond naning and

ξc

ξb = φ · (d + b).

T

probability that the ash ow proess

x0 .

xt

hits the boundary

20

z̄ − µ̂ T

√

σ T

z̄ = log(ξ/x0 ), µ̂ = µ − σ 2 /2,

umulative distribution funtion.

immediately obvious that

Pξ,T

the default threshold

ξc = φ · d

is equivalent within our framework to the

From standard results,

Pξ,T = Prob{Tξ < T } = N

where

π = d,

The probability that the bank enters nanial

distress within a given time horizon

urrent level of

in the

for CoCo bond naning. Sine interest

payments after onversion are redued to

is lower than

ξb

from above given a

this an be alulated as

+ exp

and

ξ

N(·)

Note that

z̄

2 µ̂ z̄

σ2

N

z̄ + µ̂ T

√

σ T

,

(11)

denotes the standard normal

inreases in

ξ,

from whih it is

is monotonially inreasing in the threshold

Therefore, it follows for any time horizon

T

ξ.

that the default probability with

CoCo bond naning is smaller than the orresponding probability under straight

bond naning

Pξc ,T < Pξb ,T .

Apparently, the inequality holds for any arbitrary drift rate

µ

so that we do not

need to distinguish between the physial and risk-neutral drift rate.

As a seond measure of the severity of nanial distress, we an ompare the

expeted distress osts between straight bond and CoCo bond naning.

20 See e.g. Björk (1998), Ch. 13.

15

We

nd the same unambiguous positive eet of CoCo bonds and report details in

Appendix A.2. We summarize the ndings in this setion in

(Contingent onvertibles in a omplete ontrat setting) Under

the possibility to write omplete ontrats, CoCo bonds are inentive-ompatible

in the sense that an optimally designed bond inreases the bank's rm value and

mitigates the severity of nanial distress doumented by a lower probability of

nanial distress as well as lower present value of distress osts.

Proposition 1

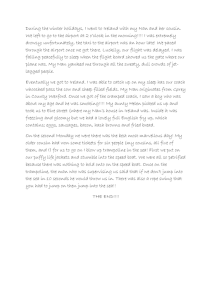

Figure 1: Bank value and distress probabilities.

b

The left panel plots the rm value for a bank with straight bonds, Vt (solid line) and with

c

CoCo bonds, Vt (dashed line) as funtion of the oupon rate c and b. The right panel plots

the probability of nanial distress Pξ,T (on log-sale) for straight bonds (solid line) and

T . Note that Pξ,T is plotted under the

physial measure, and thus represents the atual probability of default. It is alulated by

P

exploiting the relationship µ = µ − ψσ , and assuming a market prie of risk equal to ψ = 0.5.

CoCo bonds (dashed line) for inreasing time horizons

Parameter values are:

xt = 1, d = 1.5, λ = 0.55, r = 0.08, µ = 0.05, τ = 0.35, σl = 0.15.

V

Pξ,T

0.1

28

26

0.01

24

0.001

PSfrag replaements22

PSfrag replaements 10-4

20

0.2

0.4

0.6

0.8

c,b ,

1.0

2

4

6

8

10

T

10-6

As an illustration of the ndings in proposition 1, gure 1 reports numerial

values for the rm value (left panel) of a bank having issued straight bonds (solid

line) and the value of a bank using CoCo bonds (dashed line). The graph reveals

that with CoCo bonds the debt apaity of the bank is substantially higher whih

in turn leads to an inreased rm value at the optimal oupon rate. The right

panel plots the probability for nanial distress (on log-sale) for a bank with

an optimal amount of straight bonds (solid line) and for a bank with an optimal

CoCo bond (dashed line).

Again, the numerial example onrms the general

nding that for any time horizon

T,

the probability of nanial distress is lower

for banks having issued CoCo bonds.

16

4

CoCos as Origin of Banking Crises Inomplete

Contrats

The previous setion has demonstrated that CoCo bonds have substantial beneial eets on banks as well as on the banking system.

Not only do CoCo

bonds raise the bank's debt apaity whih inreases rm value, it also dereases

the probability of running into ostly nanial distress beause of the automati

impliit reapitalization mehanism. A folk wisdom in nanial eonomis is the

saying that there is no suh thing as a free lunh. So, one may wonder whether

there are really only advantages to CoCo bonds, or if there is a hidden drawbak.

On an abstrat level, a large body of theoretial literature has stressed the role of

debt ontrats as being a disiplining devie on the deision making of managers

and owners. Jensen (1986)'s free ash-ow hypothesis or the role of short-term

debt as ommitment devie stressed by Calomiris and Kahn (1991) and Diamond

and Rajan (2000, 2001) are prominent examples.

From a ontrat-theoretial

perspetive, in partiular Innes (1990) and Hart and Moore (1998) are important

ontributions whih establish the optimality of a debt ontrat. They show that

under the ondition of inomplete ontrats, a naning arrangement is optimal

where the nanier reeives a xed payment in good states of the world, while

being handed over ontrol rights in bad states of the world. This naning arrangement resembles exatly a debt ontrat. The ruial insight is the fat that

managers (or the entrepreneur) is disiplined by the threat of being expropriated

in bad states. Note that CoCo bonds undermine preisely this disiplining feature

of debt ontrats. In bad states of the world, former owners do not loose their

ontrol rights immediately. On the ontrary, former bondholders are obliged to

onvert their debt laim into an equity laim.

Arguably, absent the threat of

losing ontrol rights, owners fae dierent inentives.

In this setion, we analyze this doubt formally by assuming ontrats to be inomplete in the sense that manager-owners an hange the investment poliy, or

more preisely that the hoie of investment poliy is observable, but not ontratible.

The issuane of CoCo bonds instead of straight bonds has arguably

an important impliation for the risk taking behavior of bank manager-owners.

Intuitively, sine the bank's equity holders enjoy the full benets from a ash ow

17

inrease but are proteted against a default in a less favorable state due to the

mandatory onversion, they might prefer a more risky strategy ompared to the

ase with straight bond naning. For this reason, we introdue the problem of

risk-shifting to the bank's naning deision and evaluate both the impat on

equity holder's wealth and the severity of running into nanial distress.

4.1

Risk Taking Inentives

In this setion, we assume that bank managers have an unique option to inrease

the riskiness of the bank's operating prot. In partiular, we an think about the

risk-shifting option as the possibility of managers to hoose dierent tehnologies

suh as the bank's possibility to relax their monitoring eort or to put less resoures into an eetive risk management system (shirking) as e.g. in Deamps

et al. (2004). While these ations avoid osts and ould therefore raise (expeted)

prots, unmonitored reditors have moral hazard inentives whih inreases the

riskiness of returns.

Alternatively, with respet to their (proprietary) trading

ativities, the risk-shifting option is to be interpreted as the investment in more

risky seurities whih inreases the overall asset value risk in the sense of the lassi asset substitution problem as in Jensen and Mekling (1976), Green (1984) or

Leland (1998).

In formal terms, we assume that the urrent ash ow risk is

managers have an irreversible option to inrease risk to

purposes relevant risk-neutral) drift

µ

σh ,

σl

and that bank

while the (for priing

21

remains unaeted.

To ompute the de-

fault probability under the physial (true) probability measure, knowledge of the

physial drift

µP

physial drift via

is also required. Sine the risk-neutral drift

P

µ = µ − ψ σ,

the physial growth rate

for a given positive market prie of risk

ψ > 0.

µ

P

µ

is related to the

rises with the risk

σ

The assumption that an inrease

in risk is ompensated by a orresponding inrease in the (physial) drift rate is

22

preisely onsistent with the notion of shirking.

We abstrat from manager-owner onits whih would only add another layer of

ageny onits and assume that deisions are made in the interest of the owners.

21 This modeling approah is standard within the asset substitution literature as e.g. in Leland

(1998), Erisson (2000), and

?.

22 See e.g. Deamps et al. (2004).

18

In this setion, we analyze the inentives of equity holders to shirk, i.e. to hoose

the high risk investment program. We rst show that the nanial onstraints

are ruial to understanding risk taking inentives.

One the rm has issued the bond, equity holders have an inentive to hoose the

high risk tehnology if this inreases the value of their laim. In formal terms, the

risk preferene an be evaluated by determining the sign of the rst derivative of

the equity laim with respet to the risk parameter

derivative of the equity value

Stb

Taking the rst partial

for straight bond naning w.r.t.

σ

yields,

∂St

∂

= −V(ξ, π)

D(xt , ξ, σ)

∂σ

∂σ

∂β(σ)

xt

·

.

= −V(ξ, π) D(xt, ξ, σ) · log

ξ

∂σ

xt

> 0,

immediately obvious that D(xt , ξ, σ) > 0 and log

ξ

While it is

∂β(σ)

straightforward to show that

∂σ

depends on the rst term

V(ξ, π),

> 0.

V(ξ, π)

(12)

it is also

Therefore, the sign of the derivative

whih was dened as

V(ξ, π) = (1 − τ )

Note that

σ.

ξ

π

−

r−µ r

.

(13)

is neatly interpreted as the present value from a riskless after-

tax perpetual net inome stream given a urrent earnings level of

interest obligation

π , V(ξ, π)

for suiently high levels of

is negative as long as

ξ , V(ξ, π)

ξ

ξ.

For a given

is suiently small, while

turns out to be positive.

Eonomially, with striter nanial onstraints (i.e. with a higher boundary

ξ ),

equity holders loose a more valuable ash ow stream relative to the given debt

liabilities if default ours, whih makes them relutant to the risk of running into

nanial distress. Thus, the earlier a bank is fored into nanial reorganization,

the more severe is the negative eet for the equity value. As a result, striter

nanial onstraints are an inentive for the bank to at more prudent and to

avoid exessive risks taking. We highlight the nding as

In the ase of straight bond naning, equity holders' risk preferenes

depend on the exogenous onstraints ξ . If onstraints are suiently weak in the

sense that the threshold ξ is low, equity holders have inentives to inrease risk,

i.e. ∂St /∂σ > 0. If onstraints are strong in the sense that ξ is suiently high,

equity holders have inentives to avoid risks, i.e. ∂St /∂σ < 0.

Lemma 2

19

From (13) we an immediately derive the ritial threshold where risk preferenes

swith, i.e. where the derivative is zero,

threshold

ξˆ diretly

∂St

∂σ

= 0,

for any

xt > ξ .

This ritial

follows from (2) and satises

r−µ

ˆ

ξ(π)

=π

.

r

For any

ξ

above

ξˆ,

(14)

owners dislike higher risks, while for any

holders have inentives to inrease risk. At

ξˆ,

ξ

below

ξˆ,

equity holders are indierent with

respet to the risk strategy. In other words, the equity laim is onvex in

ξ < ξˆ,

while being onave for

ξˆ < ξ

equity

and (pieewise) linear for

xt

for

ξ = ξˆ.

Note that if the bank does not fae any exogenous onstraints, the optimal endogenous threshold an be shown to be

ξ ∗ (π) = π

r−µ β 23

.

Sine the last fration

r β−1

is always smaller than one, the endogenous threshold is always below

ξˆ whih

shows that absent any nanial onstraints, equity holders always have the usual

all option-like inentive to inrease risk.

The threshold

ξˆ

displays two intuitively reasonable harateristis.

threshold depends on the growth potential of the bank. For higher

First, the

µ, ξˆ is

lower,

thus, a bank with good growth prospets is able to raise apital for ash ow

levels where a omparable bank with a lower growth rate already faes nanial

diulties. Seond, it inreases with the interest payment

π,

whih is intuitive

sine with higher debt levels the bank is supposed to run into nanial diulties

earlier.

To gauge the impat of a CoCo bond on the risk taking behavior of banks, we

analyze how risk preferenes hange when the bank replaes the optimal straight

bond by an optimal CoCo bond. Optimal bond volumes refer to those levels,

and

c∗ ,

b∗

respetively, that maximize the bank value, whih need not neessarily

oinide with the rst-best solution that ould be obtained in a omplete ontrat

ase. From the previous setion, we know that given the onstraint

ξˆ,

the bank

owners have no inentives to inrease risk, i.e. to shirk when having issued a

straight bond. In what follows, we onsider the ritial level

ˆ

ξ(π) = ξ(π)

at whih

the bank for straight bond naning is indierent about its risk preferenes as the

nanial onstraint

ξ(π)

for the bank in order to have a meaningful omparison

for CoCo bond naning.

23 See e.g. Dixit and Pindyk (1994), Mella-Barral (1999), and Deamps et al. (2004).

20

Again, we need to alulate the rst derivative of the equity value

respet to

σ.

Stc

with

The basi idea of CoCo bonds is to provide banks with a preom-

mitted reapitalization at a time where they fae diulties in raising external

naning. In line with this reasoning, we assume the onversion to our at the

time when the external onstraint would be binding if there were no onvertibility option, i.e. at the threshold

ˆ + c).

χ = ξ(d

The onversion avoids immediate

nanial distress beause it lowers debt obligations. However, if operating prots

ontinue to deline, the bank eventually may fae nanial diulties when ash

ows deteriorate further to the lower threshold

From the denition of

χ

and by dierentiating

Stc

and

ξc ,

the terms

with respet to

ˆ .

ξc = ξ(d)

V(χ, d + c) and V(ξc , d) in (9) are zero,

σ,

we are left with

∂Stc

∂

= (1 − γ)V(χ, d)

D(xt , χ)

∂σ

∂σ

xt

∂β(σ)

·

.

= (1 − γ)V(χ, d)D(xt , χ) · log

(15)

χ

∂σ

xt

> 0 and

Again, the sign of the derivative depends on V(χ, d), sine log

χ

∂β(σ)

χ

d

>

0

. By the denition of V and χ, this equals V(χ, d) = (1−τ )

−

=

∂σ

r−µ

r

(1 − τ ) rc > 0 whih is always positive for γ < 1. Therefore, we derive the

important result that, as long as initial equity holders retain a positive fration

of ash ow rights (γ

< 1),

∂Stc

is always positive, whih means that equity holders

∂σ

always have an inentive to engage in risk-shifting ativities. We highlight this

result as

(Risk taking in inomplete ontrat setting) Suppose a bank has

ˆ + c) and ξc =

issued straight bonds and faes nanial onstraints (χ = ξ(d

ˆ ), whih leaves manager-owners indierent with respet to the risk strategy,

ξ(d)

b

t

= 0. If that bank replaes the straight bond by an optimally designed CoCo

i.e. ∂S

∂σ

bond where initial equity holders retain a positive fration of ash-ow rights,

c

t

i.e. γ < 1, manager-owners always have an inentive to inrease risk, i.e. ∂S

> 0.

∂σ

Proposition 2

The proposition shows that for the ase where exogenous nanial onstraints

are suh that

ˆ

ξ(π)

= φ̄ · π

with

φ̄ = (r − µ)/r ,

a CoCo bond for straight bond

swap leads to risk-shifting inentives. Although we onsider the ase, where the

21

bank initially has no inentives to hange its business risk as the most relevant

24

situation,

this partiular hoie does not limit the generality of the eonomi

insight in our main result in proposition 2. The next subsetion shows that the

results an be generalized to the ase of arbitrarily strit (or weak) nanial

onstraints.

Consider the general exogenous threshold

ξ = φ·π

for an arbitrary

φ > 0.

We

rst show that if the CoCo bond for straight bond swap is strutured in suh

a way that the oupon payment is kept onstant, i.e

b = c,

then a risk-shift

inreases the bank's equity value more strongly under CoCo bond naning than

under straight bond naning as indiated by the following lemma:

For any arbitrary thresholds χ = ξb and ξc with ξc < χ and for CoCo

bonds that replae straight bonds with the same oupon, i.e. b = c, a CoCo bond

inreases risk taking inentives of manager-owners, in the sense that

Lemma 3

∂Stb

∂Stc

<

.

∂σ

∂σ

The proof of lemma 3 is in the appendix. From lemma 3 together with lemma 1,

we an derive the following more general proposition about risk taking inentives

for an arbitrary onstraint and optimal debt level hoies.

(Generalization of risk taking inentives) If nanial onstraints

are weak, then the bank will always prefer the higher risk with both optimal straight

bonds as well as optimal CoCo bonds. For strong nanial onstraints, the rm

will always prefer the low risk for optimal straight bond naning, while it might

still prefer the higher risk under optimal CoCo bond naning.

In tehnial terms, for arbitrary onstraints ξ = φ · π and optimal hoie of the

b

∂Stc t ˆ, then ∂Stb ∗ < 0 and

debt level, if ξ < ξˆ, then 0 < ∂S

<

.

If

ξ

>

ξ

∗

∗

∂σ b=b

∂σ c=c

∂σ b=b

Proposition 3

∂Stc ∂σ c=c∗

≷0

The proof is in the appendix A.4.

Proposition 3 generalizes the ndings from

proposition 2 and lemma 3 to the ase of arbitrary nanial onstraints and optimal bond hoies. Importantly, the result shows that it will never be the ase

24 The argument is that the initial bank, that has disretion over its risk poliy, has already

adapted its desired risk level and is in 'equilibrium' with respet to the hoie over

22

σ.

that the bank has preferenes for the high risk under straight bond naning, but

preferenes for the low risk under CoCo bond naning.

The intuitive reason for why straight bonds impose lower risk-shifting inentives

on the equity holders than CoCo bonds is due to the wealth eet for the equity holders in partiularly poor states. In the ase of CoCo bonds outstanding,

there are poor states in whih onversion of the CoCo bonds takes plae and

the (old) equity holders still keep their valuable equity laims.

In the ase of

straight bond naning, however, the same state leads to default, in whih ase

the equity holders are left with nothing aording to absolute priority rules. As

a result, banks with CoCo bonds outstanding have a lower inentive to prevent

poor states so they are willing to aept a higher ash ow risk than the equity

25

holders for straight bond naning would be willing to aept.

This more general nding shows that the distortion of risk shifting inentives

whih are indued by a CoCo bond for straight bond swap is robust with respet

to the assumption on the exogenous nanial onstraints. This leads to an important impliation for the ase of a bank that benets from an impliit bail-out

option by the government. If a bank is onsidered to be too big to fail, and the

bank manager-owners antiipate the bail-out ommitment, they will already fae

inentives to engage in risk shifting ativities. Our result in proposition 3 show

that in suh a ase, the risk taking inentives for the bank with a CoCo bond an

even be inreased.

Taken together, proposition 2 and 3 onrm the intuition that in inomplete ontrat settings, debt serves as a disiplining devie, where the disiplining eet

stems from the threat of losing omplete ontrol rights in a bankrupty proess.

If, as in the ase of CoCo bonds, equity holders only lose ash-ow rights but

not omplete ontrol rights, the disiplining impat is mitigated, and managerowners fae distorted risk inentives. Hene, our analysis ontradits results from

25 The result is a neat analogy to the ase of regular onvertible bonds. As rst stated in Green

(1984), regular onvertible bonds an mitigate the lassi asset substitution problem (see e.g.

Jensen and Mekling, 1976), beause onversion takes plae at the disretion of bondholders

in good states. Contingent onvertible bonds are the preise polar ase, where onversion

takes plae mandatorily in poor states, and therefore it is intuitively reasonable to expet

them to aggravate the asset substitution problem.

23

Flannery (2005) who nds that shareholders onfront undistorted risk-bearing in-

26

entives.

Proposition 3 implies that we an distinguish three ases.

First, the ase

where banks with straight bonds already have risk-shifting inentives (e.g. due

to an impliit bail-out ommitment) so that swithing to a CoCo bond naning

reinfores risk inentives. Seond, the ase where banks with straight bonds have

an aversion against inreasing risks, and for whih the swith to a CoCo bond

does not result in a preferene for higher risks.

Third, the ase where banks

with straight bonds have a preferene for the low risk, but where the swith to

CoCo bonds reverses risk preferenes, i.e. where banks will engage in more risky

ativities one having issued CoCo bonds.

4.2

Impat of Distorted Risk Taking Inentives

In this setion, we analyze the impat of risk-shifting inentives on the net-wealth

of the bank, inentive ompatibility onditions and the severity of nanial distress. In partiular, we fous on the last ase identied at the end of the previous

subsetion, where CoCo bonds hange the risk taking behavior.

Sine we onsider an inomplete ontrats setting, the hoie of the risk-strategy

is observable but not ontratible.

Thus, in suh a full-information setup, in-

vestors an rationally antiipate the risk hoies of bank owners and will demand

a orresponding ompensation. This means that the bond will be pried by taking into aount the expeted hoie of the risk parameter

bond is pried by assuming

σl ,

σ.

Thus, a straight

while a CoCo bond will be pried by taking into

aount the risk-shifting inentives, i.e. by assuming

σh .

In general, it is a well

known result within this model lass that a higher risk redues the optimal rm

27

value,

beause within a trade-o model, the bank benets from advantages of

debt naning as long as it remains solvent but inurs losses when it suers from

a default. A higher business risk inreases the likelihood of a default, whih inreases the present value of the losses in the ase of a default without providing

26 See Flannery (2005), p. 12.

27 This nding has already been disussed in the basi model by Leland (1994).

24

any additional advantages.

In formal terms, it is straightforward to show that the rm value

negatively on

σ,

β

x

x

log

< 0,

ξb

ξb

(16)

where the laim follows from the repeatedly used fat that

σ.

depends

i.e.

∂Vtb

τ

= −π

∂β

r

on

Vtb

β

depends positively

A little more algebra shows that this nding arries over to the ase of

CoCo bonds. Taking the derivative yields,

∂Vtc

dτ (µ − r) + ξc r(λ − (1 − τ ))

=

∂β

r(r − µ)

β

cτ x

x

< 0.

log

r χ

χ

As

λ

is bounded above by

(1 − τ ),

and

µ < r,

β

x

x

log

−

ξc

ξc

(17)

the derivative is always negative.

In setion 3.1, we have established from lemma 1 that the optimal rm value

with CoCo bonds is always higher than with straight bonds, i.e.

V b (b∗ ) < V c (c∗ ),

if the risk-strategy is ontratible. As the bank shifts towards a more risky strategy, the bank rm value for a CoCo bond naning delines. If the risk-shifting

possibility is not severe, i.e.

σh

only slightly exeeds the initial risk

σl ,

the bank

value under CoCo naning will still be higher than under straight bond naning.

Conversely, if the risk-shifting possibility is severe, i.e.

σh

is large, the optimal

bank value will be lower than in the ase of a straight bond issue. The left panel

in gure 2 shows in line with (17) that the bank's rm value under CoCo naning,

Vtc

(dashed line), delines monotonially as its risk-shifting option is more

severe, i.e. as

σh

inreases, while the bank value under straight bond naning,

Vtb

(horizontal line), is obviously independent of

for

σh

for whih

long as

σh

Vtc

equals or exeeds

lies between the initial

merial base ase

σ̂ = 0.196),

Vtb

as

σl = 0.15

σh .

We dene a ritial value

σ̂ = sup{σh |Vtc (σh ) ≥ Vtb (σl )}.

and the ritial value

(in the nu-

the bank's rm value is higher under CoCo bond

naning. The right panel plots yield spreads (dened as

bonds and straight bonds.

σ̂

As

c∗ /Ct − r )

for CoCo

While the spread for a straight bond (depited as

horizontal dashed line) is only 50 basispoints, it is substantially higher for CoCo

bonds. Even if bank managers do not engage in risk shifting, the yield spread

25

Figure 2: Bank value and yield spreads

c

The left panel plots the dierene between the bank rm value with CoCo bonds, Vt and the

b

b

c

b

b

bank rm value with straight bonds, Vt , as a perentage of Vt i.e. ∆V% = (Vt − Vt )/Vt . The

horizontal line indiates the ritial level

σ̂

for whih the dierene is zero. The right panel

plots yield spreads in basispoints for straight bonds (horizontal solid line) versus spreads of

CoCo bonds (dashed line). Parameter values are:

xt = 1, d = 1.5, λ = 0.55, r = 0.08, µ = 0.05,

τ = 0.35, σl = 0.15, γ = 0.4.

ys

∆V%

700

σ̂

0.04

500

0.02

PSfrag replaements-0.02

600

400

0.16

0.18

σh300

0.20

0.22

0.24

PSfrag replaements200

100

-0.04

0.16

-0.06

0.18

0.20

0.22

0.24

σh

amounts to 325 basispoints. The spread rises with the risk shifting opportunity,

and bond investors demand a spread of 524 basispoints if the bank has inentives

to raise the risk to

σh = 0.20.

The substantially higher spreads are roughly in

line with evidene from the industry where CoCo bonds are expeted to trade up

28

to an additional 300 basispoints interest margin.

The higher spreads are due

to two fators. On the one hand, a bank with CoCo bonds has a higher leverage,

and on the other hand, CoCo bondholders demand an additional premium for

the fat that onversion mandatorily takes plae at a time when equity values are

low. Thus, the higher spreads partly reet this insurane premium.

Two points about the results are noteworthy: First, despite the fat that CoCo

bond naning is assoiated with a higher risk

σh , the overall bank value an still

be higher relative to the ase of straight bond naning. The reason for the value

inrease lies in the relaxation of nanial onstraints (i.e. a lower default barrier)

whih inreases the bank's debt apaity and enables the bank to exploit debt

advantages to a larger extent. In our setup, the bank is able to generate a higher

instantaneous tax shield. Note that the value inrease due to higher tax shields

is at the expense of the tax authority, whih in turn reeives less taxes.

Seond, although CoCo bonds inrease the bank rm value via a higher debt a28 See

Finanial Times UK experiment raises prospets of new asset lass, November 5, 2009.

26

paity, bond investors demand a substantially higher spread whih inreases with

the riskiness of the asset value.

Spreads are high beause by onstrution the

onversion of CoCo bonds takes plae at a time when onversion is not favorable

from the perspetive of investors, i.e. CoCo bond investors obtain a fration of

the equity laim preisely in states where equity values are low. Our ndings are

an important warning signal against arguments as e.g. mentioned in Flannery

(2005, 2009) that the internalization of risk-taking osts will deter banks from

taking too muh risk. Our results show that although banks bear the osts of

risk-taking via substantially higher spreads, they an still have an inentive to

engage in risk-shifting ativities.

The nding that a CoCo bond issue for

σh < σ̂

results in a higher overall

bank rm value implies that equity holders obtain a higher wealth by issuing

CoCo bonds.

Our analysis demonstrates the important insight that although

reditors antiipate a potential risk-shift so that they pay a fair prie for the

investment, owners are still better o. As a result, from an investors' perspetive,

CoCos are a Pareto improvement beause no investor suers and some obtain a

stritly higher wealth.

However, it is important to stress that although from the perspetive of the bank

CoCo bonds are Pareto-optimal, it is a priori not lear whether the use of CoCo

bonds is also desirable from a systemi point of view. To evaluate the systemi

eet of CoCo bonds, we onsider the probability of nanial distress for the

banking system in the following paragraph.

As in setion 3.2, we ompute the bank's probability of running into nanial

distress.

To ompare a bank with straight bonds to a bank with CoCo bonds,

not only the threshold

parameter

σ.

ξ

diers but, ontrary to the previous setion also the risk

Furthermore, from the denition of the risk-shift, we assume that

the risk-neutral drift remains onstant. Thus, as a result of the inreasing risk,

the physial drift rate inreases as well.

4.1 that the physial drift rate

µP

Reall from the disussion in setion

is related to

σ

by

µP = µ − ψ σ .

the atual inrease depends on the market prie of risk

fators, we extend the notation and write

27

Pξ,σ,T .

ψ.

Therefore,

To aount for these

Further, to ease interpretation,

we report the dierene in distress probabilities,

time horizon

T

between a bank with CoCo bonds and risk

Sine

for

∆PT

σh ,

σh = σl ,

σh

over a

and a bank with

σl .

straight bonds and risk

Note that for

∆PT = Pξc ,σh ,T − Pξb ,σl ,T

we know from proposition 1 that

inreases monotonially in

σh

∆PT

must be negative.

to a positive value, there is a value

for whih probabilities of nanial distress oinide. Therefore, we dene

another ritial value

non-negative, i.e.

σ̄

as the smallest value of

σh

for whih the dierene is

σ̄ = inf{σh |Pξc ,σh ,T ≥ Pξb ,σl ,T }.

Numerial results for the base ase senario are reported in the left panel of gure

3.

Figure 3: Probability of nanial distress.

The left panel plots the dierene in distress probabilities of a bank with CoCo bonds and

∆PT = Pξc ,σh ,T − Pξb ,σl ,T , for T

The right panel plots the ritial values

straight bonds, i.e.

of

ψ = 0.5.

Parameter values are:

= 10 years and a market prie of risk

σ̂ and σ̄ for dierent time horizons T .

xt = 1, d = 1.5, λ = 0.55, r = 0.08, µ = 0.05, τ = 0.35, σl = 0.15.

σh

∆PT

0.22

0.21

σ̂

σ̄

0.08

σ̂

0.20

0.06

0.19

0.04

0.18

PSfrag replaements

0.17

PSfrag replaements0.02

0.16

0.18

0.20

0.22

0.24

σ̄

σh

10

20

30

40

50

T

The graph onrms the general insight from setion 3.2, that CoCo bonds are

beneial in terms of probability of distress

as long as

over the hoie of the risk tehnology, i.e. for

the bank has no disretion

σh = σl .

However, if ontrats

are inomplete, and the bank has disretion to inrease the investment risk

σh ,

distress probabilities inrease with the severity of the risk-shift, and outweigh

the initially beneial eets. The ritial value

σ̄

above whih CoCo bonds are

detrimental in terms of probability of nanial distress turns out to be

(for a time horizon of

line. For

σh

T = 10

larger than

σ̄ ,

σ̄ = 0.183

years), whih is indiated as the vertial dashed

a bank with CoCo bond naning will atually have a

higher probability of nanial distress. The graphi also shows the ritial value

28

σ̂

up to whih CoCo bonds are rm value-inreasing as the vertial solid line.

From omparing the ritial values

σ̄

and

σ̂ ,

we obtain the important existene

result, that ases are possible for whih we nd

σ̂ .

In other words, there exist risk levels

σh

σ̄

to be stritly smaller than

whih the bank an hoose, for

whih CoCo bonds are an ex ante optimal strategy for the bank in terms of value

maximization, but for whih the probability of nanial distress is higher relative

to the ase of straight bond naning. The right panel in gure 3 plots the ritial

values

σ̄

and

σ̂

for dierent time horizons

T

and shows that the existene of suh

a onstellation is robust over longer time horizons. Furthermore in appendix A.2,

we show that we obtain the same qualitative result if we onsider the expeted

present value of distress osts as a seond measure for the severity of default.

The numerial analysis thus demonstrates the potentially adverse impat of CoCo

bond naning, whih we summarize as

(Wealth of investors versus banking stability) Suppose nanial

onstraints are suh that a bank with straight bonds hooses the low-risk tehnology

σl (the bank monitors), while a bank with CoCo bonds has inentives to hoose

the high-risk strategy σh (the bank shirks). Suppose further that bond investors

rationally antiipate distorted risk taking inentives and obtain a orresponding

ompensation. Then, it an be possible that a bank with CoCo bond naning

obtains a higher bank value, while the probability of nanial distress is higher

than for optimal straight bond naning.

Proposition 4

The intuition for proposition 4 an be explained in terms of a trade-o. On

the one hand, CoCo bonds are beneial in the sense that they relax the nanial

onstraints (i.e. lower the default barrier

ξc ),

whih allows the bank to exploit

debt naning advantages to a larger extent. Therefore, the bank value inreases

relative to the ase of straight bond naning. On the other hand, from propositions 2 and 3, we know that CoCo bond naning indues the inentive to

inrease the ash ow risk. Although the default barrier is lower in the ase of

CoCo bonds, the probability, that the more volatile ash ow proess hits the

default barrier, an atually inrease. Intuitively, the higher ash ow volatility

overompensates the relaxation of nanial onstraints.

Proposition 4 highlights a potentially dangerous adverse impliation of CoCo

29

bond naning and ontrasts with the main results in e.g. Flannery (2005, 2009)

and Landier and Ueda (2009). The reasoning in these papers relies on a stati

analysis and basially resembles our results for omplete ontrats.

Flannery

(2005, 2009) and Landier and Ueda (2009) stress the potential benets of CoCo

bonds in terms of the relaxation of nanial onstraints, i.e. the redution in the

probability of nanial distress.

Although in partiular Flannery (2005, 2009)

also reognizes the potential risk-taking inentives, he onludes that this is not

a drawbak of CoCo bonds, sine CoCo bond holders will antiipate distorted

risk preferenes and demand a higher premium. Sine the bank has to internalize

risk-taking osts, this will ontrol the risk-shift. In ontrast, we show that this

reasoning does not need to be true in general. Our results suggest that although

the bank internalizes risk-taking osts, it an still be optimal for manager-owners

to inrease risk. More importantly, the risk-shift an be suh that it overompensates the redution in the default threshold, whih atually inreases the probability of nanial distress relative to straight bond naning.

Thus, ontrary

to the previous work on CoCo bonds, our results demonstrate that CoCo bonds

an reate negative externalities for the eonomy, and that individually rational

deisions may have systemially undesirable outomes.

Although the nding in proposition 4 is to be understood as an existene

result, whih issues an important warning signal against the euphori use of

CoCo bonds, we argue that it is also found to hold for a substantial range of

parameter values by providing robustness results in Appendix A.5. Thereby, we

fous on two ruial parameters whih might have a signiant impat on results:

The market prie of risk and the fration of total liabilities replaed by CoCo

bonds.

4.3

Inentive-ompatible onversion trigger

In this setion, we disuss a potential solution to regulate the moral hazard

problem inherent in CoCo bonds. From the results established in lemma 2, we

know that the severity of exogenous onstraints ontrols the risk-taking inentives

of manager-owners. Striter onstraints (in the sense of higher thresholds) indue

30

manager-owners to at more prudently, sine they fae the risk of loosing a more

valuable laim.

In this subsetion, we aim at designing the CoCo bond that

does not provide risk-shifting inentives.