Fundamentals of Intermediate Accounting

Weygandt, Kieso and Warfield

Chapter 17:

Additional Reporting

Issues

Prepared by

Bonnie Harrison, College of Southern Maryland

LaPlata, Maryland

1

Chapter 17

Additional Reporting Issues

1

2

3

4

After studying this chapter, you should be able to:

Describe various accounting changes.

Understand how to account for cumulative-effect

accounting changes.

Understand how to account for retroactive

accounting changes.

Describe the accounting for changes of estimates.

2

Chapter 17

Additional Reporting Issues

After studying this chapter, you should be able to:

5 Describe the accounting for correction of errors.

6 Compute earnings per share in a simple capital

structure.

7 Compute earnings per share in a complex capital

structure.

3

Types of Accounting Changes

The types of accounting changes are:

Changes in Accounting Principle

Changes in Accounting Estimates

Errors in Financial Statements

4

Changes in Accounting Principle

A change in principle involves a change

from one generally accepted principle to

another

A change in principle does not result from

the adoption of a new accounting principle

A change to a generally accepted principle

(from an incorrect principle) is a correction

of an error

5

Changes in Accounting Principle

Changes in accounting principle are classified

into:

Cumulative-effect type of accounting

change

Retroactive-effect type of accounting

change

Change to the LIFO method of inventory

6

Cumulative-Effect Type of Accounting

Change

The catch up method should be used to account

for these changes

Financial statements for prior periods are not

restated

For all prior periods, the following items are

shown on an as-if basis (as if the new principle

had been applied):

income before extraordinary items

net income

7

Cumulative-Effect Type of Accounting

Change

The adjusting entry is effective as of the

beginning of the year

Pro forma information is shown only as

supplementary information

Such information may be reported:

1)

in the income statement

2)

in a separate schedule

3)

in the notes to the financial statements

8

Cumulative Effect: Example

• XYZ company changes from the sum-of-theyears’ digits method to the straight line method of

depreciation.

• The depreciation amounts are:

Year

SYD

ST.LINE

2002

$15,000

$8,000

2003

$14,000

$8,000

• The company’s tax rate is 40%

• Record the change as of the beginning of 2004

9

Cumulative Effect: Example

• Year

SYD

• 2002

• 2003

$15,000

$14,000

SL

Diff

Tax

Effect

$8,000 $7,000 $2,800

$8,000 $6,000 $2,400

-------- -------$13,000 $5,200

-------- --------

• Tax effect is the difference times the tax rate

10

Cumulative Effect: Example

•

•

Journal Entry:

Accumulated Depreciation $13,000

Deferred Tax Asset

$5,200

Cumulative Effect of

Change in Principle

$7,800

1) The debit to accumulated depreciation is the

excess of SYD over the straight line basis

2) The credit to Cumulative Effect is the income

effect (net of tax effect)

11

Income Statement Presentation

The following information must be presented in

whole dollar amounts and as per share amounts:

o Income before Extraordinary Item

and Cumulative Effect of Change :$ XXX

o Extraordinary Item (Net of Tax)

:$ XX

o Cumulative Effect on Prior Years

of Retroactive Application

:$ XX

o Net Income

:$ XX

12

Retroactive-Effect Type of Accounting Change

The cumulative effect of the new method at the

beginning of the period is determined

Prior period statements are recast based on the

new principle

Any cumulative effect of prior periods is adjusted

to the beginning retained earnings balance

13

Retroactive-Effect Type of Accounting Change

The five situations requiring restatement of all prior period

statements are:

1. A change from the LIFO inventory method to another

method

2. A change in the method of accounting for long term

construction type contracts

3. A change from or to the full cost method in extractive

industries

4. Issue of financials to obtain first time financing

5. A pronouncement recommending retroactive adjustment

14

Retained Earnings Presentation

• Retained Earnings account is shown as follows:

• Balance at beginning of year

• Adjustment for the Cumulative

Effect on Prior Years

• Balance at beginning (as adjusted)

• Net Income

• Balance at end of year

:$ XXX

:$ XX

:$ XX

:$ XXX

:$ XXX

15

Reporting a Change in Estimate

Changes in estimates are accounted for on a prospective

basis

Such changes are viewed as normal, recurrent adjustments

When uncertainty exists as to whether a change in

principle or a change in estimate has occurred:

•

the change should be treated as a change in estimate

Estimates that are later determined to be incorrect should

be corrected as changes in estimates

Examples of changes in estimates involve:

• inventory obsolescence; salvage values of assets,

uncollectible receivables, liability for warranties and taxes

16

When is a Change in Accounting Principle Appropriate?

Changes are appropriate when the changed

principle is preferable to the existing accounting

principle

The changed principle should result in improved

financial reporting

A change is considered preferable if a FASB

standard:

creates a new accounting principle, or

expresses preference for a new principle, or

rejects a specific accounting principle

17

Reporting the Correction of an Error

Corrections are treated as prior period adjustments to

retained earnings for the earliest period being reported

Examples of accounting errors are:

1) A change from an accounting principle that is not

generally accepted to one that is accepted

2) Mathematical errors

3) Changes in estimates that were not prepared in good

faith

4) A failure to properly accrue or defer expenses or

revenues

5) A misapplication or omission of relevant facts

6) Incorrect classification of cost as expense or asset

18

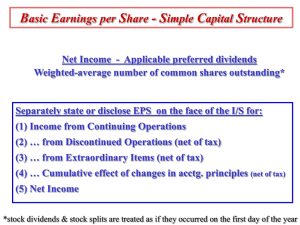

Earnings Per Share

EPS indicates the income earned by each share of

common stock.

Reported only for common stock.

Dilution of EPS means reduction in EPS.

Reduction in EPS results from potential conversion

of dilutive securities into common stock.

Shareholders want to know the extent of reduction in

EPS, if dilution takes place.

19

E.P.S

• BASIC E.P.S:

NET INCOME - PREFERRED DIVIDEND

------------------------------------------------------------WEIGHT.AVERAGE OUTSTANDING.

COMMON SHARES

20

Basic EPS Computations: Example

Given:

Jan 1: 500,000 shares outstanding.

May 1: Issued 84,000 shares.

Sept 1: Reacquired 42,000 shares.

Nov 1: Issued 36,000 shares.

N.Inc [to common stock]: $654,000.

Determine the earnings per share.

21

Basic EPS Computations: Example

Jan 1:

May:

Sept 1:

Nov 1:

500,000 *

584,000 *

542,000 *

578,000 *

Total W.Avg.shares

4/12

4/12

2/12

2/12

=

=

=

=

166,667

194,666

90,333

96,334

548,000

Earnings per Share = $654,000 / 548,000 shares

= $1.19

22

Stock Dividends and Splits

Stock dividends and stock splits require restatement

of weighted shares outstanding before the dividend

or split.

Stock dividends or splits during the year are deemed

to have been outstanding since the beginning of

the year.

Stock dividends or splits after end of the year but

before issue of the financials are likewise deemed to

be outstanding since the beginning of the year.

23

What is “DILUTION?”

• “DILUTION” is the reduction in E.P.S, if:

securities, potentially convertible into

common stock, are converted [assumed

at beginning of the year].

• Two EPS amounts are important:

Basic and Diluted

24

Complex Capital Structures

• Complex structures have convertible

securities, options, warrants, or other rights

that reduce earnings per share.

• Only securities that reduce earnings per

share (dilutive) are considered.

• Securities that increase earnings per share

(antidilutive) are ignored.

25

Diluted Earnings per Share: Methods

• The dilutive effect of convertible securities is

measured by the if-converted method

• The dilutive effect of options and warrants is

measured by the treasury stock method

• For computing dilution, the rate of conversion

most advantageous to the security holder is

used (maximum dilutive conversion rate)

26

The If-Converted Method

• The conversion of the securities into common

stock is assumed to occur at the beginning of

the year

• The related interest effect (net of tax) is

removed from net income

• The weighted average number of shares is

increased by the additional common shares

assumed issued (at the beginning)

27

The Treasury Stock Method

Options and warrants (and their equivalents) are

included in EPS computations

Options and warrants are assumed exercised at the

beginning of the year

The proceeds from the exercise of options are

assumed used to buy back common shares

The exercise price per share must be less than the

market price per share for dilution to occur

28

Options and Warrants:

Treasury Stock Method

Given:

Exercise price of an option :

[for one share of stock]

Market price of one share

at Exercise date:

Options deemed exercised:

$ 10

$ 40

1,000

Compute the number of weighted shares for determining

diluted earnings per share

29

Options and Warrants:

Treasury Stock Method

Total proceeds from exercise:

$10,000

Shares assumed issued upon exercise: 1,000

Assumed reacquisition of shares:

250

DILUTION: 1,000 - 250 = 750 SHARES

(increase in outstanding shares)

30

Earnings per Share: Simple Capital

Structures - Summary

1

2

Single Presentation of EPS

Net Income less Preferred Dividends

3 Weighted Average Number of Common Shares Outstanding

4

EPS = Result in Step 2

Result in Step 3

31

Earnings per Share: Complex Structures Summary

Dual EPS Presentation

Basic EPS

Net Income adjusted for interest

(net of tax) and preferred dividends

-----------------------------------------Weighted average number of

common shares assuming maximum

dilution

Diluted EPS

Dilutive Convertibles

Dilutive Options and

Warrants

Dilutive Contingent

Issues

32

COPYRIGHT

Copyright © 2003 John Wiley & Sons, Inc. All rights

reserved. Reproduction or translation of this work beyond

that named in Section 117 of the 1976 United States

Copyright Act without the express written consent of the

copyright owner is unlawful. Request for further information

should be addressed to the Permissions Department, John

Wiley & Sons, Inc. The purchaser may make back-up copies

for his/her own use only and not for distribution or resale.

The Publisher assumes no responsibility for errors,

omissions, or damages, caused by the use of these

programs or from the use of the information contained herein.

33