Financial Models and Cost - Benefit

advertisement

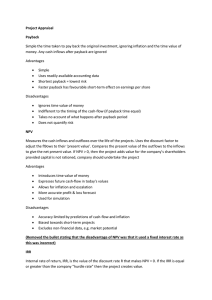

Introduction to Financial Management ES3D4 / ES4D5 Construction Management 1 Easter Revision guide based on analysis of Past Papers for ES3D4 and ES4D5 2010 2011 Concrete pressure (lectures 29 and 30 by Paul Markham) Q1 Q1 Waste management (lectures 23 & 24 by Martin Fairlie, chapter 5 in Operations Management for Construction by Chris March) Q2 Q2 Safety regulation in the context of CDM (lectures 17 to 19 by Martin Fairlie, chapter 4 in Operations Management for Construction by Chris March) Q3 Q3 Project appraisal - whole life costs and Net Present Value (lectures 26 to 28 by Karen Bradbury) Q4 Types of procurement contract (lectures 9 and 10 by George Webb) Q4 2011-12 Surveying added (lectures 1 to 4 by Tony Price & Nicki Meads) Equipment productivity and selection Q5 ES4D5 only – project management networks Q6 Q5 ES3D4 / ES4D5 Construction Management 2 Project Appraisal Financial Models Comparing the value of different contracts Choosing new equipment ES3D4 / ES4D5 Construction Management 3 Financial Models for Project Selection • • • • Payback period Return on investment (ROI) Net present value (NPV) Internal rate of return (IRR) • All these techniques are limited because they rely on forecasted cash-flow. ES3D4 / ES4D5 Construction Management 4 Payback Period • The time taken to gain a financial return = the original investment. Year Cash-flow m/c A Cash-flow m/c B 0 (£35, 000) (£35, 000) 1 £20, 000 £10, 000 2 £15, 000 £10, 000 3 £10, 000 £15, 000 4 £10, 000 £20, 000 Payback period 2 Years 3 years ES3D4 / ES4D5 Construction Management 5 Payback Period cont. Advantages • Simple • Uses readily available accounting data • Shortest payback = lowest risk • Faster payback has favourable short-term effect on earnings per share Disadvantages • Ignores time value of money • Indifferent to the timing of the cash-flow (if payback time equal) • Takes no account of what happens after payback period • Does not quantify risk ES3D4 / ES4D5 Construction Management 6 Return on Investment Average Annual Profit ROI % Original Investment AAP (Total gains) (Total outlay ) Number of years Year Cash-flow m/c A Cash-flow m/c B 0 (£35, 000) (£35, 000) 1 £20, 000 £10, 000 2 £15, 000 £10, 000 3 £10, 000 £15, 000 4 £10, 000 £20, 000 Total gains £55, 000 £55, 000 AAP 20000 £5000 4 ROI 5000 14% 35000 For both ES3D4 / ES4D5 Construction Management 7 Compound growth • Invest £1 today at interest rate of 10%per annum, compounded annually Time (T) 1 2 3 Value after T years £1 x (1+0.10) = £1.10 £1 x (1+0.10)2 = £1.21 £1 x (1+0.10)3 = £1.33 • In general, £1 invested today for T years at R% per annum, compounded annually, will grow to: £1 1 R 100 T ES3D4 / ES4D5 Construction Management 8 Discount Factors and Present Value • Conversely, in order to end up with £1 at the end of T years, today we need invest only: £1 1 T 1 R 100 • This is the present value of £1 that we expect to receive T years from now ES3D4 / ES4D5 Construction Management 9 Discount Factors and Present Value cont. • The discount factor that multiplies £1 in the above expression reflects the time value of money – £1 expected T years from now is not as valuable as £1 for sure today – if we had £1 today, we could invest it for T years at R% per annum • the interest forgone is the opportunity cost of having to wait T years to receive £1 ES3D4 / ES4D5 Construction Management 10 Discounted Cash Flows cont. • Present value of expected future cash flows: PV 20000 15000 2 10000 3 10000 4 A 1 0.10 1 0.10 1 0.10 1 0.10 PV 10000 10000 2 15000 3 20000 4 B 1 0.10 1 0.10 1 0.10 1 0.10 assuming company’s cost of capital = 10% per annum ES3D4 / ES4D5 Construction Management 11 Net Present Value • In return for some initial investment I, a typical capital project is expected to generate a stream of future cash flows Ct , t = 1, 2, … T C1 C2 C3 CT … 1 2 3 T I • Net Present Value of project equals: C3 C1 C2 CT NPV I T 2 3 1 R 1 R 1 R 1 R ES3D4 / ES4D5 Construction Management 12 Net Present Value cont. • If NPV > 0, then the project adds value for the company’s shareholders – provided capital is not rationed, company should undertake the project ES3D4 / ES4D5 Construction Management 13 Year Cash-flow m/c A Discount factor PV 0 (£35, 000) 0 (£35, 000) 1 £20, 000 0.9091 £18, 182 2 £15, 000 0.8264 £12, 396 3 £10, 000 0.7513 £7, 513 4 £10, 000 0.6830 £6, 830 Total NPV £9, 921 Year Cash-flow m/c B Discount factor PV 0 (£35, 000) 0 (£35, 000) 1 £10, 000 0.9091 £9, 091 2 £10, 000 0.8264 £8, 264 3 £15, 000 0.7513 £11, 270 4 £20, 000 0.6830 £13, 660 Total NPV £7, 285 ES3D4 / ES4D5 Construction Management 14 Net Present Value cont. Advantages • Introduces time value of money • Expresses future cashflow in today’s values • Allows for inflation and escalation • More accurate profit & loss forecast • Used for simulation Disadvantages • Accuracy limited by predictions of cash-flow and inflation • Biased towards shortterm projects • Excludes non-financial data, e.g. market potential ES3D4 / ES4D5 Construction Management 15 Hurdle Rate • The hurdle rate for a project is the minimum rate of return that the providers of the firm’s capital require from the investment • Also known as opportunity cost of capital – how much providers of firm’s capital could earn from investing the money instead in a well-diversified portfolio of financial securities of same risk as project ES3D4 / ES4D5 Construction Management 16 Hurdle Rate cont. Alternative definition: “The required rate of return in a discounted cash flow analysis, above which an investment makes sense and below which it does not. Often, this is based on the firm's cost of capital or weighted average cost of capital, plus or minus a risk premium to reflect the project's specific risk characteristics. “ www.investorwords.com/2362/hurdle_rate.html ES3D4 / ES4D5 Construction Management 17 Hurdle Rate cont. • Hurdle rate is provided by financial markets: Hurdle Rate Market Risk-free Return Market Risk Premium Risk i.e. the greater the risk the higher the required rate of return. ES3D4 / ES4D5 Construction Management 18 Internal Rate of Return • Internal rate of return, IRR, is the value of the discount rate R that makes NPV = 0 • If a project is expected to generate a stream of positive future cash flows in return for some initial investment I, then graph of NPV vs. R looks like: ES3D4 / ES4D5 Construction Management 19 Internal Rate of Return cont. • The “NPV > 0” rule for accepting capital projects is then equivalent to the rule: IRR hurdle rate ES3D4 / ES4D5 Construction Management 20 Year Cash-flow m/c A Discount factor 24% PV 0 (£35, 000) 0 (£35, 000) 1 £20, 000 0.8065 £16, 130 2 £15, 000 0.6504 £9, 756 3 £10, 000 0.5245 £5, 245 4 £10, 000 0.4230 £4, 230 Total NPV £361 Year Cash-flow m/c A Discount factor 25% PV 0 (£35, 000) 0 (£35, 000) 1 £20, 000 0.8000 £16, 000 2 £15, 000 0. 6400 £9, 600 3 £10, 000 0.5120 £5, 120 4 £10, 000 0.4096 £4, 096 Total NPV (£184) Therefore 24% <IRR<25% (for m/c B 18% <IRR<19% not shown) ES3D4 / ES4D5 Construction Management 21 • Net present value (NPV) is when we subtract initial investment from present value of cash flow – Positive NPV means that the project created value • Internal rate of return (IRR) is the discount rate that makes NPV zero – If the IRR is equal or greater than the company “hurdle rate” then the project creates value • Payback period is the time it takes to cover the investment • Return on investment measures the profitability of an investment Massood Samii, MIT OpenCourseWare Summary ES3D4 / ES4D5 Construction Management 22 Meehan corp. is a civil engineering company with annual revenue of £8 billion per year. The company is a multinational with operation in Latin America and South East Asia. Meehan was established in 1962, and since then it has experienced a high rate of growth. The company is involved in infrastructure development, commercial property development and oil exploration and development. The company is currently considering whether or not to accept a road construction project. Massood Samii, MIT OpenCourseWare Example ES3D4 / ES4D5 Construction Management 23 Meehan has collected the following information about the project; which will take four years to complete and Meehan must initially invest about £64 million on equipment and £26 million on buying the necessary property, for a total of £90 million. The annual operation cost is £20 million a year, which includes labour cost, and other operational costs. The company uses straight line 8 years depreciation. The salvage value of equipment is calculated as the cost. The tax rate is 34%. Massood Samii, MIT OpenCourseWare Example cont. ES3D4 / ES4D5 Construction Management 24 The contract calls for payment of £32 million at the end of each of first three years and £100 million upon completion at the end of the four year period. The project will commence in January 2010. Therefore all initial expenses such as purchase of land and equipment must take place prior to the start of the project. However, operational revenue and costs are calculated for the end of each subsequent year. • Should Meehan accept this project, if the discount rate is 10%? • What if Meehan used 8% discount rate? • What if Meehan needed a £5 million working capital that it would recapture at the end of the project? Massood Samii, MIT OpenCourseWare Example cont. ES3D4 / ES4D5 Construction Management 25 Massood Samii, MIT OpenCourseWare £ million ES3D4 / ES4D5 Construction Management 26 Massood Samii, MIT OpenCourseWare £ million ES3D4 / ES4D5 Construction Management 27 Exam Question 4, 2010 – Whole Life Cost Type A Windows Type B Windows • £900,000 to install • £20,000 to decorate every 5 years • Replace after 25 years for £1,200,000 • £1,250,000 to install • Repair at 20 years and 40 years for £300,000 each time Discount factor at 4% 0 yrs = 1, 5 = 0.8219, 10 = 0.6756, 15 = 0.5553, 20 = 0.4564, 25 = 0.3751, 30 = 0.3083, 35 = 0.2534, 40 = 0.2083, 45 = 0.1712 ES3D4 / ES4D5 Construction Management 28 Recommend which windows and what factors might influence the decision? ES3D4 / ES4D5 Construction Management 29 Which to use; IRR or NPV? • Why not all? • Accountants prefer NPV to IRR because the interest rate can be varied with NPV • NPV is a measure of profitability based on the transaction • IRR is a measure of profitability established by the capital markets (hurdle) • In a capital drought use NPV because the fundamental objective of financial analysis is to maximise the PV of the company’s investment portfolio. ES3D4 / ES4D5 Construction Management 30 Determining the Discount Rate C1 C2 C3 CT … 0 1 2 3 … T C3 C1 C2 CT PV T 1 R 1 R 2 1 R 3 1 R But … how do we determine the discount rate R? ES3D4 / ES4D5 Construction Management 31 Discount Rate • Discount rate R is the opportunity cost of capital – i.e. return that investors could obtain for themselves by investing instead in a well-diversified portfolio of financial securities with same level of risk as project • What do we mean by “risk”, and how do we measure it? • How do we adjust discount rate R for risk? • Financial markets provide the answer – highly efficient at pricing securities – only risk that cannot be diversified is rewarded by financial markets with additional return ES3D4 / ES4D5 Construction Management 32 What determines the discount rate R? Where: R is the discount rate Rf the risk free interest rate. Normally government bond Ri Rate of inflation. It is measured by either by consumer price index or GDP deflator. Rr Risk factor consisting of market risk, industry risk, firm specific risk and project risk Example: If risk free interest is 5%, inflation 3% then nominal rate of interest is 8%. In addition if we add 5% risk premium then our discount rate is 13% Later we argue that weighted average cost of capital would make a good indicator for discount rate Massood Samii, MIT OpenCourseWare R = Rf + Ri + Rr ES3D4 / ES4D5 Construction Management 33 Beta “A quantitative measure of the volatility of a given stock, mutual fund, or portfolio, relative to the overall market. Specifically, the performance the stock, fund or portfolio has experienced in the last 5 years as the market moved 1% up or down. A beta above 1 is more volatile than the overall market, while a beta below 1 is less volatile.” www.investorwords.com/4378/SP_500.html ES3D4 / ES4D5 Construction Management 34 Beta cont. • Required return on any asset (or portfolio of assets) reflects the component of risk that cannot be diversified away i.e. the risk that is related to the economy as a whole – this component of risk is known as systematic risk • Systematic risk is measured by the beta of the asset (or portfolio of assets) – beta of market portfolio equals 1 • So … in order to determine the rate of return required of an investment, we need to be able to estimate the beta of that asset ES3D4 / ES4D5 Construction Management 35 Securities Market Line cont. • The risk-free rate RF is the return that we expect from investing in an asset that has no risk – e.g. short-dated Treasury bills issued on behalf of UK or US Government • The market risk premium E[RM]-RF is the extra return that we expect from investing in a well-diversified portfolio that tracks the market – by definition, this portfolio has a beta of 1 ES3D4 / ES4D5 Construction Management 36 Capital Asset Pricing Model • The Securities Market Line is the graph of the Capital Asset Pricing Model (CAPM) • In words, the CAPM says that: Expected return on asset i risk - free rate (beta of asset i) (market risk premium) ES3D4 / ES4D5 Construction Management 37 Cost of Equity vs. Cost of Debt • Most companies are financed partly by – equity (owned by shareholders) – debt (owned by lenders) • In general, equity is more risky than debt – interest payments on debt must be paid, whereas dividends can be cut or not paid • As a result, shareholders demand a higher rate of return from their investment than do lenders – cost of equity is higher than cost of debt ES3D4 / ES4D5 Construction Management 38 Cost of Equity vs. Cost of Debt cont. • Weighted Average Cost of Capital (WACC) reflects the split (by market value) in company’s financing: WACC (proportion of debt) (cost of debt) (proportion of equity) (cost of equity) or in symbols: WACC D E[R ] E E[R ] D E D E D E ES3D4 / ES4D5 Construction Management 39 WACC • WACC represents the overall return on the firm’s assets required by providers of capital • WACC provides a benchmark – return required on “average risk” project undertaken by company • Need to use a higher (lower) rate to discount cash flows from projects of higher (lower) risk than “average-risk” project ES3D4 / ES4D5 Construction Management 40 Summary • Time value of money – expected future cash flow of £1 T years from now is not as valuable as receiving £1 for certain now – present value of expected future cash flow is obtained by multiplying cash flow by discount factor 1/(1+R)T • Discount factor reflects both timing and risk of expected future cash flow – the higher the risk, the greater is discount rate R ES3D4 / ES4D5 Construction Management 41 Summary cont. • Net Present Value, NPV, of stream of expected future cash flows equals the sum of the present values of individual expected future cash flows, net of initial investment I • If capital is not rationed, company should accept all capital projects with NPV > 0 – if capital is rationed, company should rank projects according to profitability index NPV/I • Internal rate of return IRR is the value of the discount rate R that makes NPV = 0 – break-even rate ES3D4 / ES4D5 Construction Management 42 Summary cont. • Cost of capital is rate of return required by providers of finance – shareholders expect to earn cost of equity on their shareholdings – lenders expect to earn cost of debt on their loans • CAPM quantifies the relationship between expected (or required) return and (systematic) risk for any asset (or portfolio of assets): E[Ri ] RF bi (E[RM ] RF ) where systematic risk is measured by asset’s beta bi ES3D4 / ES4D5 Construction Management 43 Summary cont. • WACC is weighted average of cost of debt and cost of equity – weights equal the proportions (by market value) of equity and debt financing in the company’s capital structure • WACC is a key input to corporate financial decision-making – return on firm’s assets required on average by providers of capital – reflects overall risk level of firm’s operations ES3D4 / ES4D5 Construction Management 44 Summary cont. • Cost of equity also reflects financial risk associated with company having debt in its capital structure – “hidden cost” of equity financing ES3D4 / ES4D5 Construction Management 45 Cost Benefit Analysis ES3D4 / ES4D5 Construction Management 46 • Public projects are those that are undertaken by government. Their objective is not necessarily to maximize profit or NPV as discussed earlier • The main objective of public projects is to maximize social benefits and return to the society • The problem arises regarding quantification of benefits and costs. Often there is no tradable market for public goods (parks, environmental clean up, non-toll road) or even if there is, it does not reflect the true value to the society (public education, public transportation). • The method used for the evaluation of a project from the public point of view ( as opposed to a private firm which looks purely for private value creation for owner/stockholders) is called CostBenefit Analysis ( value creation for society). Massood Samii, MIT OpenCourseWare Public Projects ES3D4 / ES4D5 Construction Management 47 Definition Guide to Cost-Benefit Analysis of Major Projects, In the context of EC Regional Policy, 1997 edition, European Union Massood Samii, MIT OpenCourseWare “Cost-Benefit Analysis is a procedure for evaluating the desirability of a project by weighting benefits against costs. Results may be expressed in different ways, including internal rate of return, net present value and benefit-cost ratio.” ES3D4 / ES4D5 Construction Management 48 1. Project identification 2. Definition of objectives (unemployment, economic growth, reduce regional income inequality) 3. Feasibility and option analysis 4. Financial analysis 5. Socio-economic costs 6. Socio-economic benefits 7. Discounting 8. Economic rate of return 9. Other evaluation criteria 10. Sensitivity and risk analysis Massood Samii, MIT OpenCourseWare EU CBA for major projects ES3D4 / ES4D5 Construction Management 49 • Objective of investment may not necessarily be profit, but other factors such as job creation. • In public goods, for example non-toll highway, since no payment is taking place, evaluation must be based on another alternative. • For public goods, evaluation of benefits is in terms of non monetary returns. The gain from an investment is for the society and not for investors. Massood Samii, MIT OpenCourseWare Why Cost-Benefit Analysis ES3D4 / ES4D5 Construction Management 50 • The issue is how best to quantify the benefits other than monetary benefits from particular investment. Yet all those benefits must be put in a monetary term for comparison purposes • In NPV and IRR costs are both explicit. However, implicit cost and benefits, namely social costs are not taken into account. Massood Samii, MIT OpenCourseWare Why CBA cont. ES3D4 / ES4D5 Construction Management 51 • How do we decide on the return on public goods if they are not traded (can we find a similar trade-able good such as a similar toll road ?) • If the government charges a fee for the use of public goods, what should be the fee? ( for example, what is the proper level of toll that government collects?). After all in many cases government or the owner of public goods (even in the case of privatized toll road) has a monopoly power and therefore it can exploit this power. • What is the distributive effect of the government subsidizing the use of public goods (or taxing it)? For example if a motorway is built with tax money, but I never get to use that motorway, why should I pay for it? • What is the externality of public goods (construction of a motorway)? That is the businesses around the highway benefit from an increase in activities leading to an increase in tax revenue. Massood Samii, MIT OpenCourseWare Key questions ES3D4 / ES4D5 Construction Management 52 • What rate of discount should be used in the calculation? Some of the decision on public goods could be politically motivated. The two critical issues are prices and decision to investment. For example, price of water, electricity, toll and bridges, tuition in public universities are all political decisions and are not fully driven by market forces. • But while decisions are politically driven, they must also have economic justifications. How do we measure the economic benefits? Massood Samii, MIT OpenCourseWare Key questions cont. ES3D4 / ES4D5 Construction Management 53 Impact of Large Projects – A large project may in fact raise the labour cost for other sectors – It could also effect over all economic growth of country with its positive impact on the economy as a whole, leading to increase in demand for output of other sectors – From social point of view, government decisions must take into account these and a number of other impacts Massood Samii, MIT OpenCourseWare • Mega projects absorb a large amount of resources with substantial impact over a long term on the prices and outputs of other sectors ES3D4 / ES4D5 Construction Management 54 • Most of the public projects have a feed back system. For example, a highway to reduce traffic congestion may lead to increase in economic activities in that region, which cause migration to the area which in turn leads to more traffic and congestion. • Also, in many cases project A would effect project B either directly or sometimes indirectly through project C. For example, building of a highway may speed up traffic, but could lead to congestion in the feeder road, if they are left unimproved • While it is possible to see relationships mentioned above, their quantifications are not trivial and are quite difficult to estimate. Massood Samii, MIT OpenCourseWare Definition of project ES3D4 / ES4D5 Construction Management 55 • Public investment projects should take into account the external effect of their action so far as it alters the physical production possibilities of other producers or satisfaction that consumers get from resources. It should not take into account side effects if the sole effect is via prices of products or factors. For example, a dam has its main objective of irrigation and electricity generation, but it also may provide, free of charge, a possibility for people to use the area around it for a picnic. The benefit to users of a picnic area is the externality. But, if there is a charge for the park, only the charge should be included in the estimation. • Therefore externalities are when other benefits without payment are taking place as a result of a particular investment. Massood Samii, MIT OpenCourseWare Externalities ES3D4 / ES4D5 Construction Management 56 Secondary Benefits For example an irrigation system will lead to more grain production which in turn leads to a series of other related activates down stream. There is a debate as to whether we should use the secondary benefits. General consensus is that if the market price reflects the benefit of secondary effects we should use that, otherwise we must impute the value of secondary benefits . Massood Samii, MIT OpenCourseWare • Inducement to create other activities is considered to be secondary effect. These should be taken into account. ES3D4 / ES4D5 Construction Management 57 • Use of social rate of discount presents a number of difficulties. • Role of time and preference. Private investor preference is toward a quicker return (short term) than public investment. • The weighted average cost of capital used by the private sector as the discount rate is not applicable in the case of public projects. This is because of the structure of government financing through taxes and government bonds. • Government has the advantage in terms of having a lower rate of interest than the private sector. This implies that the social rate of discount for the same project is lower for the government than for private sector. Massood Samii, MIT OpenCourseWare Choice of Discount Rate ES3D4 / ES4D5 Construction Management 58 • The issue of distributive effect is highly theoretical. – The argument is the following: since government is the agent of society it should take the interests of all equally into account. Therefore, by its decision it will impact some people negatively (by taxation) and others positively by investment. This kind of decisions are not “Pareto Optimal”. – The counter argument is that if the net gain is greater than the net loss, the gainers can compensate losers and society is left with a net positive result. – However, this is problematic since valuation of gain and loses by individuals in the society is difficult. Massood Samii, MIT OpenCourseWare Distributional Constraints ES3D4 / ES4D5 Construction Management 59 • Implication for infrastructure is that taxing and investing in infrastructure is not “Pareto Optimal”, while privatised development of infrastructure is, since those who use the facility pay for it and are better off, whilst not taxing others . • Alternatively it is argued that if the decision improves the overall social benefit, even if it makes some worse off, it is still an acceptable decision. e.g. Government involvement in infrastructure using tax, which makes some tax payers worse off but increases the benefit to society is acceptable if the social benefits exceed the social cost. Massood Samii, MIT OpenCourseWare Social Choice ES3D4 / ES4D5 Construction Management 60 • A government has a limited budget, therefore it must allocate its resources among various uses. The issues therefore include: – Does the project provide net benefit (benefit over cost)? – Does it provide the highest net benefit among various projects government can undertake? – For whom does it create benefit (allocation issue)? Massood Samii, MIT OpenCourseWare Budgetary Constraint ES3D4 / ES4D5 Construction Management 61 A CBA is conducted for a simple highway improvement and extension. The improvement in highway leads to more capacity resulting in time saving. Data indicates that for rush hour the time cost of a trip is £5 without and £3 with the project . It is assumed that operating cost of a vehicle is unaffected by the project (£4). The project lowers the cost of each trip leading to an increase in the number of trips. For rush hour the cost saving is £2 and for non rush hour it is £0.8. The project is also expected to reduce fatalities from 12 per year to 6. We assume value of time to be £0.1 per minute during rush hour and 0.08 during non-rush hour. Massood Samii, MIT OpenCourseWare Example ES3D4 / ES4D5 Construction Management 62 Example cont. Massood Samii, MIT OpenCourseWare Assume cost of right of way is £100 million that can be recovered at the end of the project and that the construction cost is £200 million over four years (£50 million a year) and maintenance £1 million per year. Calculate whether this project makes sense if the life of the project is 30 years and the bond rate is 4% with 2% inflation rate (2% real interest). ES3D4 / ES4D5 Construction Management 63 Massood Samii, MIT OpenCourseWare Data for Highway Project ES3D4 / ES4D5 Construction Management 64 Determining Consumer Surplus ES3D4 / ES4D5 Construction Management 65 Massood Samii, MIT OpenCourseWare ES3D4 / ES4D5 Construction Management 66 Massood Samii, MIT OpenCourseWare ES3D4 / ES4D5 Construction Management 67