Study

lib

Documents

Flashcards

Chrome extension

Login

Upload document

Create flashcards

×

Login

Flashcards

Collections

Documents

Last activity

My documents

Saved documents

Profile

Foreign Language

Math

Science

Social Science

Business

Engineering & Technology

Arts & Humanities

History

Miscellaneous

Standardized tests

Business

Finance

Derivatives

Quiz For Lecture # 11 European Call Option using Black-Scholes/Merton

QuickGuide - Option Wizard

Quick Reference Card - Microsoft Center

questions in English

Questions (10)

Q3 2009/10 results 11 February 2010 BT Group plc 1

Q1 Option Valuation (European call, binomial tree)

Q. Q. Q. - New Hampshire Public Utilities Commission

Q&A

Q LCH.CLEARNET

Q Discuss the following questions: How can we use the futures

Put and Call Options

Purpose and objectives

PUBLIC SUMMARY DOCUMENT Product: Welland Aurum One

Risky Games - Universitat Pompeu Fabra

Risks

Risk Warning

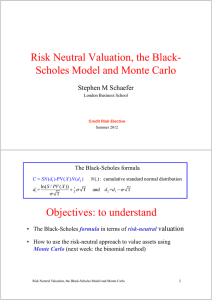

Risk Neutral Valuation & Black-Scholes Model

Risk Measurement: An Introduction to Value at Risk

Risk Management and Insurance

Risk Management and Financial Management Training Modules with FAST Tools 1

Risk Management and Financial Institutions, 2e, Chapter 5

Risk Analysis of Interruptible Load Contracts ∗ Paula Rocha Afzal Siddiqui

Revise Lecture 9

«

prev

1 ...

50

51

52

53

54

55

56

57

58

... 106

»

next

Suggest us how to improve StudyLib

(For complaints, use

another form

)

Your e-mail

Input it if you want to receive answer

Rate us

1

2

3

4

5

Cancel

Send