+ P(1+i )

advertisement

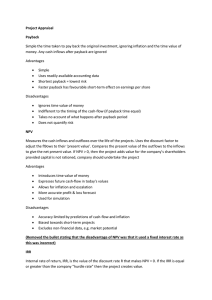

")

ECE 333 Renewable Energy Systems Lecture 19: Economics Prof. Tom Overbye Dept. of Electrical and Computer Engineering University of Illinois at Urbana-Champaign overbye@illinois.edu Announcements • • • HW 8 is 5.4, 5.6, 5.11, 5.13, 6.5, 6.19; it should be done before the 2nd exam but need not be turned in and there is no quiz on April 9. Read Chapter 6, Appendix A Exam 2 is on Thursday April 16); closed book, closed notes; you may bring in standard calculators and two 8.5 by 11 inch handwritten note sheets – In ECEB 3002 (last name starting A through J) or in ECEB 3017 (last name starting K through Z) 1 Energy Economic Concepts • Next several slides cover some general economic concepts that are useful in evaluating renewable energy projects – – Useful in general, but quite appropriate for distributed PV system analysis Covered partially in Section 6.4 and in Appendix A 2 Energy Economic Concepts • The economic evaluation of a renewable energy resource requires a meaningful quantification of cost elements – – • fixed costs variable costs We use engineering economics notions for this purpose since they provide the means to compare on a consistent basis – – two different projects; or, the costs with and without a given project 3 Time Value of Money • Basic notion: a dollar today is not the same as a dollar in a year – – Would you rather have $10 now or $50 in five years? What would a $50,000 purchase you’ll make in 10 years be worth today? • The convention we use is that payments occur at the end of each period (e.o.p.) 4 VIDEO TIME! http://www.investopedia.com/t erms/t/timevalueofmoney.asp 5 Time Value of Money – Principle and Interest • • Principle – the initial sum Interest – productivity of money over time, money today vs. money tomorrow – – Simple interest – not compounded, interest is only paid on the principle amount Compound interest – (what we consider) when interest is also paid on the interest vs. on the principle only Difference between the two is greater when: the interest rate is higher, compounding is more frequent, duration of payments is longer EXAMPLE! P = principal i = interest value 6 Positive Interest Rate (i > 0) • • • • A positive interest rate means that having $1.00 in 10 years is not as good as having one dollar today The assumption is that over 10 years, you could do something better with that $1.00 – you can use the $1.00 to make more money You can even put your $1.00 in the bank and earn interest, which is like the worst case since you could invest in something better Hence, i > 0 → Future value > Present value (F > P) 7 Compound Interest e.o.p. amount owed interest for next period amount owed for next period 0 P Pi P + Pi = P(1+i ) 1 P(1+i ) P(1+i ) i P(1+i ) + P(1+i ) i = P(1+i ) 2 2 P(1+i ) 2 P(1+i ) 2 i P(1+i ) 2 + P(1+i ) 2 i = P(1+i ) 3 3 P(1+i ) 3 P(1+i ) 3 i P(1+i ) 3 + P(1+i ) 3 i = P(1+i ) 4 n-1 P(1+i ) n-1 P(1+i ) n-1 i P(1+i ) n-1 + P(1+i ) n-1 i = P(1+i ) n n P(1+i ) n The value in the last column for the e.o.p. (k-1) provides the value in the first column for the e.o.p. k (e.o.p. is end of period) 8 Terminology • • We call (1 + i) n the single payment compound amount factor 1 We define 1 i and 1 i is the single payment present worth factor F is called the future worth; P is called the present worth or present value at interest i of a future sum F n n • F P 1 i n or P F 1 i n 9 Cash Flows • • A cash flow is a transfer of an amount A t from one entity to another at end of point (e.o.p.) time t Each cash flow has (1) amount, (2) time, and (3) sign Ex. I take out a loan 0 1 2 3 4 I make equal repayments for 4 years 10 Cash Flows Diagrams - Overview End of year 1 0 1 Present 2 3 4 Convention for cash flows inflow outflow Ex. Take out a loan Revenue collected Incoming cash flows Ex. Initial purchase Payments made Outgoing cash flows11 VIDEO TIME! http://www.investopedia.com/t erms/c/cashflow.asp 12 Discount Rate • • • The interest rate i is typically referred to as the discount rate d because it is used to “discount” cash flows to the present In converting a future amount F to a present worth P, we can view the discount rate as the interest rate that can be earned from the best investment alternative A postulated savings of $ 10,000 in a project in 5 years is worth at present P F5 10,000 1 d 5 5 13 Discount Rate • • • For d = 0.1, P = $ 6,201, while for d = 0.2, P = $ 4,019 In general, the lower the discount factor, the higher the present worth The present worth of a set of costs under a given discount rate is called the life-cycle costs 14 VIDEO TIME! http://www.investopedia.com/t erms/d/discountrate.asp 15 Equivalence • • • • It can be difficult to tell if a project makes sense or not just from the cash flow diagram This is because the payments are in different years, and the value of money in different years is not equivalent n But, we saw that F P 1 d This means that with an interest rate of i, $P today is equivalent to $F at the end of year n 16 Equivalence • • Using this notion, we can take any amount kj and “move” or “discount” it to a future year (j+n1) or to a past year (j-n2) using the discount rate d Hence, the following three cash flow sets are equivalent: 17 Equivalence • • • Projects can be compared by examining the equivalence of their cash flow sets Two cash-flow sets (i.e., for projects) a A t : t 0,1,2,..., n and b A t : t 0,1,2,..., n under a given discount rate d are said to be equivalent cash-flow sets if their worths, discounted to any point in time, are identical. It doesn’t matter which point in time the cash flows are discounted to, but it is common to discount everything to the present (called Net Present Value (NPV)) 18 Equivalence • Common conversion factors – – – Present Value- (P|A,i%,n) and (P|F,i%,n) Future Value- (F|A,i%,n) and (F|P,i%,n) Capital Recovery Factor- (A|P,i%,n) P = Present value F = Future value A = Annual value 19 Equivalence, Example • Are these cash-flow sets equivalent? 8,200.40 d = 7% a A t b A t 2000 2000 2000 2000 2000 0 1 2 3 4 a 5 6 7 0 1 b 2 20 Equivalence, cont. • Let’s move each cash flow set to year 2 Cash flow set a 1 F2 2000(1 i ) 2000(1 i ) 2 2000(1 i )3 2000(1 i )4 2000(1 i )5 = 8200.40 Cash flow set b F2 8200.40 • Therefore, A at and A bt are equivalent cash flow sets under d = 7% 21 Present and Future Value, Example • Consider the set of cash flows illustrated below $ 400 $ 300 $ 200 $ 200 3 0 1 4 2 5 6 7 8 d = 6% $ 300 22 Example, cont. • We compute F 8 at t = 8 for d = 6% F8 300 1 .06 300 1 .06 7 Future Value • 5 200 1 .06 400 1 .06 200 $ 951.56 4 2 We next compute P P 300 1 .06 300 1 .06 1 Present Value • 200 1 .06 $ 597.04 4 3 400 1 .06 6 200 1 .06 8 We check that for d = 6% F8 597.04 1 .06 $ 951.56 8 23 Annualized Investment • A capital investment, such as a renewable energy project, requires funds, either borrowed from a bank, or obtained from investors, or taken from the owner’s own accounts • Conceptually, we may view the investment as a loan with interest rate i that converts the investment costs into a series of equal annual payments to pay back the loan with the interest 24 Annual Payments, Example What value must A have to make these cash flows equivalent? $ 2000 1 2 3 4 5 0 i = 6% A A A A A Solution: Find A such that the NPV is zero 25 Cash Flows, cont. • Write down the equation for the net present value of the cash flow set, set equal to zero, then solve for A P A(1.06)1 A(1.06)2 ... A(1.06) n 0 n P A 1 0.06 t 1 t n A t 1 t (1 d ) 1 n d (1 d ) t 1 n n t d (1 d ) A P 2000 (A|P,6%,5) n (1 d ) 1 n Annualized Value (A) A $474.79 What about as d goes to zero? 26 Annualized Investment • Then, the equal annual payments are given by d (1 d )n A P n (1 d ) 1 A P CRF(i ,n) • • • Capital Recovery Factor (CRF) (5.20) The capital recovery factor, CRF(i,n), is the inverse of the present value function PVF CRF measures the speed with which the initial investment is repaid Capital recovery function in Microsoft Excel: PMT(rate,nper,pv) 27 Mortgage payment example • What is the monthly payment for a 100K, 15 year mortgage with a monthly interest rate of 0.5%? – – – • = PMT(0.005,180,100000) =$843.86 per month If terms are changed to 20 years payment goes to $716/month Assume a 100K investment in a PV installation with a 15 year life, monthly interest rate of 0.5%, and no O&M expenses. What is monthly income needed to cover the loan? – Solution is the same as above 28 Infinite Horizon Cash-Flow Sets • Consider a uniform cash-flow set with n At A : t 0, 1, 2, ... • Then, P A n 1 d n 1 A d For an infinite horizon uniform cash-flow set A d P d = “ simple rate of return” 1/d = “simple payback” d is also the CRF, since A = dP 29 Internal Rate of Return • • • Until now, we have always specified the interest rate or discount rate Now we’ll “solve for” the rate at which it makes sense to do the project This is called the internal rate of return, also called the “break-even interest rate” – • Higher is better because a higher IRR means that even if the interest rate gets higher, the project still makes sense to do Note there is no closed form solution - use a table (or Excel, etc.) to look it up 30 Internal Rate of Return • Consider a cash-flow set A A : t 0, 1, 2, ... t • The value of d for which n P t A t 0 t 0 • is called the internal rate of return (IRR) The IRR is a measure of how fast we recover an investment or stated differently, the speed with which the returns recover an investment 31 VIDEO TIME! http://www.investopedia.com/t erms/i/irr.asp 32 Internal Rate of Return Example • Consider the following cash-flow set $6,000 $6,000 $6,000 $6,000 $6,000 0 1 $30,000 2 3 4 8 33 Internal Rate of Return • The present value P 30, 000 6, 000 (P|A,i%,8) 0 30, 000 (P|A,i%,8)= 5 6, 000 units are years has the (non-obvious) solution of d equal to about 12%. – • From Table 5.4: rows= n, values= (P|A, i%, n), cols= IRR The interpretation is that with a 12% discount rate, the present value of the cash flow set is 0 and so 12% is the IRR for the given cash- flow set – The investment makes sense as long as other investments yield less than 12%. 34 Efficient Refrigerator Example • • A more efficient refrigerator incurs an investment of additional $ 1,000 but provides $ 200 of energy savings annually For a lifetime of 10 years, the IRR is computed from the solution of 0 1, 000 200 (P|A,i%,10) or (P|A,i%,10) 5 The solution of this equation requires either an iterative approach or a value looked up from a table 35 Efficient Refrigerator Example, cont. •IRR tables show that (P|A,i%,10) d 15% 5.02 and so the IRR is approximately 15% If the refrigerator has an expected lifetime of 15 years, this value becomes (P|A,i%,15) d 18.4% 5.00 As discussed earlier, the value is 20% if it lasts forever 36 Impacts of Inflation • • • Inflation is a general increase in the level of prices in an economy; equivalently, we may view inflation as a general decline in the value of the purchasing power of money Inflation is measured using prices: different products may have distinct escalation rates Typically, indices such as the CPI – the consumer price index – use a market basket of goods and services as a proxy for the entire U.S. economy – reference basis is the year 1967 with the price of $ 100 for the basket (L 0); in the year 1990, the same basket cost $ 374 (L 23) 37 US Inflation Over Last 350 Years Historically prices have gone up and gone down. Recently many homeowners found home prices can also fall! Source: http://upload.wikimedia.org/wikipedia/commons/2/20/US_Historical_Inflation_Ancient.svg 38 Figuring Average Rate of Inflation • Calculate average inflation rate from 1982 to 2014 234 32 Current 1 e 2.34 100 (12/2014) basket ln 2.34 ln 1 e e 2.69% value is 32 about 234 compared to base year of 1982. Annual rate is about 1% in 2014 https://qzprod.files.wordpress.com/2014/11/us-consumer-price-indexes-year-on-year-change-core-cpi-headline-cpi_chartbuilder.png?w=1280 39 Inflation (Escalation) Rate • With escalation, an amount worth $1 in year zero becomes $(1+e) in year 1, etc., so PVF(d ,n) 1 1 1 + ... n 1+d 1+d 2 1+d becomes PVF(d ,e,n) • 1+e 2 1+e n 1+e + ... 2 n 1+d 1+d 1+d We can compare terms to find an equivalent discount rate d’: 1+e 1 1+d 1+d ' 40 VIDEO TIME! http://www.investopedia.com/t erms/i/inflation.asp 41