Chapter 12

Goodwill and Other

Intangible Assets

Prepared by:

Patricia Zima, CA

Mohawk College of Applied Arts and Technology

Goodwill and

Other Intangible Assets

Definition,

Recognition

and

Measurement

•Characteristics

•Recognition

and

measurement

at acquisition

•Measurement

after acquisition

Types of

Impairment

Intangibles of Intangible

•Marketing- Assets

related

•Limited-life

•Customer- intangibles

related

•Indefinitelife

•Artisticintangibles

related

other than

•Contractgoodwill

based

•Goodwill

•Technologybased

•Goodwill

Other Internally

Developed

Intangibles

•Research and

development

costs

•Development

stage costs

•Organization

costs

•Advertising

costs

•Conceptual

questions

Presentation,

Analysis, and

International

Comparison

•Presentation

of intangible

assets

•Perspectives

•Comparison

of Canadian

and

International

GAAP

Appendix

12A–

Valuing

Goodwill

•Excessearnings

approach

•Totalearnings

approach

•Other

methods of

valuation

2

Intangibles: Characteristics

•

CICA Handbook, Section 3062, broadly

defines intangible assets as:

1. Assets that are lacking in physical

substance, and

2. Assets that are not financial instruments

• Examples of intangible assets: patents,

copyrights, franchises, and trademarks

3

Recognition and Measurement at

Acquisition

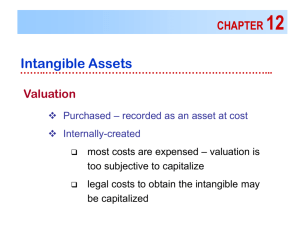

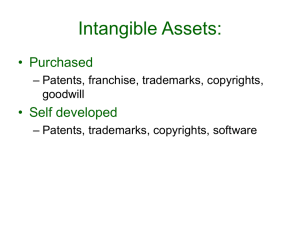

• Purchased Intangibles

– Measured at cost

– Cost includes all expenditures that are necessary

to get the intangible asset ready for its intended

use (e.g., purchase price, legal fees)

• If intangible assets are exchanged for non-monetary

assets, the fair value of the item given up or the fair

value of the intangible received is used to determine

cost

• For a “basket purchase” of intangibles, the cost is

allocated based on fair values

4

Recognition and Measurement

at Acquisition

•

Identifiable intangibles:

– are recognized separately

– must have at least one of the following

characteristics:

1. Results from contractual or legal rights,

2. They can be separated from the entity and

sold, rented, exchanged, transferred or

licensed

• Identifiable intangibles with similar

characteristics should be grouped and reported

5

together

Recognition and Measurement

at Acquisition

• Internally Developed Intangibles

– Costs that a company incurs internally to

create intangibles (such as patents and

brand names) are generally expensed

• Deferred Charges

– Costs incurred that benefit future periods

– It has become less acceptable to recognize

deferred charges unless the costs meet the

definition and recognition requirements of

Section 1000

6

Accounting for the Acquisition Costs

of Intangibles

Type

Manner Acquired

Purchased

Internally

created

Identifiable

Capitalize

Generally

expense

Goodwill-type

Capitalize

Expense

Other internally

developed

Capitalize restricted amounts

for both

7

Measurement after Acquisition

•

An intangible asset with finite (or limited) useful

life is amortized over its useful life

• Intangibles assumed to have no residual value,

unless:

1. There is a commitment to purchase, or

2. There is an observable market

• An intangible asset with an indefinite useful life

is not amortized and an impairment test is

carried out at least annually

8

Valuation after Acquisition

•

•

Factors to consider when determining useful life of

an intangible asset:

1. Expected future usage

2. Legal, regulatory, or contractual provisions

that may limit useful life

3. Effects of technological or commercial

obsolescence

4. Level of maintenance expenditures required

to obtain future benefits

Method of amortization chosen should match

benefits received, otherwise, straight-line

amortization used

9

Types of Intangibles

Six major categories for intangibles:

1. Marketing-related

2. Customer-related

3. Artistic-related

4. Contract-based

5. Technology-based

6. Goodwill

10

Marketing-Related Intangibles

• Used in marketing and promotion

• Include:

– Trademarks or trade names

– Newspaper mastheads

– Internet domain names

– Non-competition agreements

11

Trademarks and

Trade Names

• Trademarks and trade names are renewable

indefinitely every 15 years, so the legal life may be

unlimited; the useful life, however, may be limited

• Costs of acquired trademarks or trade names are

capitalized

• If trademarks or trade names are developed by the

business, all direct costs are capitalized

• If the future benefits of a trademark (such as CocaCola) is determined to have an indefinite life, it is

not amortized

12

Customer-Related Intangibles

• Result from interactions with third parties

• Include:

– Customer lists

– Order/production backlogs

– Contractual and noncontractual customer

relationships

13

Artistic-Related Intangibles

• Ownership rights to artistic endeavours

• Examples: literary works, musical works,

pictures, photographs and audiovisual

material

• These ownership rights are protected by

copyrights

14

Copyrights

• Copyrights are granted for the life of the creator,

plus 50 years

• Copyrights can be sold or assigned, but cannot be

renewed

• Useful life is generally less than the legal life

• Amortized over period in which benefits accrue

• Costs of acquiring and defending copyrights are

capitalized

• Research costs associated with a copyright are

expensed

15

Contract-Based Intangibles

• Value of a right resulting from a contractual

arrangement

• Examples: licensing arrangement, leaseholds,

construction permits, broadcast rights, service or

supply contracts, franchises, and licenses

• A franchise is a contractual agreement where

franchisor grants the franchisee the rights to:

– sell specified products or services

– use certain trademarks or trade names

– perform certain functions within a particular

geographical area

16

Franchises and Licenses

• A franchise may exist for a limited time or for an

indefinite time period

• The cost of a franchise (with a limited life) is

amortized over the lesser of the legal or useful life

• A franchise (with an unlimited life) is amortized

over:

– expected useful life if such life is deemed

limited, or

– it is not amortized

• Annual operating payments for a franchise are

expensed

17

Leaseholds

• Agreement between the lessor (owner) and the

lessee (renter)

• Gives the lessee the right to use the property

• Valid for a specific period of time

• The lessee makes stipulated, periodic cash

payments which are normally expensed

• Capital Leases: if the lease agreement transfers

all benefits and risks to the lessee

• For capital leases, the PV of all future payments

is recorded as a tangible asset and as a longterm liability

18

Leaseholds and Leasehold

Improvements

• Lease prepayments are reported as prepaid

expenses, not as intangible assets

• Leasehold improvements are improvements

made by the lessee to the leased property

• These leasehold improvements revert to the

lessor at the end of lease term

• They are generally shown in the property,

plant, and equipment section of the balance

sheet, rather than with intangible assets

19

Technology-Based Intangibles

•

Relate to innovations or technological

advances

• Include:

1. Product Patents

• Physical (tangible) products

2. Process Patents

• Process by which products are made

3. Computer Software Costs

20

Patents

• A patent gives exclusive right to the holder for

making, selling or using a product or process

• Costs of purchasing patents are capitalized

• Costs to research and most development costs

are expensed as incurred

• Patents are amortized over the shorter of the

legal life (20 years) or their useful lives

• Legal fees and other costs to successfully

defend a patent are capitalized and amortized

over the remaining useful life of the patent

21

Computer Software Costs

• External Use

– Designed for resale

– Development costs treated as research and

development costs

• Internal Use

– Designed for use within the organization

– Purchase cost and all direct costs of the

software may be capitalized

– Any modifications to the software are capitalized

if considered a betterment

22

Goodwill

• Goodwill is the excess of the purchase price

over the fair value of the identifiable tangible and

intangible net assets acquired in a business

combination

• Goodwill can be acquired and sold only when a

business combination occurs

• Goodwill cannot be separated from the business

• Internally-generated goodwill is not capitalized

• Goodwill is the only intangible requiring separate

disclosure on the balance sheet

23

Acquired Goodwill: Valuation

Given:

Purchase price (cash):

Book value of assets:

Book value of liabilities:

Fair value of assets:

$ 400,000

$ 255,000

$ 55,000

$ 350,000

To determine goodwill, see the following:

24

Acquired Goodwill: Calculation

Goodwill =

Purchase price – Fair value of identifiable net

assets

Goodwill = $400,000 less 350,000 = $50,000

Entry in the books of the Purchaser:

Assets (various) 405,000

Goodwill

50,000

Liabilities

55,000

Cash

400,000

25

Negative Goodwill

•

“Negative goodwill” or a bargain purchase

arises when fair value of acquired net assets

is greater than the purchase price

• The current standard requires that:

– The excess is used to reduce the amounts

assigned to other acquired assets that are

generally non-financial in nature, and

– Any excess remaining is treated as an

extraordinary gain

26

Goodwill–Valuation after Acquisition

•

Three approaches have been suggested:

1. Charge immediately to expense

– Results in consistent accounting for purchased

goodwill and internally generated goodwill

– One rationale is that difficult to identify the

useful life

2. Amortize over useful life

– Better matching of costs to benefits

3. Carry at cost indefinitely, unless value impaired

– Method approved by Accounting Standards

Board

– Management is responsible for performing an

impairment test

27

Intangible Asset Impairment –

Limited-Life Intangibles

• Impairment occurs when carrying value of an

asset is greater than fair value of the asset

• A recoverability test is necessary to determine

whether the asset has been impaired

• If expected future cash flows is less than the

carrying amount of the asset, asset is impaired

• If impairment, an impairment loss (carrying

amount – fair value) is recognized in the period,

usually as part of continuing operations

• Same approach as for impairment of tangible

assets

28

Limited-Life Intangibles

Impairment

Example:

Carry amount of patent

$6,000,000

Recoverable amount

3,500,000

Fair value (discounted amount) 2,000,000

Recoverability test?

• Indicates impairment

(since $3,500,00 < $6,000,000)

Impairment loss?

• $6,000,000 – $2,000,000 = $4,000,000

29

Limited-Life Intangibles

Impairment

Loss on Impairment

4,000,000

Accumulated Amortization, Patents 4,000,000

• Remaining carrying amount amortized over

expected useful life

• Future increases in value of intangible are not

recognized

30

Indefinite-Life Intangibles Other

than Goodwill - Impairment

• Impairment test should be done annually

• Use fair value test only

• Fair value of intangible compared to the

carrying amount

• When fair value is less than carrying amount,

impairment has occurred and loss is recorded

• The recoverability test is not used for

indefinite-life intangible assets

31

Goodwill Impairment

•

Two-step process

1. Fair value of the reporting unit compared

to carrying amount of the reporting unit,

including goodwill

• When fair value greater than carrying

amount, no impairment

• When fair value less than carrying

amount, then a second step is

required

2. Determine if goodwill is impaired (see

next slide)

32

Goodwill Impairment

•

•

•

•

Compare implied current fair value of goodwill

with carrying amount of goodwill

Implied current fair value of goodwill:

– Fair value of the whole reporting unit is

compared to the fair value of the identifiable

net assets

When the fair value is less than carrying amount,

impairment is recognized

Goodwill impairment loss is reported separately

in the income statement before extraordinary

items and discontinued operations

33

Deferred Charges

• Intangibles that may be recorded as deferred

charges include: deferred development costs,

pre-operating and start-up costs, and

organization costs

• CICA Handbook, Section 3070, Deferred

Charges, removed from the handbook in

2005

• “Deferred charges” are not as common as

previously, as the costs must now meet the

definition of an asset

34

Research and Development

(R&D) Costs

•

R&D costs are not in themselves intangible

assets

• Generally material in amount and generally

lead to something that will be patented or

copyrighted

• Challenges in R&D accounting:

1. Determining costs associated with a

particular activity or project

2. Determining size of future benefits and for

how long those benefits may be realized

35

Research and Development

(R&D) Costs

• CICA Handbook, Section 3450 governs the

accounting for R&D costs:

– All research costs are charged to expense

when incurred

– Development costs are charged to expense

except in certain defined circumstances

– An exception to the above, may be able to

capitalize if a company purchases in-process

R&D as part of a business combination

36

Research and Development

(R&D) Costs

• Research activities:

– involve planned search or critical investigation

aimed at discovery of new knowledge

– may or may not be directed towards a specific

project

• Development activities include:

– translation of research findings or other

knowledge into a plan or design for a new

product or process, or

– significant improvement to an existing product

or process

37

Research and Development

(R&D) Costs

•

•

R&D costs include the following:

1. Materials and services consumed

2. Direct personnel costs (e.g., salaries)

3. Amortization of equipment and facilities used

in R&D activities

4. Amortization of intangibles related to R&D

activities

5. Reasonable overhead allocation

Development costs are capitalized when all five of

the following conditions are met and future benefits

are reasonably certain

38

Research and Development

(R&D) Costs

•

Development cost capitalization criteria:

1. Product/process clearly defined, and costs

can be identified

2. Technical feasibility has been established

3. Management’s intent is to produce and

market or use the product/process

4. If the intent is to sell, a market is clearly

defined; if the intent is to use, there is a

definable use/need

5. Resources exist to complete the project

39

Pre-Operating Costs

•

•

•

Costs incurred prior to start of formal

operations

EIC-27 allows for the deferral of pre-operating

costs if three conditions are met:

1. The expenditure relates directly to placing

the new business in service

2. It would not have been incurred if not for

the new business

3. The amount is likely to be recovered from

future operations of the new business

Amortized over maximum of 5 years

40

Other Deferred Charges

Organization Costs:

• Costs incurred to form a corporation (e.g.,

underwriter fees, legal fees)

• Usually recorded as an intangible asset

• They are usually amortized over a relatively

short period of time (perhaps up to 5 years)

Advertising Costs:

• No Canadian standard

• Usually expensed as difficult to measure future

benefits

41

International Comparison

• Canadian and international GAAP are

substantially converged for intangible

assets

• Some differences still exist related to the

treatment of “negative” goodwill, preoperating costs, internally developed

intangibles, and impairment models of

goodwill and other intangibles

42

COPYRIGHT

Copyright © 2007 John Wiley & Sons Canada, Ltd.

All rights reserved. Reproduction or translation of

this work beyond that permitted by Access Copyright

(The Canadian Copyright Licensing Agency) is

unlawful. Requests for further information should be

addressed to the Permissions Department, John

Wiley & Sons Canada, Ltd. The purchaser may make

back-up copies for his or her own use only and not

for distribution or resale. The author and the

publisher assume no responsibility for errors,

omissions, or damages caused by the use of these

programs or from the use of the information

contained herein.

43