Chapter 9

advertisement

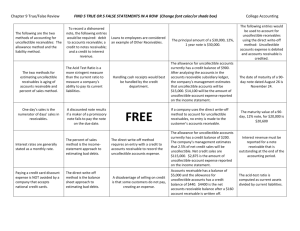

CHAPTER 9 Receivables Chapter Overview The chapter begins with an overview of various types of receivables – both current and long-term. Internal controls over receivables, the duties of the credit department, and Decision Guidelines for controlling, managing, and accounting for receivables are presented. The concept of uncollectible-account expense is introduced along with an explanation of the Allowance for Uncollectible Accounts, a contra account related to Accounts Receivable. Two methods for recording uncollectible accounts are discussed: first the allowance method and, later in the chapter, the direct write-off method. The authors explain the preference for the allowance method. Two methods for estimating uncollectible-account expense are presented and illustrated: the percent of sales method and the aging-of-accounts method. Entries are shown for recording the uncollectible-account expense each period and for writing off uncollectible accounts. The direct write-off method is explained. Entries for recording recoveries on accounts previously written off are illustrated. A brief discussion of both credit-card sales and debit-card sales concludes this part of the chapter. A mid-chapter summary problem allows students to practice estimating uncollectibles and reporting receivables on the balance sheet. Next, notes receivable are presented, including terms, calculations, and journal entries related to notes. Accruing interest revenue at the end of the accounting period is illustrated. Students learn how to account for a dishonored note. Different balance sheet presentations of notes and accounts receivable are shown. The role that the acid-test ratio and days’ sales in receivables play in decision making is demonstrated. Additional Decision Guidelines for receivables and an Excel Application problem conclude the chapter. An end-of-chapter summary problem reviews notes receivable calculations and entries. The Appendix to Chapter 9 discusses discounting notes receivable. Learning Objectives After studying Chapter 9, your students should be able to: 1. Design internal controls for receivables 2. Use the allowance method to account for uncollectibles by the percent-of-sales and aging-of-accounts methods 3. Use the direct write-off method to account for uncollectibles 4. Account for notes receivable 5. Report receivables on the balance sheet 6. Use the acid-test ratio and days’ sales in receivables to evaluate a company Chapter Outline Introduction to Receivables A. Receivables are monetary claims against businesses and individuals. These claims arise from selling goods or services on credit or from lending money. B. C. D. 1. Each credit transaction involves a creditor who sells something and obtains a receivable, and a debtor who makes the purchase and has a payable. 2. Exhibit 9-1 is the asset portion of a balance sheet, with receivables highlighted. An account receivable or trade receivable represents an amount due from a customer. 1. An account receivable is an amount due from a customer for goods or services sold. 2. The account is classified as a current asset on the balance sheet. 3. A subsidiary ledger includes a separate account for each customer. A note receivable is more formal than an account receivable. 1. A note receivable is a written promise to receive cash; a promissory note is a negotiable document that serves as evidence of the receivable. 2. A note receivable may be classified as either current or long-term, depending on its maturity date. Other receivables may include loans to employees or subsidiary companies; these may be either current or longterm assets. Objective 1: Design internal controls for receivables A. Internal control over collections of cash on account is important. 1. Cash-handling duties should be separate from cash-accounting duties. 2. The bookkeeper should not also handle cash receipts. A bank lock box accomplishes the same control over receipts of cash. 3. The person posting the accounts receivable subsidiary ledger should not also handle cash receipts. B. The credit department is responsible for evaluating and approving new credit customers as well as monitoring the payment history of current customers. The credit department should not have access to cash. C. Decision Guidelines discuss controlling, managing, and accounting for receivables. D. Selling on credit creates both a benefit (more sales) and a cost (some customers will not pay). E. F. 1. Uncollectible-account expense results from charge sales that customers cannot or will not pay. 2. The account may also be called doubtful-account expense or bad-debt expense. This is a normal expense for any business that sells on credit; two methods are used for recording this expense: 1. The allowance method – preferred because it matches collection losses with revenues in the period in which the sales were made. 2. The direct write-off method – fails to match the expense with the sales revenue. The allowance method of recording uncollectible-account (or bad-debt) expense is based on estimates of collection losses. 1. Allowance for Uncollectible Accounts (or Allowance for Doubtful Accounts) is a contra account, an asset account with a credit balance. This account represents the estimated amount of collection losses, or the amount of receivables the business expects not to collect. 2. On the balance sheet, net accounts receivable equals Accounts Receivable minus Allowance for Uncollectible Accounts. Net accounts receivable is the amount of receivables the business expects to collect. 3. Uncollectible-Account Expense is reported on the income statement. Objective 2: Use the allowance method to account for uncollectibles by the percent-of-sales and aging-of-accounts methods A. Under the allowance method, there are two ways to estimate uncollectible-account expense: percent-of-sales and aging-of-accounts. 1. The percent-of-sales method (also called the income statement approach) considers the credit sales for the period. If focuses on the amount of expense to be reported on the income statement. a. The percentage used is an historical percentage based on prior uncollectible accounts and past collection experience. To calculate the uncollectible-account expense, the percentage is multiplied by the credit sales. b. At the end of each accounting period this adjusting entry is made: Uncollectible-Account Expense XX Allowance for Uncollectible Accounts c. 2. XX This entry adjusts the Allowance account by the amount of expense. The aging-of-accounts method (also called the balance-sheet approach) considers the age and amount of accounts receivable at the end of the period. This method focuses on the amount of net accounts receivable to be reported on the balance sheet. a. First, the accounts are aged (classified according to the age of the account), as illustrated in Exhibit 9-2. b. An historical percentage is applied to each age category. This amount represents the estimated amount of uncollectible accounts from each age category. When these amounts are added together, the total is the desired ending balance in the Allowance account. c. The longer an account goes uncollected, the more likely it is to become a bad debt; therefore a higher percentage is applied to accounts that are long past due. d. The amounts of uncollectible accounts from each category are added together. This amount is the desired ending balance in the Allowance Account. (See Exhibit 9-2.) e. To calculate the expense, consider the unadjusted balance in the Allowance account and the desired ending balance, based on the calculation described above. The expense is the amount that will be added to (or deducted from) the Allowance account to achieve the desired ending balance. f. At the end of each accounting period this adjusting entry is made: Uncollectible-Account Expense XX Allowance for Uncollectible Accounts XX g. Note that this entry adjusts the Allowance account to the estimated amount of uncollectible accounts. B. Net realizable value is the net amount of accounts receivable – Accounts Receivable less Allowance for Uncollectible-Accounts. C. The percent of sales and aging methods may be used together. For interim statements, the percent of sales method is easy to use; at year-end, the aging method is more accurate because it adjusts accounts receivable to the expected realizable value. For a comparison of the two methods, see Exhibit 9-3. D. An account is written off when it is determined to be uncollectible. No expense is recorded at this time. Instead, the Allowance account is reduced with a debit. 1. When an account is deemed to be uncollectible, the entry to write-off this account is: Allowance for Uncollectible Accounts XX Accounts Receivable (customer name) 2. XX The write-off of an account has no effect on net income; it does not have any effect on net receivables. In other words, net receivables are the same before and after the write-off because the company still expects to collect the net amount. Objective 3: Use the direct write-off method to account for uncollectibles A. When using the direct write-off method of accounting for uncollectible receivables, the company waits until a customer’s account is deemed uncollectible to write off the account. 1. At the time an account is written off, this entry is made: Uncollectible-Account Expense XX Accounts Receivable (customer name) B. 2. This method is defective because it does not set up an allowance for uncollectibles, resulting in accounts receivable that may be overstated on the balance sheet. 3. The direct write-off method does not match revenue and uncollectible-account expense. In some cases, the expense may be recorded in a later period than the revenue. 4. However, the direct write-off method is easy to use and will not create significant distortions in income or assets if collection losses are insignificant. If an account written off is later collected, two entries are required: one entry to reverse the original write-off of that account and a second entry to record the cash collection. Accounts Receivable (customer name) XX Allowance for Uncollectible Accounts To reverse previous write-off. Cash Accounts Receivable (customer name) To record collection of account receivable. C. XX XX XX XX Credit-card and bankcard sales benefit both consumers and retailers. 1. With cards such as American Express, VISA, and Discover, the customer does not have to pay cash immediately, but is instead billed monthly. The customer then writes only one check for the statement balance. 2. The retailer receives cash almost immediately for the sale (rather than having to wait until the customer is billed) and does not have to check a customer’s credit or send bills. a. The retailer’s entry when there are credit-card sales is: Accounts Receivable – Discover Credit-Card Discount Expense Sales Revenue b. XX XX XX When the retailer collects the discounted amount: Cash XX XX Accounts Receivable – Discover c. The retailer’s entry when there are bankcard sales such as VISA is: Cash Bankcard Discount Expense Sales Revenue D. XX XX XX Debit cards do not require a third party (such as VISA). When the buyer uses the card, his cash account is immediately decreased and the vendor’s cash is immediately increased. Objective 4: Account for notes receivable A. A note receivable represents a written promise to pay a specific sum of money on a particular date. Key terms and features related to a promissory note are illustrated in Exhibit 9-4 and given below: 1. The principal is the amount borrowed by the debtor. 2. The maker of the note is the debtor; the payee is the creditor. 3. The interest is revenue to the payee and the borrower’s cost of using the creditor’s money. It is always stated on an annual basis unless specified. The text uses a 360-day year. Interest is calculated as: Principal x Rate x Time = Interest 4. B. Maturity value (principal plus interest) is due on the maturity date. To determine maturity date, count the exact days or months from the issue date of the note. Be sure to begin counting on the day following the date of the note. Accounting for notes receivable is illustrated below: 1. A note receivable may be received for cash, for a sale, or in settlement of an account. The entry is: Note Receivable – Maker XX Cash (or Sales Rev. or Accounts Rec.) 2. XX The entry to accrue interest revenue at the end of the accounting period is: Interest Receivable Interest Revenue XX XX 3. The entry to record collection of the note and interest revenue on the maturity date is: Cash XX Note Receivable Interest Receivable Interest Revenue XX XX XX C. A company holding a note receivable may sell the note before its maturity date; this is referred to as discounting a note receivable. Refer to the appendix to the chapter for further explanation. D. If a note receivable is not paid at maturity, the maker of the note is said to dishonor or default on the note. The payee records interest revenue earned on the note and debits Accounts Receivable for the full maturity value of the note: Accounts Receivable Note Receivable Interest Revenue XX XX XX Objective 5: Report receivables on the balance sheet A. A business usually reports its accounts receivable at net realizable value and discloses the allowance account parenthetically. B. Alternately, the firm may report net realizable value for receivables on the balance sheet and include details in the footnotes. C. In many large companies, computers aid in accounting for receivables. Exhibit 9-5 illustrates the integration of order entry, shipping, and billing for M&M Mars. Objective 6: Use the acid-test ratio and days’ sales in receivables to evaluate a company A. Key ratios can help managers and owners make decisions about the liquidity of a business. B. On the balance sheet, cash is always listed first because it is the most liquid asset; cash is followed by short-term investments, then current receivables, then inventory. C. The balance sheet in Exhibit 9-6 is used to illustrate the two ratios: acid-test and days’ sales in receivables. 1. The acid-test (or quick) ratio measures a company’s ability to pay current liabilities. In general, an acid-test ratio of 1.0 is considered safe. The computation is: Acid-test ratio = 2. C. Cash + Short-term investments + Net current receivables Total current liabilities The days’ sales in receivables (or collection period) indicates how many days it takes to collect the average level of receivables. The number of days should be very near the days in the credit period. There are two steps to the computation: a. One day’s sales = b. Days’ sales in average accounts receivable Net sales 365 days = Average net accounts receivable One day’s sales A meaningful analysis of financial information is best achieved by calculating many ratios over a number of years. D. Decision Guidelines summarize the accounting for receivables and using ratios related to receivables. Appendix to Chapter 9: A. Notes receivable may be discounted (or sold) by the payee for cash prior to maturity date. 1. Often, present value calculations are used to determine the discounted price of a note receivable that is sold to a bank prior to maturity. 2. The bank calculates the interest (or discount) based on the maturity value of the note, the bank’s holding period, and the bank’s discount rate. 3. The maturity value less the bank’s discount equals the proceeds or discounted value. 4. The payee records receipt of the proceeds of a discounted note with this entry: Cash (proceeds) Interest Expense Note Receivable 5. B. XX XX XX Note: the entry may instead require a credit to Interest Revenue (rather than a debit to Interest Expense) if the interest included in the maturity value is greater than the bank’s discount. The steps to discounting a note receivable are illustrated in Exhibit 9A-1.