Week 7 : Week 7 - Exam #1 Time Remaining: 1. What phrase is

advertisement

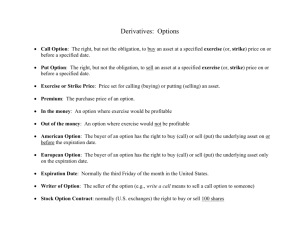

Week 7 : Week 7 - Exam #1 Time Remaining: 01:29:36 1. What phrase is often used interchangeably with the phrase market capitalization? (Points : 1) Market value Open Interest Trading volume Notional value 2. Assume that an investor lends 100 shares of Jiffy, Inc. common stock to a short seller. The bid-ask prices are $32.00 - $32.50. When the position is closed the bid-ask prices are $32.50 - $33.00. The commission rate is 0.5%. The market interest rate is 5.0% and the short rebate rate is 3.0%. Calculate the gain or loss to the lender. Assume the lender is not subject to a bid-ask loss or commissions. (Points : 1) $164.00 loss $100.00 gain $100.00 loss $164.00 gain 3. During the growing season a corn farmer sells short corn futures contracts in an amount equal to her crop. If upon harvesting and selling her crop she maintains the contracts, she is then considered a: (Points : 1) Speculator Arbitrager Hedger None of the above 4. What kind of risk does not disappear when spread across many investors? (Points : 1) Diversifiable Catastrophic Predictive Nondiversifiable 5. Who from the following list would be considered a speculator by entering into a futures or options contract on commodities?(Points : 1) Corn delivery truck driver Food manufacturer Farmer None of the above 6. Assume that you purchase 100 shares of Jiffy, Inc. common stock at the bid-ask prices of $32.00 - $32.50. When you sell the bid-ask prices are $32.50 - $33.00. If you pay a commission rate of 0.5%, what is your profit or loss? (Points : 1) $32.50 loss $16.25 loss $0 $32.50 gain 7. Which of the following is not a derivative instrument? (Points : 1) Installment sales agreement Option agreement to buy land Contract to sell corn Mortgage backed security 8. According to trading volume data tabulated for 2002, which international futures exchange market experienced the highest total trading volume in the world? (Points : 1) Chicago Board of Trade Chicago Mercantile Exchange New York Mercantile Exchange Eurex 9. All of the following are financially engineered products, except: (Points : 1) Mortgage backed security Principal only Mortgage Interest only 10. What phrase might be used to describe the initial transaction a short seller initiates when shorting an equity security? (Points : 1) Covering Buy Sell Borrow 11. The total number of contracts which exist and are delivery or payment is referred to as the ___________________. (Points : 1) Market value Notional value Trading volume Open Interest 12. This measures the number of financial claims that change hands either daily or annually. (Points : 1) Open Interest Notional value Market value Trading volume 13. A mutual fund is engaged in the short term and temporary purchase of index futures, for purposes of minimizing its cash exposures. Which "use" most closely explains their actions? (Points : 1) Speculation Reduced transaction costs Regulatory arbitrage Risk management 14. Which of the following phrases is used to describe an option where immediate exercise results in a negative payoff? (Points : 1) At-the-money Near-the-money In-the-money Out-of-the-money 15. The premium on a long term call option on the market index with an exercise price of 950 is $12.00 when originally purchased. After 6 months the position is closed and the index spot price is 965. If interest rates are 0.5% per month, what is the Call Payoff?(Points : 1) $12.00 $15.00 $12.36 $2.64 16. The spot price of the market index is $900. The annual rate of interest on treasuries is 4.8% (0.4% per month). After 3 months the market index is priced at $920. An investor has a long call option on the index at a strike price of $930. What profit or loss will the writer of the call option earn if the option premium is $2.00? (Points : 1) $2.00 loss $2.00 gain $2.02 gain $2.02 loss 17. The spot price of the market index is $900. After 3 months the market index is priced at $920. The annual rate of interest on treasuries is 4.8% (0.4% per month). The premium on the long put, with an exercise price of $930, is $8.00. What is the profit or loss at expiration for the long put? (Points : 1) $1.90 gain $1.90 loss $2.00 gain $2.00 loss 18. Which type of option is least likely to be exercised? (Points : 1) In-the-money Near-the-money Out-of-the-money At-the-money 19. The spot price of the market index is $900. A 3-month forward contract on this index is priced at $930. The market index rises to $920 by the expiration date. The annual rate of interest on treasuries is 4.8% (0.4% per month). What is the difference in the payoffs between a long index investment and a long forward contract investment? (Assume monthly compounding) (Points : 1) $19.16 $26.40 $43.20 $10.84 20. The spot price of the market index is $900. After 3 months the market index is priced at $920. The annual rate of interest on treasuries is 4.8% (0.4% per month). The premium on the long put, with an exercise price of $930, is $8.00. At what index price does a long put investor have the same payoff as a short index investor? Assume the short position has a breakeven price of $930. (Points : 1) $940.00 $938.10 $930.00 $921.90 21. What term may be used to describe a long put position in which the exercise price is below the asset price? (Points : 1) At-the-money Out-of-the-money In-the-money Near-the-money 22. The spot price of the market index is $900. A 3-month forward contract on this index is priced at $930. The annual rate of interest on treasuries is 4.8% (0.4% per month). What annualized rate of interest makes the net payoff zero? (Assume monthly compounding) (Points : 1) 11.2% 13.2% 8.5% 4.8% 23. A put option if purchased and held for 1 year. The exercise price on the underlying asset is $40. If the current price of the asset is $36.45 and the future value of the original option premium is (- $1.62 ), what is the put profit, if any at the end of the year? (Points : 1) $1.62 $5.17 $1.93 $3.55 24. The premium on a call option on the market index with an exercise price of 1050 is $9.30 when originally purchased. After 2 months the position is closed and the index spot price is 1072. If interest rates are 0.5% per month, what is the Call Profit? (Points : 1) $12.61 $9.30 $9.39 $22.00 25. The spot price of the market index is $900. A 3-month forward contract on this index is priced at $930. What is the profit or loss to a short position if the spot price of the market index rises to $920 by the expiration date? (Points : 1) $20 loss $10 gain $20 gain $10 loss 26. Which strike price is reflective of an out-of- the-money long call with an asset price of $34? (Points : 1) $36 $32 $34 $38 27. Which of the following phrases is used to describe an option where immediate exercise results in a positive payoff? (Points : 1) Near-the-money Out-of-the-money At-the-money In-the-money 28. The spot price of the market index is $900. After 3 months the market index is priced at $920. The annual rate of interest on treasuries is 4.8% (0.4% per month). The premium on the long put, with an exercise price of $930, is $8.00. Calculate the profit or loss to the short put position if the final index price is $915. (Points : 1) $15.00 loss $6.90 gain $6.90 loss $15.00 gain 29. What strategy is an investor most likely to employ to insure against the losses associated with a straddle write? (Points : 1) Ratio call write Butterfly spread Bull spread Strangle 30. Which strategy is a bet that the actual volatility of an asset is low relative to the market's assessment? (Points : 1) Written straddle Purchased straddle Long Call Long Put 31. What strategy is an investor most likely to employ to reduce the high premium cost associated with a strangle strategy?(Points : 1) Bull spread Butterfly spread Strangle Ratio call write 32. A strategy consists of buying a market index product at $830 and longing a put on the index with a strike of $830. If the put premium is $18.00 and interest rates are 0.5% per month, compute the profit or loss from the long put position by itself (in 6 months) if the market index is $810. (Points : 1) $1.36 loss $3.45 gain $1.45 gain $2.80 loss 33. A strategy consists of buying a market index product at $830 and longing a put on the index with a strike of $830. If the put premium is $18.00 and interest rates are 0.5% per month, compute the profit or loss from the long index position by itself expiration (in 6 months) if the market index is $810. (Points : 1) $18.00 gain $45.21 loss $21.22 loss $24.25 gain 34. What is the maximum profit that an investor can obtain from a strategy employing a long 830 call and a short 850 call over 6 months? Interest rates are 0.5% per month. (Points : 1) $12.32 $6.80 $9.24 $7.68 35. What is the maximum loss that an investor can obtain over 6 months from a strategy employing a long 830 call and a short 850 call? Interest rates are 0.5% per month. (Points : 1) $12.32 $7.68 $9.24 $6.80 36. Which of the following strategies represents a purchased put and a written call for which the premiums are equal? (Points : 1) Ratio call write Butterfly spread Bull spread Strangle 37. A strategy consists of buying a market index product at $830 and longing a put on the index with a strike of $830. If the put premium is $18.00 and interest rates are 0.5% per month, what is the profit or loss at expiration (in 6 months) if the market index is $810? (Points : 1) $18.65 gain $20.00 gain $36.29 loss $43.76 loss 38. A strategy consists of buying a market index product at $830 and longing a put on the index with a strike of $830. If the put premium is $18.00 and interest rates are 0.5% per month, what is the estimated price of a call option with an exercise price of $830? (Points : 1) $49.55 $47.67 $42.47 $45.26 39. At the 6-month point, what is the breakeven index price for a strategy of longing the market index at a price of 830? Interest rates are 0.5% per month. (Points : 1) $855.21 $830.00 $866.32 $802.12 40. A strategy consists of longing a put on the market index with a strike of 830 and shorting a call option on the market index with a strike price of 830. The put premium is $18.00 and the call premium is $44.00. Interest rates are 0.5% per month. What is the breakeven price of the market index for this strategy at expiration (in 6 months)? (Points : 1) $830.00 $866.32 $855.21 $802.12 41. A position in which you buy a call and sell an otherwise identical call with a higher strike price is called a ________. (Points : 1) Butterfly spread Ratio call write Bull spread Strangle 42. The $850 strike put premium is $25.45 and the $850 strike call is selling for $30.51. Calculate the breakeven index price for a strategy employing a short call and long put that expires in 6 months. Interest rates are 0.5% per month. (Points : 1) $822.67 $824.79 $875.82 $830.76 43. What is the break even point that an investor can obtain from a 6-month strategy employing a long 830 call and a short 850 call? Interest rates are 0.5% per month. (Points : 1) $832.82 $852.22 $862.92 $842.32 44. Which of the following strategies is the appropriate one if you have no view on the stock-price direction and you think volatility will fall? (Points : 1) Buying puts Selling the underlying Buying calls Writing a straddle 45. An investor purchases a call option with an exercise price of $55 for $2.60. The same investor sells a call on the same security with an exercise price of $60 for $1.40. At expiration, 3 months later, the stock price is $56.75. All other things being equal and given an annual interest rate of 4.0%, what is the net profit or loss to the investor? (Points : 1) $0.54 gain $1.21 loss $1.50 loss $1.65 gain 46. Which of the following strategies is the appropriate one if you are bullish about the stock-price direction and you think volatility will increase? (Points : 1) Buying puts Selling the underlying Buying calls Buying straddle 47. As a writer of a straddle position, how would you insure against large losses? (Points : 1) Buying an out-of-the-money put and buying an out-of-the-money call Buying an in-the-money put and selling an out-of-the-money call Selling an out-of-the-money put and buying an in-the-money call Selling an out-of-the-money put and selling an out-of-the-money call 48. An insured asset position is equivalent to: (Points : 1) -Zero-coupon bond - call -Zero-coupon bond + put Zero-coupon bond - put Zero-coupon bond + call 49. Which of the following strategies is not a volatility play? (Points : 1) Straddle Strangle Bull spread Butterfly spread 50. Assume that you open a 100 share short position in Jiffy, Inc. common stock at the bid-ask prices of $32.00 - $32.50. When you close your position the bid-ask prices are $32.50 - $33.00. You pay a commission rate of 0.5%. The market interest rate is 5.0% and the short rebate rate is 3.0%. What is your additional gain or loss due to leasing the asset? (Points : 1) $96 gain $160 loss $64 loss $64 gain Time Remaining: 01:29:36