Chapter 2_MH

advertisement

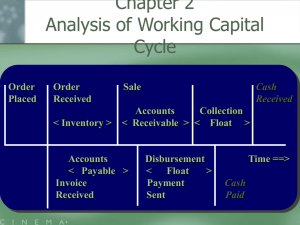

SHORT-TERM FINANCIAL MANAGEMENT Chapter 2 – Analysis of the Working Capital Cycle Prepared by Patricia R. Robertson Kennesaw State University 2 Chapter 2 Agenda ANALYSIS OF THE WORKING CAPITAL CYCLE Differentiate between solvency ratios and the cash conversion period, distinguish between solvency and liquidity, calculate and interpret the cash conversion period, and determine the change in shareholder wealth attributable to changes in the cash conversion period. Cash Flow Timeline 3 The cash conversion period is the time between when cash is received versus paid. The shorter the cash conversion period, the more efficient the firm’s working capital. The firm is a system of cash flows. These cash flows are unsynchronized and uncertain. Solvency v. Liquidity 4 A firm is solvent when its assets exceed its liabilities. This accounting measure is based on book, not market, values. A firm is liquid when it can pay its bills on time without undue cost. Solvency Measures 5 The following ratio measures are generally referred to as liquidity measures but, in fact, measure solvency. Net Working Capital Net Liquid Balance Working Capital Requirements Working Capital Requirements / Sales Current Ratio Quick Ratio Net Working Capital 6 Net Working Capital is a dollar-based solvency measure. The larger the amount, the more solvent the firm. It is an absolute, not relative measure, so it ignores scale and trends. Too much working capital is considered a drag on financial performance. Like the current ratio, it can be overstated based on uncollectible receivables and obsolete inventory. Some analysts exclude cash from the ratio to measure the amount of cash tied up in the operating cycle. Net Working Capital = Current Assets – Current Liabilities WCR & NLB 7 Net Working Capital commingles operating and financial accounts. A variation separates Net Working Capital into two pieces: Working Capital Requirements (WCR) Operating CA – Operating CL Net Liquid Balance (NLB) Financial CA – Financial CL Shows ability of stock resources to pay ‘arranged’ maturing debt which is unaffected by the operating cycle. Net Working Capital = WCR + NLB WCR & NLB 8 Working Capital Requirements (WCR) Net Working Capital Current Assets Minus Current Liabilities Current Assets Minus Current Liabilities Cash Accounts Payable Cash Accounts Payable Marketable Securities Notes Payable Marketable Securities Notes Payable Accounts Receivable CMLTD Accounts Receivable CMLTD Inventory Accruals and Other Inventory Accruals and Other Prepaids and Other Prepaids and Other Net Working Capital = WCR + NLB If positive, a portion of Current Assets is financed with ‘permanent funds’ (LT Liabilities and Equity). If negative, a portion of Current Liabilities are funding long-term. Net Liquid Balance (NLB) Current Assets Minus Current Liabilities Cash Accounts Payable Marketable Securities Notes Payable Accounts Receivable CMLTD Inventory Accruals and Other Prepaids and Other WCR & NLB / WCR/S 9 The level of WCR will change as sales expand and contract. WCR/S = WCR in relative terms (% of sales) During expansion, higher levels of WCR must be financed by: Drawing down NLB. Appropriate for seasonal sales increases. Adding to permanent working capital by acquiring new LTD, equity, or both. Appropriate for sustainable sales increases. Current Ratio 10 The Current Ratio indicates the degree of coverage provided to short-term (ST) creditors if ST assets were to be liquidated. A ratio of 2.00 indicates the firm has $2.00 of Current Assets for $1.00 of Current Liabilities. It does not consider the ‘going-concern’ aspect of the firm, which assumes the firm would have to liquidate these assets to pay off the liabilities. Plus, it is only a point in time, and not always representative. Its use is limiting based on the components (firm might have a high ratio due to large balance of uncollectible receivables and/or obsolete inventory). Quick Ratio 11 Also known as the Acid-Test Ratio, the Quick Ratio excludes inventory in the numerator since inventory is the least liquid current asset. Quick Ratio = Current Assets - Inventory Current Liabilities Inventory could be obsolete, stolen, worn (damaged), or non-saleable (unless deeply discounted at a fire-sale price). Prepaid Expenses are also commonly excluded. What Is Liquidity? 12 Elements of liquidity include several dimensions: Time The amount of time to convert an asset to cash. The quicker, the more liquid the firm. Amount Cost / Loss of Value The firm’s capacity to meet its ST obligations. Assets can be quickly converted to cash with little/no cost. A liquid firm has enough financial resources to cover its financial obligations in a timely manner with minimal cost. Cash Conversion Period 13 We are concerned with the amount and timing of cash flows. We have to build and sell products, then get paid before we generate cash inflows. In the meantime, we have cash outflows for supplies and labor. This creates the Cash Conversion Period (CCP), the elapsed time between payment to suppliers and receipt of customer payments. CCP = Production Cycle + Collection Cycle – Payment Cycle 14 CCP and Activity Measures 15 Calculation of the Cash Conversion Period (CCP) relies on three activity measures. Activity measures indicate how efficiently the firm is using its assets. Days Inventory Held (DIH) Days Sales Outstanding (DSO) Inventory Turnover Receivables Turnover Days Payables Outstanding (DPO) Payables Turnover Cash Conversion Period (CCP) 16 Days Inventory Held (DIH) measures inventory management by calculating the average length of time inventory is in stock before being sold. DIH Note: Using average inventory is a more accurate calculation. DSO DPO Days Inventory Held = Inventory Cost of Sales / 365 Cash Conversion Period (CCP) 17 Days Sales Outstanding (DSO) measures credit / collections management by calculating the average time to collect from customers. Note: Using DIH average net receivables is a more accurate calculation. Using credit sales in the denominator also offers a superior result (excludes cash sales). DSO DPO Days Sales Outstanding = Receivables Sales / 365 Cash Conversion Period (CCP) 18 Days Payables Outstanding (DPO) measures payables management by calculating the average time from inventory receipt to payment. DIH Note: Using average payables is a more accurate calculation. DSO DPO Days Payables Outstanding = Payables Cost of Sales / 365 Cash Conversion Period (Cycle) 19 Three Activity Measures explain the CCP: Days Inventory Held (DIH) Days Sales Outstanding (DSO) Days Payables Outstanding (DPO) CCP = [Production Cycle + Collection Cycle] – Payment Cycle CCP = Operating Cycle – Payment Cycle Operating Cycle = DIH + DSO Payment Cycle = DPO CCP = (DIH + DSO) – DPO Cash Conversion Period (CCP) 20 The CCP is generally positive; the longer the CCP the more financing is required for inventory and receivables. A lengthening cycle could signal liquidity issues. DIH DPO DSO CCP Example 21 A firm has a CCP of 87 days. The CCP includes DIH of 50 days. By changing inventory policies, it believes it can reduce DIH by 5 days. How does this change the firm’s investment in inventory, assuming the firm has $500M in sales and CGS of 40%? CCP Example 22 How does reducing DIH from 50 to 45 days change the firm’s inventory investment. Cost of Working Capital 23 Let’s first establish the cost of working capital. Assume a firm offers standard 30-day credit terms (it gets paid for sales 30-days after the sale is made). Assuming average daily sales are $200,000 and the cost of capital is 10%, what is the annual cost of extending trade credit? 30 × $200,000 × 10% = $600,000 The firm has permanently lost the use of $6,000,000 (it has permanently committed this amount in capital to support A/R). At a 10% cost of capital, the cost of extending credit is $600,000; in other words, in the absence of offering trade credit, the $6,000,000 could be otherwise used to generate $600,000 in incremental firm value. Valuation of ST Cash Flows 24 Each component of working capital (inventory, receivables, payables, accruals) has two dimensions…time and amount. Cash flows can be converted to a value at a standard point in time (usually t = 0) so they can be compared. For example, to increase sales, a firm is considering modifying its credit terms from net 30 to net 45 days. What is the impact on the value of one day’s sales? Firm’s Decision 25 Shown is how the cash flows compare. Net 30: 0 Does this decision make sense? Since the amounts and timing of the cash flows are different, how can they be compared? 30 Days $550,000 Net 45: 0 45 Days $600,000 Valuation of ST Cash Flows 26 It might seem that valuing intra-year year cash flows is not meaningful. However, financial policy decisions that are permanent are meaningful. ST financial decisions can impact firm value by: Altering operating cash flows (amount). Changing the length of the cash conversion cycle period (timing). Changing the company’s risk posture. Impacting interest income (or interest expense). Valuation of ST Cash Flows 27 A widely-used valuation method is the Net Present Value (NPV) approach. This approach is preferred since it accounts for the timing and risk of cash flows. There are four steps: Determine the relevant cash flows. Determine the timing of the cash flows. Determine the appropriate discount rate. Discount the cash flows to compute NPV. Choose the result that optimizes VALUE. Valuation (NPV) Approach 28 Firm XYZ is considering modifying its credit terms from net 30 to net 60. Relaxing the credit terms and giving customers more time to pay is expected to increase sales. What is the NPV of this decision? First, let’s recall how to discount money (calculate the present value of future cash flows). Discounting ST Cash Flows 29 Other finance classes emphasize the importance of compounding in financial analysis. While this is meaningful for long-term (LT) decisions, simple interest calculations are adequate for ST decisions. While the timing of intra-year cash flows is significant, the effect of compounding is not. We will often use a daily interest rate since firms invest in overnight investments or borrow money on credit lines daily. Quick TVM Review 30 To calculate PV using simple interest, the formula is: PV = FV / [1 + (i)(n)] Where i = annual opportunity cost and n = # of years i and n can be adjusted to reflect different periods To modify the formula for a daily periodic interest rate: PV = FV / [1 + [(i)(n/365)]] Annual rate times portion of year or… PV = FV / [1 + [(i/365)(n)]] Daily rate times # of days Choosing the Discount Rate (i) 31 Throughout the course, we will refer to i as: The annual interest rate The discount rate The opportunity cost of funds or capital The required rate of return The investment opportunity rate The annual cost of capital Choosing the Discount Rate (i) 32 i is the rate of return the firm should earn on its assets It is the Opportunity Cost; tying up funds in one or more assets (like current assets) prevents the firm from using those resources for the most valuable alternative, which is usually reinvestment in the firm. Simple vs. Compound Interest 33 Before we move on, let’s compare simple and compound interest to ensure you agree the difference is not material intra-year… Using the example from before…. Let’s assume a firm has standard 30-day credit terms, has average daily sales of $200,000, and a cost of capital of 10%... The Difference is Negligible 34 i = annual cost of capital Simple Interest PV = PV = PV = PV = FV 1 + (n x i ) FV i 1 + (n х /365) $200,000 1 + (30 х 0.10 /365) $198,369.57 n = number of days Compound Interest PV = PV = PV = PV = FV (1 + i ) n FV i (1 + / 365 ) n $200,000 (1 + 0.10/ 365 )30 $198,363.12 NPV With Daily Simple Interest 35 If this formula is true for a single cash flow: FV PV = 1 + (i х n ) This is the expanded formula for a series of cash flows: i = annual rate n = number of periods CF1 CF2 NPV = CF0 + + + 1 + (i х n 1 ) 1 + (i х n 2 ) … CFn + 1 + (i х n n ) NPV Simplification 36 However, many ST financial decisions can be made based on a single cash flow if it has multi-year effects. FV PV = 1 + (i х n ) So, one of the steps in the analysis is to determine if the cash flows are constant and can be represented with a single sum. If the change is permanent (a perpetuity), the aggregate impact can be calculated since the benefit will continue indefinitely. PV Perp = If not, it is an annuity. CF i = Cash Flow Per Period Interest Rate Per Period Valuation (NPV) Approach 37 Back to the decision… Firm XYZ is considering modifying its credit terms from net 30 to net 60. Relaxing the credit terms and giving customers more time to pay is expected to increase sales. The Valuation Approach (NPV) compares the cash flows (amount and timing) of a proposed policy change, including any funding costs, to the cash flows from the existing policy. There are rarely any fixed costs or fixed asset changes. Consider only the relevant cash flows. Firm XYZ’s Decision PV = FV 1 + (i х n ) 38 First, let’s observe the timeline based on the current credit policy. Presented is the cash flow timeline at net 30 and the PV of one day’s sales using a discount rate of 10%. Present sales data: $36,500,000 annual sales $36,500,000 / 365 = $100,000 / day Cash Flow Timeline (net 30) 0 30 Days $100,000 This is a DAILY NPV…it recurs every day. PV = $100,000 1 + (.10 х 30/365) PV = $99,184.78 Firm XYZ’s Decision PV = FV 1 + (i х n ) 39 Now assume the proposed net 60 is adopted. Presented is the cash flow timeline at net 60 and the PV of one day’s sales using a discount rate of 10%. We didn’t change the amount of the cash flows; but, we did change the TIMING, lengthening the Cash Conversion Period. Sales: $36,500,000 $36,500,000 / 365 = $100,000 / day Cash Flow Timeline (net 60) 0 PV = PV = 30 60 Days $0 $100,000 $100,000 1 + (.10 х 60/365) $98,382.75 Without a corresponding increase in sales, the policy change would cost the firm $802.03/day, or $292,741/year. Firm XYZ’s Decision PV = FV 1 + (i х n ) 40 Now assume sales do increase. As sales increase, many costs also change. To make the comparison, we need to FIRST look at ALL relevant present vs. proposed cash flows. Remember, we are concerned with all relevant cash flows. Here, since the timing and/or amounts of cash inflows AND cash outflows are impacted, all are relevant. NPV = PV of Inflows - PV of Outflows Firm XYZ’s Decision PV = FV 1 + (i х n ) 41 Now assume sales do increase. As sales increase, many costs also change. To make the comparison, we need to FIRST look at ALL relevant present vs. proposed cash flows. Present Cash Flows: Initial Investment Sales Increase CGS Payment Terms From Supplier Inventory Conversion: $0 + 3% (even) 65% of Sales Net 30 (DPO) Inventory-to-Production Lag Production-to-Sales Lag 30 Days 10 Days 40 Days DIH Raw Materials Purchased & Received Goods Produced; Pay For Materials Product Sold Sales Proceeds Received 0 30 40 70 Days $65,000 Inv.-toProd. Lag Prod.to-Sales Lag $100,000 Payment Terms (DSO) Firm XYZ’s Decision PV = FV 1 + (i х n ) 42 The daily NPV is the difference between the PV of the inflows and outflows. Raw Materials Purchased & Received Goods Produced; Pay For Materials Product Sold Sales Proceeds Received 0 30 40 70 Days $65,000 $100,000 Inflows PV = PV = Daily NPV = Outflows $100,000 1 + (.10 х 70 /365) $98,118.28 $98,118.28 -$64,470.11 $33,648.17 PV = PV = $65,000 1 + (.10 х 30 /365) $64,470.11 Firm XYZ’s Decision PV = FV 1 + (i х n ) 43 The calculated daily NPV is converted to the aggregate NPV since it is assumed that the daily NPV would persist indefinitely (here, use i in the denominator). Inflows PV = PV = Daily NPV = Outflows $100,000 1 + (.10 х 70 /365) $98,118.28 $98,118.28 -$64,470.11 $33,648.17 PV = PV = $65,000 1 + (.10 х 30 PVPerp = CF i PVPerp = $33,648.17 (.10/365) PVPerp = $33,648.17 0.000273973 PVPerp = $122,815,820.50 /365) $64,470.11 Firm XYZ’s Decision PV = FV 1 + (i х n ) 44 Net 30: We now compare the previous results to the proposed change to net 60. Shown is how the cash flows compare. THE AMOUNT AND TIMING OF CASH FLOWS CHANGES. Raw Materials Purchased & Received 0 Goods Produced; Pay For Materials Product Sold 30 40 $65,000 Net 60: Raw Materials Purchased & Received 0 $66,950 $103,000 х 65% 70 Days $100,000 Goods Produced; Pay For Materials Product Sold 30 Payment Terms (DSO) Sales Proceeds Received 40 Payment Terms (DSO) Sales Proceeds Received 100 Days $103,000 $100,000 х 1.03 Firm XYZ’s Decision PV = FV 1 + (i х n ) 45 We now compute the cash flow effect from the proposed change to net 60. Raw Materials Purchased & Received Goods Produced; Pay For Materials Product Sold 0 30 40 Sales Proceeds Received 100 Days $66,950 $103,000 Inflows PV = PV = Daily NPV = Outflows $103,000 1 + (.10 х 100 /365) $100,253.33 $100,253.33 -$66,404.21 $33,849.12 PV = PV = $66,950 1 + (.10 х 30 /365) $66,404.21 Firm XYZ’s Decision PV = FV 1 + (i х n ) 46 Again, the calculated daily NPV is converted to the aggregate NPV since it is assumed that the daily NPV would persist indefinitely. Inflows PV = PV = Daily NPV = Outflows $103,000 1 + (.10 х 100 /365) $100,253.33 $100,253.33 -$66,404.21 $33,849.12 PV = PV = PVPerp = CF i PVPerp = $33,849.12 (.10/365) PVPerp = $33,849.12 0.000273973 PVPerp = $123,549,288.00 $66,950 1 + (.10 х 30 /365) $66,404.21 Firm XYZ’s Decision 47 Evaluate the results and make a decision. Choose the project with the highest NPV: $123,549,288 > $122,815,821 $123,549,288 - $122,815,821 > 0 Changing the terms [permanently] increases CASH and the VALUE of this transaction. The delay in receiving the cash is more than offset by the value of the increased sales. So, change the terms to net 60. Note: If there is reason to believe that the cash flow effect will only last several years, modify the analysis to an annuity versus a perpetuity. A Word of Caution… 48 Regarding the formula… [1 + (i)(n/365)] ≠ [1 + (i)](n/365) A Word of Caution… 49 Discounting the cash flows is the step that considers the timing of the cash flows. Typically, you use a daily periodic rate. FV PV = 1 + (i х n ) Once you have the PV (and assuming you consider it a perpetuity), the denominator in the following formula is based on the frequency of the occurrence of the cash flows, not the change in the cash conversion cycle. PV Perp = CF i = Cash Flow Per Period Interest Rate Per Period Use appropriate periodic rate that matches the frequency of the cash flows. A Word of Caution… 50 For example, if you have a daily NPV of $75,000 and the cost of funds is 10%, the perpetuity (aggregate) value of the transaction is: $75,000 / (.10 / 365) = $273,750,000 If the $75,000 occurred monthly: $75,000 / (.10 / 12) = $9,000,000 This is the same thing as annualizing the benefit and then dividing it by the annual rate: ($75,000 x 365) / .10 = $273,750,000 ($75,000 x 12) / .10 = $9,000,000 Another Word of Caution… 51 When evaluating the result of a NPV calculation, remember if it is an inflow or an outflow: If you are evaluating accounts receivables (an inflow), you want the higher NPV. If you are evaluating inventory costs and/or paying for that inventory (accounts payables, which is an outflow), you want the lower NPV. If you are evaluating a situation that includes both inflows and outflows, you want the higher NPV. The Importance of Cash 52 Why is more cash sooner a good thing? Firms can reinvest cash in the firm (new equipment, more inventory, more warehouse space, etc.). It can finance operations and sales growth internally without having to rely on external financing. Firms can borrow less or invest more.