Accounting

Principles

Second Canadian Edition

Weygandt · Kieso · Kimmel · Trenholm

Prepared by:

Carole Bowman, Sheridan College

CHAPTER

19

FINANCIAL STATEMENT

ANALYSIS

BASICS OF

FINANCIAL STATEMENT ANALYSIS

• Analysing financial statements involves

evaluating three characteristics of a

company:

1. its liquidity

2. its profitability

3. its solvency

COMPARATIVE ANALYSIS

• Three types of

comparisons:

– Intracompany basis

– Intercompany basis

– Industry averages

COMPARATIVE ANALYSIS

• Three tools:

– Horizontal analysis

– Vertical analysis

– Ratio analysis

HORIZONTAL ANALYSIS

Change

since base

period

Current year amount — Base year amount

———————————————————————

Base year amount

ANY COMPANY INC.

Assumed Net Sales

For the Year Ended December 31 (in millions)

2003

2002

2001

2000

1999

$ 6,562.8

$ 6,295.4

$ 6,190.6

$ 5,786.6

$ 5,181.4

121%

119%

112%

100%

127%

VERTICAL ANALYSIS

• Expresses each item in a financial statement as a

percent of a base amount (total assets or net

sales)

ANY COMPANY, INC.

Condensed Balance Sheets (Partial)

December 31 (in millions)

Assets

Current assets

Capital assets

Other assets

Total assets

2002

Amount

$1,496.5

2,888.8

666.2

$5,051.5

Percent

29.6

57.2

13.2

100.0%

2001

.

Amount

Percent

$1,467.7

30.1

2,733.3

56.9

636.6

13.0

$4,837.6

100.0%

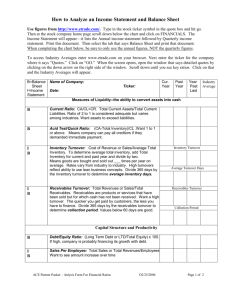

RATIO ANALYSIS

Liquidity Ratios

Measure short-term ability

of the enterprise to pay its

maturing obligations and to

meet unexpected needs for

cash.

Profitability Ratios

Revenues

-

Expenses

Since 1892

=

Net

Income

Measure the income or

operating success of an

enterprise for a given period

of time.

Solvency Ratios

XYZ

Co.

Measure the ability of the

enterprise to survive over a

long period of time.

LIQUIDITY RATIOS

•

•

•

•

•

•

•

Current ratio

Acid test ratio

Cash current debt coverage ratio

Receivables turnover

Collection period

Inventory turnover

Days sales in inventory

CURRENT RATIO

• Measures short-term debt-paying ability

Current ratio =

Current assets

Current liabilities

(Discussed in Chapter 4)

ACID TEST RATIO

• Measures immediate short-term debtpaying ability

Acid test ratio =

Cash + temporary investments + net receivables

Current liabilities

(Discussed in Chapter 9)

CASH CURRENT DEBT

COVERAGE RATIO

• Measures short-term debt-paying ability

(cash basis)

Cash current debt coverage ratio =

Cash provided by operating activities

Average current liabilities

(Discussed in Chapter 18)

RECEIVABLES TURNOVER

• Measures liquidity of receivables

Receivables turnover =

Net credit sales

Average net receivables

(Discussed in Chapter 9)

COLLECTION PERIOD

• Measures number of days receivables are

outstanding

Collection period =

365 days

Receivables turnover

(Discussed in Chapter 9)

INVENTORY TURNOVER

• Measures liquidity of inventory

Inventory turnover =

Cost of goods sold

Average inventory

(Discussed in Chapter 5)

DAYS SALES IN INVENTORY

• Measures number of days inventory is on

hand

Days in inventory =

365 days

Inventory turnover

(Discussed in Chapter 5)

PROFITABILITY RATIOS

•

•

•

•

•

•

Profit margin

Gross profit margin

Cash return on sales

Asset turnover

Return on assets

Return on common

shareholders’ equity

•

•

•

•

•

•

Book value per share

Cash flow per share

Earnings per share (EPS)

Price-earnings (PE) ratio

Payout ratio

Dividend yield

PROFIT MARGIN

• Measures net income generated by each

dollar of sales

Profit margin =

Net income

Net sales

(Discussed in Chapter 5)

GROSS PROFIT MARGIN

• Measures margin between selling price

and cost of goods sold generated by each

dollar of sales

Gross profit margin =

Gross profit

Net sales

(Discussed in Chapter 5)

CASH RETURN ON SALES

• Measures net cash flow generated by

each dollar of sales

Cash return on sales =

Net cash provided by operating activities

Net sales

(Discussed in Chapter 18)

ASSET TURNOVER

• Measures how efficiently assets are used

to generate sales

Asset turnover =

Net sales

Average total assets

(Discussed in Chapter 10)

RETURN ON ASSETS

• Measures overall profitability of assets

Return on assets =

Net income

Average total assets

(Discussed in Chapter 10)

RETURN ON COMMON

SHAREHOLDERS’ EQUITY

• Measures profitability of common

shareholders’ investment

Return on common shareholders’ equity =

Net income

Average common shareholders’ equity

(Discussed in Chapter 14)

BOOK VALUE PER SHARE

• Measures the equity (net assets) per

common share

Book value per share =

Common shareholders’ equity

Number of common shares

(Discussed in Chapter 14)

CASH FLOW PER SHARE

• Measures the net cash flow per common

share

Cash flow per share =

Net cash provided by all activities

Number of common shares

(Discussed in Chapter 18)

EARNINGS PER SHARE (EPS)

• Measures net income earned on each

common share

Earnings per share =

Net income

Number of common shares

(Discussed in Chapter 15)

PRICE-EARNINGS (PE) RATIO

• Measures relationship between market

price per share and earnings per share

Price-earnings ratio =

Share price

Earnings per share

(Discussed in Chapter 15)

PAYOUT RATIO

• Measures % of earnings distributed in

the form of cash dividends

Payout ratio =

Cash dividends

Net income

(Discussed in Chapter 15)

DIVIDEND YIELD

• Measures rate of return earned from

dividends

Dividend yield =

Cash dividends per share

Share price

(Discussed in Chapter 15)

SOLVENCY RATIOS

•

•

•

•

Debt to total assets

Interest coverage

Cash interest coverage

Cash total debt coverage

DEBT TO TOTAL ASSETS

• Measures % of total assets provided by

creditors

Debt to total assets =

Total liabilities

Total assets

(Discussed in Chapter 16)

INTEREST COVERAGE

• Measures ability to meet interest

payments as they come due

Interest coverage =

Income before interest expense

and income tax expense (EBIT)

Interest expense

(Discussed in Chapter 16)

CASH INTEREST COVERAGE

• Measures cash available to meet interest

payments as they come due (cash basis)

Cash interest coverage =

Income before interest expense, income tax

expense, and amortization expense (EBITDA)

Interest expense

(Discussed in Chapter 16)

CASH TOTAL DEBT COVERAGE

• Measures long-term debt-paying ability

(cash basis)

Cash total debt coverage ratio =

Net cash provided by operating activities

Average total liabilities

(Discussed in Chapter 18)

LIMITATIONS OF FINANCIAL

ANALYSIS

• Estimates

• Historical cost

• Alternative

accounting

methods

• Atypical data

• Diversification

COPYRIGHT

Copyright © 2002 John Wiley & Sons Canada, Ltd. All rights reserved.

Reproduction or translation of this work beyond that permitted by

CANCOPY (Canadian Reprography Collective) is unlawful. Request for

further information should be addressed to the Permissions Department,

John Wiley & Sons Canada, Ltd. The purchaser may make back-up copies

for his / her own use only and not for distribution or resale. The author and

the publisher assume no responsibility for errors, omissions, or damages,

caused by the use of these programs or from the use of the information

contained herein.