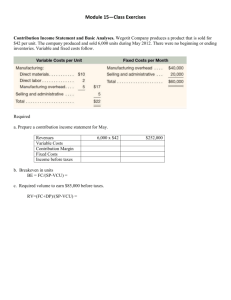

Contribution Margin per Unit

Chapter 6

Cost-Volume-Profit Analysis

©2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Introduction

Cost-volume-profit (CVP) analysis focuses on the following factors:

1.The

prices of products or services

2.The

volume of products or services produced and sold

3.The per-unit variable costs

4.The total fixed costs

5.The mix of products or services produced

CVP Analysis Assumptions

Major assumptions of CVP analysis include:

1

Selling price is constant throughout the entire relevant range.

2

Costs are linear throughout the relevant range.

3

Sales mix to calculate the weighted-average contribution margin is constant.

4

The amount of inventory is constant.

Comparison of Income Statements

TRADITIONAL

Sales

Less: Cost of Goods Sold:

Variable Costs

Fixed Costs

$350

150

$1,000

Total Cost of Goods Sold

Gross Profit

Less: S, G, & A Costs:

Variable Costs

Fixed Costs

Total S, G, & A Costs

Net Operating Income

$ 50

250

$ 500

$ 500

300

$ 200

CONTRIBUTION MARGIN

Sales

Less: Variable Costs:

Manufacturing

Costs

S, G, & A Costs

Total Variable Costs

$350

50

Contribution Margin

Less: Fixed Costs:

Manufacturing Costs $150

S, G, & A Costs

Total Fixed Costs

250

Net Operating Income

$1,000

$ 400

$ 600

400

$ 200

Contribution Margin Per Unit

Happy

Daze

Game Co.

Contribution margin (per unit) =

Contribution margin (in $)/Units sold

= $28,000/8,000 = $3.50

Sales (8,000 units)

Less: Variable Costs

Contribution Margin

Less: Fixed Costs

Total Contribution

Margin Per

$100,000 unit

$12.50

72,000

$ 28,000

35,000

Net Operating Income (Loss) $ (7,000)

9.00

$3.50

Contribution Margin Ratio

Contribution Margin (in $)

Sales (in $)

Total

Sales (8,000 units) $100,000

Less: Variable Costs 72,000

Contribution Margin $ 28,000

Less: Fixed Costs 35,000

Net Operating Income (Loss) $ (7,000)

Happy Daze’s

Contribution Margin =

$28,000

$100,000

= 28%

Applying the

Contribution Margin Ratio

For every dollar change in sales, contribution margin will increase or decrease by the contribution margin ratio multiplied by the increase or decrease in sales dollars.

If Sales Decrease

Sales Dollar Decrease

200 units x $12.50

x

200 units:

Contribution

Margin Ratio

=

Decrease in

Contribution

Margin and

Net

Operating

Income

$2,500 X

28% = $700

Considering Qualitative Factors

Companies must also consider qualitative factors when choosing options that affect its bottom line.

What if a less expensive supplier is less reliable or provides inferior quality material?

????

????

??

What if reducing labor causes more machine costs, trading variable costs for fixed costs ?

What if using inexperienced workers causes more defective products?

Break-Even Analysis

The break-even point is the level of sales at which contribution margin just covers fixed costs and consequently net operating income is equal to zero.

Break-Even

(units)

=

Fixed Costs

Contribution Margin Per Unit

Break-Even

(Sales $)

=

Fixed Costs

Contribution Margin Per Unit

Break-Even Graph

Break-Even Calculations for Multiple

Products

When more than one product is produced and sold, managers must calculate a

“weighted average” contribution margin for all products and estimate the sales mix.

Break-Even (Units) =

Fixed Costs

Weighted Average

Contribution Margin Per Unit

Relationship between Weighted-Average

Contribution Margin and Break-Even

Point

As Weighted-

Average

Contribution

Margin

INCREASES

The

Break-Even

Point will

DECREASE.

Target Profit Analysis

(Before and After Tax)

Sales volume

(to reach a target profit before tax)

Fixed Cost + Target Profit

(before tax)

=

Contribution Margin per Unit

The Impact of Taxes

It is also important to consider the payment of income taxes in the target profit formula.

If a company wants to earn $100,000 in target profit after taxes, and has a 35% income tax rate, what must its before-tax target profit be?

Before-tax Profit =

=

After-tax Profit

(1 – Tax Rate)

$100,000

(1 – 35%)

=

$153,846

(rounded)

Sales Volume to Reach an

After-Tax Target Profit

If a company has fixed cost of $35,000, a contribution margin per unit of $3.50, and desires an after-tax profit of $100,000, how many units must it sell?

Sales Volume to

Reach After-tax

Target Profit

=

=

Fixed Costs + Before-tax Profit

Contribution Margin per Unit

$35,000 + $153,846

$3.50

=

53,956 units

Cost Structure

Cost structure refers to the relative proportion of fixed and variable costs in a company.

% fixed costs

% variable costs

Operating Leverage

• The measure of the proportion of fixed costs in a company’s cost structure.

• It is used as an indicator of how sensitive profit is to changes in sales volume.

Operating

Leverage

=

Contribution Margin

Net Operating Income