financial accounting II statement analysis

advertisement

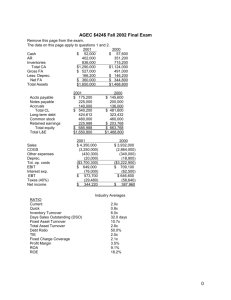

Slusher 1 Shelby Slusher Professor Shauna Hatfield April 26, 2015 Accounting 1120 Financial Statement Analysis We are going to be looking at International Machines of Business (IMB) financial statements to determine several thing, efficiency, profitability, ability to pay debt and stock investments. We will compare all the ratios we have calculated to the previous year and the industry average. By comparing the year before and industry averages to the current year we can see if they have grown or not as a company, it will help us determine if they are doing ‘better’ or ‘worse’. Let’s talk IBM’s profitability, which is their ability to utilize recourses to generate a profit. The ratios we will be looking at to determine their profitability are Profit Margin, Return on Assets, and Return on Equity. Profit Margin measures the company’s ability to control cost, a higher profit margin is better than a lower one. IBM’s Profit Margin is 12.96% for 2014 and 16.76% for 2013. They are well above the industry average which is 1.0%. This could mean that IBM has better control over how and where they spend money. Return on Equity measures how much revenue a company makes with what shareholders have invested, a higher percent means a higher growth rate in the company. Their Return on Equity 22.83% for 2014 and 31.95% for 2013, the industry average is 3.64%. IBM had a higher percent in 2013 than in 2014 which could Slusher 2 mean that more people were investing in 2013 than they were in 2014. They are above industry average which says that they have a higher percent of people investing in them. Overall IBM is more profitable than last year and the industry averages. Now let’s talk about efficiency which is how well a company can turnover inventory and make a profit. The ratios we will look at to analysis IBM’s efficiency are Days Sales Uncollected, Total Asset Turnover, Inventory Turnover, Days Sales in Inventory, and Receivables turnover. Let’s look at Days Sales Uncollected first which measures how long it takes a company to collect money for a good or service sold on credit. IBM’s Days Sales Uncollected for 2014 was 33.13 days and 30.05 days for 2013, the industry average is 62 days. IBM is well below industry average which means they are very efficient in collecting from customers who have a credit on their account. Total Assets Turnover measures how much revenue a company can generate with what assets they have on hand. A higher number is better because it tells you that the company can generate more revenue per asset dollar. The turnover for 2014 was .303 and .306 for 2013. IBM’s asset turnover was significantly lower than the industry average which is 1.6. This could mean that it takes longer for IBM to generate revenue from their assets. Inventory Turnover measures how fast a company can turnover their inventory, with inventory turnover you don’t want it to high or low, somewhere in between is the best. IBM’s rate were 4.8 in 2014 and 5.5 in 2013, they are below the industry average which is 17.56. IBM’s inventory turnover rate being so low means they could have a hard time selling their goods or have priced them to high for consumers to want to buy. Days Sales in Inventory measures how long it takes for the company to turn their inventory into revenue, usually the lower the number the better. In 2014 their rate was 82.43 and in 2013 it was 76.58. The increase in days could mean that they are having troubles selling their inventory for several reasons, they Slusher 3 aren’t marketing correctly, they have priced their product out of consumers’ price range. The industry average is 20.79 which is below what IBM’s rates are, which says the average company does a more efficient job at turning their inventory into revenue. The last ratio that we are going to look at that measures efficiency is Receivables turnover. It measures the number of times a company collects in accounts receivables. The industry average is 5.86, IBM rate is significantly lower in 2014 it was .28 and in 2013 it was .33, and these low numbers could mean that company has poor sells. Overall it looks like IBM could be more efficient with their money than they are. Now we are going to take a look at their ability to pay long term debt and current debt/ liabilities. We will look at our long term debt ratios first which are Debt ratio, Debt to Equity, and Times- Interest Earned. Debt Ratio measures how much assets you have per liability. The numbers for 2014 were 89.78% and 81.83% for 2013 which are relatively higher than the industry average which is at 59.3%. The high debt ratios for IBM could mean that they are raking in the debt and not paying it off. The Debt to Equity measure if the company can generate enough revenue to satisfy its debt, a lower debt to equity is better because it means they are less risky. In 2014 their numbers were 1.79 and in 2013 they were at 2.00, which is just slightly above the industry average at 1.46.This means that IBM is able to generate enough cash to pay debts off if need be. Times- Interest Earned measures the interest earned on debt and a company’s ability to repay it. The industry average was 2.9 and in 2014 IBM’s numbers 34.57 and 50.37 in 2013. These high rates for IBM could mean that they have too much debt and are trying to pay it down when they could be using that cash and investing it in projects or stocks. Now we will look at their ratios for current liabilities which measure how able a company is to pay off debt right then. Current Ratio measures the company’s ability to pay current liabilities with current assets. IBM’s current ratio was 1.25 in 2014 and 1.28 in 2013, which is just slightly Slusher 4 lower than the industry average at 1.86. Our last ratio we are going to look at for this section is the Acid-Test ratio which measure ability to pay off current liabilities, this need to be above 1 or they won’t be to pay off their current liabilities. In 2014 it was 1.02 and in 2013 it was 1.06 which means they can pay off their current liabilities. Overall IBM is able to pay their current and long term debts when they need too. Now we are going to look at cash flow which measure cash inflows. Cash Flow to Assets measures the cash flow from operating activities. The cash flow for 2014 was .13 and .14 in 2013 which is right where it needs to be. Cash flow per share measure the cash flow per share of stock, in 2014 it was 17.04 and in 2013 it was 16.59. It appears that they have increased their cash flow per share from the previous year. Price to Free Cash is 2.04 in 2014 and 2.44 in 2013 which means they were doing better in 2013. Overall they are doing very well with their cash flow and where it goes and how it is spent. Our last topics in on stock investments, the ratios are Dividend payout, Dividend yield, Price- earnings, and Dividends per share. Dividend per share measures what is being paid out per share of stock. The numbers for 2014 are 4.30 and the numbers for 2013 are 3.85, the increase in dividends per share means that they are having more people investing in their company. Priceearnings shows the earnings per price of each share of stock. In 2014 it was 13.65 and in 2013 it was 13.35, with this small increase it means that they are making more per stock and is lower than the industry average at 19.3. Dividend yield and dividend payout is how much is annually returned and how much is declared per share. Our numbers for Dividend yield are 21.33# in 2014 and 20.29% in 2013, the industry average is 2.2%. In 2014 for dividend payout it was 35.51% in 2014 and 24.57% in 2013 which is lower than the industry average at 42.1%. Overall Slusher 5 it looks like they are doing fairly average for their stock investments and from their stock investors. All in all it looks like IBM was more efficient, profitable, and had less debt. With all of this information that we went over it look like IBM will continue to grow and flourish as a company. They do better than most of the industry averages and have improved from their previous year. Slusher 6 2014 2013 industry average 41. Revenue per share 93.6357 93.3273 42. Gross marginal ratio 89.96% 88.81% 80.1% 43. Days sales uncollected 33.135 30.052 62 44. Total asset turnover .3034 .3063 1.6 45. Book value per share 53.1443 48.9317 46. Inventory turnover 4.8311 5.5912 17.56 47. Current ratio 1.2480 1.2788 1.86 48. Days sales in inventory 82.4307 76.5873 20.79 49. Debt ratio 89.78% 81.83% 59.3% 50. Acid test ratio 1.0179 1.0597 1.57 51. Profit margin 12.96% 16.76% 1.0% 52. Return on equity 22.83% 31.95% 3.64% 53. Receivables turnover .2855 .3353 5.89 54. Times interest earned 34.568 50.368 2.9 55. Cash flow to assets .1384 .1425 56. Return on assets .1023 .1306 57. Cash flow per share 17.0394 16.5892 58. Dividends per share 4.3037 3.8501 59. Price – earnings 13.646 12.3523 19.3 60. Dividends yield 21.325 20.290 2.2% 61. Price to free cash flow 2.03664 2.4422 30.2 62. Debt to equity 1.7986 2.0021 1.46 63. Dividend payout 35.51% 24.57% 42.1% 64. Basic earnings per share 11.9741 15.0667 2.66 1.6%