Universal Service

advertisement

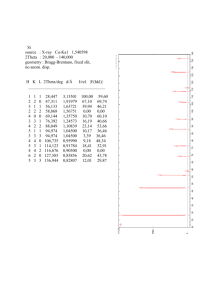

Introduction to Telecommunications Policy October 10, 1999 Aspen, Colorado Glenn H. Brown gbrown@mcleanbrown.com 1 Agenda 1.The Policy Makers 2.The Telecommunications Act of 1996 3.Regulatory Issues Facing Rural America 4.Keys to Effective Advocacy 2 The Policy Makers • In This Section We Will Examine: – The Major Telecom Regulatory Bodies • Federal Communications Commission (FCC) • State Regulatory Commissions • Federal/State Joint Boards – The Role of Other Governmental Bodies • United States Congress • Local and Municipal Government • The Courts – How/When to Get Involved 3 Federal Communications Commission • Established by the Communications Act of 1934 • Five Commissioners – – – – Appointed by the President and Confirmed by the Senate No More Than 3 From The Same Political Party Five Year Terms President Designates Chairman • Six Bureaus – Organized by Function – Handle Day-to-Day Responsibilities • Total Staff of 1755 (Per 1997 Annual Report) – Highly Qualified – Generally Lawyers, Accounts & Economists 4 5 COMMON CARRIER BUREAU • Accounting Policy Division – Oversees Universal Service Funding • Accounting Safeguards Division – Oversees Audits and Cost Accounting Rules • Network Services Division – Oversees Numbering, Network Reliability, TRS and Hearing Aid Compatibility • Enforcement Division – Handles Consumer Protection, Complaints and Merger/Acquisition • Industry Analysis Division – Collects and Distributes Data on the Telecom Industry • Competitive Pricing Division – Develops Pricing Policies for Interstate Services and Interconnection • Policy and Program Planning Division – Develops Rules and Regulatory Programs to Facilitate Competition 6 Levels of Entry at FCC • Commissioner Level – Commissioner – Legal Advisor • Bureau Level – Bureau Chief – Bureau Deputy Chief • Division – Division Chief/Deputy Chief – Working Staff 7 How the FCC Works • Telecom Rules in Code of Federal Regulations (CFR) Title 47 • FCC Processes to Make and/or Modify Rules – Notice of Inquiry (NOI) • FCC Considering Possible Action • Requests Input From Interested Parties • Written Comments, Reply Comments and Ex-Parte Presentations – Notice of Proposed Rulemaking (NPRM) • FCC Proposing Additions or Changes to Rules • Written Comments, Reply Comments and Ex-Parte Presentations – Requests for Public Comment • Requests Comment on Proposals and/or Papers Presented to Commission • FCC Processes to Enforce Rules 8 When/How to Work With the FCC • Before Visiting With Commissioners or Bureau Chief be Sure Issue is “On the Radar Screen” • Work With the Lower Level Staff First • Best Time to Present Views is Before Issue is Put Out For Comment – Opportunity to Shape the Notice – Ex-Parte Filings Not Required • File Complete and Informative Comments and Replies – Use Facts and Data • Make Ex-Parte Contacts to Reinforce Your Advocacy – Support Your Position – Address the Issues Presented by Other Parties – Form Coalitions When Possible • Contacts Prohibited During “Sunshine” Period 9 State Regulatory Commissions All 50 States and DC Have Commissions – From 3 to 7 Commissioners – Commissioner Selection • 39 States Appointed • 12 States Elected – Staff Size From 11 (RI) to 800 (CA) – Varied Responsibilities Including Telecom, Electricity, Gas, Water, Taxi Cabs, Insurance, etc. – Varied Rules and Procedures 10 State Commissions STATE NUMBER TYPE STAFF Alabama 3 Elected 140 Alaska 5 Appointed 42 Arizona 3 Elected 250 Arkansas 3 Appointed 101 California 5 Appointed 800 Colorado 3 Appointed 93 Connecticut 5 Appointed 156 Delaware 5 Appointed 26 District of Columbia 3 Appointed 57 Florida 5 Appointed 370 Georgia 5 Elected 148 Hawaii 3 Appointed 31 Idaho 3 Appointed 55 Illinois 5 Appointed 300 Indiana 5 Appointed 85 Iowa 3 Appointed 75 Kansas 3 Appointed 213 Kentucky 3 Appointed 121 Louisiana 5 Elected 85 Maine 3 Appointed 65 Maryland 5 Appointed 128 Massachusetts 5 Appointed 134 Michigan 3 Appointed 150 Minnesota 5 Appointed 43 Mississippi 3 Elected 145 STATE Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming NUMBER 5 5 3 3 3 5 5 7 3 5 3 3 5 3 7 3 3 3 3 3 3 3 3 3 3 TYPE STAFF Elected 43 Elected 42 Appointed 88 Appointed 78 Appointed 289 Appointed NA Appointed 700 Appointed 139 Elected 43 Appointed 370 Elected 460 Appointed 109 Appointed 538 Appointed 11 Elected 72 Elected 23 Elected 253 Appointed 245 Appointed 15 Appointed 23 Appointed 550 Appointed 156 Appointed 235 Appointed 180 Appointed 29 11 Major Differences FCC State PUCs Responsibilities Interstate Services Intrastate Services Operating Mode Paper Proceedings Live Hearings Staff Resources Significant Generally Less Local Service Rates Local Competition Universal Service Access Rates Local Competition Individual Parties Coalitions Major Issues Advocacy 12 The Joint Board Process • For Issues That Cross Jurisdictional Boundaries – Jurisdictional Separations – Universal Service • Makeup of Joint Board – Three Federal Commissioners – Four State Regulators – (Universal Service Joint Board Includes a Public Advocate) • Joint Board Recommends, FCC Decides • Mixed History 13 The Role of Congress • Congress Oversees the FCC and Approves Its Budget • Congress Passed The Telecommunications Act of 1996 – Directed the Introduction of Local Competition – Mandated Universal Service Protection – Called For Eventual Deregulation • Senators and Representatives are not Shy! – In 1998 Chairman Kennard Received Over 1800 Letters From Congress • Politics Often Gets Involved 14 Congressional Committees • United States Senate – Commerce, Science & Transportation Committee • John McCain (R - AZ), Chairman • Ernest F. Hollings (D - SC), Ranking Member – Communications Subcommittee • Conrad Burns (R - MT), Chairman • Ernest F. Hollings (D -SC), Ranking Member – The “Farm Team” • House of Representatives – Committee on Commerce • Tom Bliley (R - VA), Chairman • John D. Dingell (D - MI), Ranking Member – Subcommittee on Telecommunications • W. J. “Billy” Tauzin (R - LA), Chairman) • Edward J. Markey (D - MA), Ranking Member 15 The Role of Local Government • Traditionally Telecom Regulated at State and Federal Level • Industry is Changing and Converging – Digital revolution blurs boundaries between telecom, cable and Internet – Wireless services growing geometrically • Local Governments Becoming More Involved – Cable regulation has traditionally been local – Local zoning issues with tower siting – Sales tax issues with e-commerce • Will Federal Government Preempt? 16 The Role of the Courts • Fish ‘Gotta Swim, Birds ‘Gotta Fly and Lawyers ‘Gotta Sue • On Major Telecom Issues the Stakes are so High Than no Matter Who Wins The Other Guy Takes it to Court • If a Court Overturns the FCC on an Issue, it is Remanded Back to the FCC for Reconsideration 17 1996 Telecom Act Major Objectives • Open Local Telephone Markets To Competition • Incumbent Local Exchange Carriers (LECs) Must Open Their Networks To Competitors: – Interconnection – Wholesale Provisioning Of Services – Unbundled Network Elements • RBOCs May Enter Long Distance Markets Upon Meeting A 14-point “Checklist” • FCC Must Provide For The Provision Of Universal Service – Rural, Insular & High Cost Areas – Schools And Libraries – Rural Health Care 18 1996 Telecom Act Section 254(b) - Universal Service (1) Quality and Rates Quality services should be available at just, reasonable and affordable prices (2) Access to Advanced Services Access to advanced telecommunications and information services should be provided in all regions of the Nation (3) Access in Rural and High Cost Areas Consumers in all regions of the Nation should have access to services (including advanced services) at rates that are reasonably comparable to those in urban areas 19 1996 Telecom Act Section 254(b) - Universal Service (4) Equitable and Non-Discriminatory Contributions All telecommunications providers should contribute to the preservation and advancement of universal service (5) Specific and Predictable Support Mechanisms There should be specific, predictable and sufficient Federal and State mechanisms to preserve and advance universal service (6) Access to Advanced Services for Schools, Health Care and Libraries Elementary and secondary schools and classrooms, health care providers, and libraries should have access to advanced services. 20 1996 Telecom Act Other Major Provisions – Creates a Federal/State Joint Board to recommend universal service solutions to the FCC (254(a)) • Recommendation due November 8, 1996 • FCC to act on recommendations by May 8, 1997 – Defines “Eligible Telecommunications Carriers” (ETC) for receipt of universal service funds (214(e)) – Differentiates between “Rural” LECs and “Non-Rural” LECs • Based on size (I.e. < 100,000 lines) and area served (3(37)) • Different market opening requirements (251(f)) • NRLECS shall have multiple ETCs (214(e)(2)) – States that any Federal universal service support “should be explicit” (254(e)) 21 Major Regulatory Issues For Rural America • Universal Service • Access Reform/Rate Rebalancing • Local Competition • Broadband Development 22 UNIVERSAL SERVICE PROBLEM • Goal of Low Basic Service Prices • High Degree of Rate Averaging • Two Sources of Historical Universal Service Subsidy 1. Explicit About $1B 2. Implicit $5B - $19B Toll/Access Business Urban to to to Local Residence Rural • Telecom Act of 1996 Changed Everything 23 THE 1st FCC’s DECISION • Issued May 8, 1997 • Schools and Libraries – $2.25B Fund – Funding Based on State and Interstate Revenues – Sliding Scale of Discounts • Rural, Insular and High Cost Areas – Funding 75% States / 25% Federal – “Non-Rural” Telephone Companies • Support = Forward-Looking Cost - Benchmark • 14 Month Process to Select Proxy Cost Model – “Rural” Telephone Companies • Continue Present Mechanisms • Transition to Forward-Looking Mechanism Beginning in 2001 24 Major Problems • Many Rural States Can’t Afford to Pay 75% of HighCost Need – Key variable is the ratio of low-cost to high-cost customers • Proxy Models – Widely divergent positions – Accuracy of Model for small areas • Inherent Tensions Between the Players – High-cost states vs. low cost states – Local service providers vs. other telecom providers • Who Will Pay For Universal Service? How? 25 Non-Rural LECs "Common Inputs" (4.5B Fund) ST USF % 75/25 NATIONAL FUND % 25.00% 20.00% 15.00% 10.00% 5.00% 0.00% WY ID MT MS SD WV NE ND VT OK MO ME NM AL KS MN AR KY TX AZ LA WA IN NH Note: This chart assumes a fund size of $4.5B derived from using FCC “common inputs” in the BCPM3 model. 26 The actual fund size will be determined after completion of further proceedings to finalize model inputs. CO Non-Rural LECs FCC "Common Inputs ($4.5B Fund) ST USF % 75/25 NATIONAL FUND % 25.00% 20.00% 15.00% 10.00% 5.00% 0.00% VA WI TN NV IA NC OR SC GA UT MI IL OH DE PA HI CA FL MD NY CT RI MA PR AK Note: This chart assumes a fund size of $4.5B derived from using FCC “common inputs” in the BCPM3 model. The actual fund size will be determined after completion of further proceedings to finalize model inputs. NJ DC 27 Ratio of $100/mo+ Customers to Total State Total Lines Lines Over $100/mo SD 255,527 MT 311,085 ND 235,548 WY 221,982 NE 792,539 MS 1,185,210 ID 578,972 AR 848,296 MO 2,881,496 OK 1,585,379 NM 725,499 MN 2,352,496 KS 1,222,537 WV 776,326 IA 995,730 AZ 2,225,122 TX 10,449,569 AL 2,101,681 WA 3,044,486 LA 2,161,959 CO 2,270,706 OR 1,376,480 ME 651,597 WI 2,650,099 NV 937,114 KY 1,672,422 Source: BCPM3 with FCC Common Inputs 12,796 13,136 9,079 7,902 25,861 34,457 16,549 18,652 57,617 31,375 13,737 43,453 22,371 13,790 16,129 32,992 116,281 22,103 29,465 17,123 17,160 8,962 4,094 16,074 5,458 9,235 Ratio 20 24 26 28 31 34 35 45 50 51 53 54 55 56 62 67 90 95 103 126 132 154 159 165 172 181 State IL UT VT GA SC NH MI IN VA TN CA NC AK FL OH PA HI NY MD DE MA RI NJ CT DC TOTAL Total Lines 7,378,715 935,397 331,470 3,881,849 1,502,650 724,804 5,755,154 3,168,932 4,029,810 2,713,895 20,521,641 3,950,135 149,078 9,479,041 6,267,407 7,258,883 704,179 11,702,236 3,367,642 509,854 4,272,096 643,137 5,887,531 1,991,162 520,361 152,156,917 Lines Over $100/mo 39,768 4,311 1,501 14,888 5,374 2,320 17,117 8,366 9,352 6,215 45,775 6,827 224 12,555 7,952 7,755 540 7,205 910 95 591 77 191 64 815,824 Ratio 186 217 221 261 280 312 336 379 431 437 448 579 666 755 788 936 1,304 1,624 3,701 5,367 7,229 8,352 30,825 31,112 187 28 Proxy Cost Models • The Original Contenders – BCPM – HAI – HCPM BellSouth, Sprint, U S WEST ($4.5B - $9B NRLEC) AT&T, MCI ($3B - $4.5B NRLEC) FCC Staff • Major Model Issues – – – – – Network Design - “Engineer-in-a-Box” Customer Location Input Values Accuracy for Small Geographic Areas Who Needs Reality? • Current Status – FCC finalizing “synthesis model” and inputs for non-rural LECs – Rural Task Force to address model issues for rural LECs 29 Reconsideration of 1st Decision • April, 1998 - FCC Reports to Congress – Will reconsider 75/25 funding • July, 1998 - FCC Refers Issues to Joint Board – Alternatives to 75/25 funding – Report due 11/23/98 – Delays “non-rural” LEC funding to 7/1/99 • October 30, 1998 - Joint Board 2nd Recommendation – Some states will require additional federal support – Two-pronged test for support 1. Forward-looking costs >> national average 2. Inability to cover high-cost problem internally – Fund not “significantly larger” than present (ie. $125M for NRLECs) – Uses statewide averages of cost • Continues urban-to-rural implicit subsidies • Joint board may revisit if “competition threatens affordability” 30 The 2nd FCC Decision • • • • Issued May 28, 1999 Delays “Non-Rural” Explicit Fund Until 1/1/00 75/25 Funding Plan is Rejected Fund Covers State-Wide Average Costs over “Benchmark” – Uses “Synthesis Model” – Asks for input on what the benchmark should be • State Must Provide $X/Line of the Support – Provides more funding to needy states – Asks for input on what the per-line amount should be • Fund “Not Significantly Larger” Than Present ($125M) • Recipients “Held Harmless” for Current Level of Support 31 Problems With 2nd FCC Decision • Political Tensions Within the System – Low-cost states vs. high-cost states – Local service providers vs. other telecom providers • Averaging Perpetuates Implicit Support – High margin urban customers vulnerable to competition – System will be slow to react in crisis • Creates “Two-Tier” System for Rural Consumers – “Rural” Companies • Support at 115% of embedded cost – “Non-Rural” Companies • Support no larger than present • Must rely on implicit subsidies • Perpetuates the Status Quo – No more support than present ($125M) – No one gets less than present 32 Additional Problems • Funding and the Models – $125M falls far short of requirements • HAI w/Defaults • BCPM w/Defaults • Either w/FCC “Common” $3 Billion $9 Billion $4.5 Billion – Output very sensitive to inputs and platform (see above) – FCC’s “Synthesis” model still not finalized – If model is delayed, so is funding • “Non-Rural” vs. “Rural” Issues – “Non-rural” must be funded at least 115% – Forward-looking vs. Embedded • Averaging is Fundamentally Incompatible With Competition – False entry signals in over-priced areas – False protection for high-cost rural customers 33 Additional Problems (Continued) • A Fund That is Too Small Will Harm Rural America – Increased reliance on vulnerable access charges – Investment and advanced services drawn to urban areas – Rural consumers become “have-nots” • Advanced Services Will Come Fastest by Letting Markets Work – Provide sufficient funding to rural areas – Relax rules that prevent incumbents from delivering services • Inter-LATA restrictions • Unnecessary unbundling and separate subsidiary rules • Universal Service Fills the Gaps – Fully competitive market delivers advanced services to most – Universal service fund fills the gaps – The greater the role of markets, the smaller the fund 34 Schools, Libraries & Rural Health Care • Initial FCC Decision Set Funding Targets – Schools & Libraries $2.25B – Rural Health Care $0.40B • Sliding Scale For S&L Discounts – Rural vs. Non-Rural – Relative Poverty Levels • Funding Phased In Over Time 35 Access Reform/Rate Rebalancing • The “Flip-Side” of Universal Service • As Explicit Support is Increased Rates are Reduced to Remove Implicit Support • If Sufficient Explicit Support is not Provided: – Implicit support remains in rates – Competition erodes implicit support – Pressure for rural rate increases • Implicit Support Distorts Competitive Markets – False entry signals in low-cost markets – No incentives for competition in rural markets 36 Broadband Development • Exciting Technology Developments for Delivery – – – – DSL Cable Modems Wireless? Other? • What Role Should Universal Service Funding Play? • Should Narrowband Regulatory Model be Applied? • Should Competitive Markets be Allowed to Work? 37 What Can Concerned Citizens Do? • Get Informed and Get Involved • Contact The Following: – – – – Your State Public Service Commission The Federal Communications Commission (FCC) The Federal/State Joint Board Your Congressional Delegation • Major Message Points: – Universal service is a national priority – A sufficient federal fund must be established for high-cost areas – Advanced services will come to rural America through a combination of targeted supports and free market incentives – Markets must be allowed to function! 38 Keys to Effective Advocacy 1. Regulators Are People Too 2. Work The Staff First 3. Use Your Time Wisely 4. Listen As Much As You Talk 39 Keys to Effective Advocacy 5. It’s The Public Interest, Stupid 6. Know Who Supports You – Who Opposes You 7. Acknowledge Other Points Of View 8. Address Holes In Your Argument 40 Keys to Effective Advocacy 9. No Surprises – No Threats 10. Use Facts and Data 11. Keep Your Commitments 12. It Ain’t Over ‘Til Its Over 41