Case Studies

Case Study-1

Make versus Buy, Activity-Based Costing, Opportunity Costs.

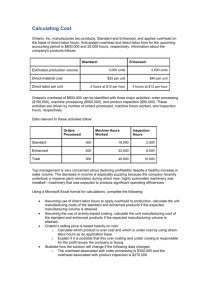

Afghan Ltd produces bicycles. This year’s expected production is 10000 units. Currently, Afghan Ltd makes the chains for its bicycles. Afghan Ltd’s management accountant reports the following costs for making the

10000 bicycles chains:

Cost per unit: Costs for 10000 units

Direct Materials:

Direct Manufacturing labour:

Variable mfg. Overhead (Power and utilities):

4.000

2.00

1.50

40000

20000

15000

Inspection, set-up, materials handling:

Machine rent:

Allocated fixed costs of plant administration, taxes and insurance:

Total costs:

2000

3000

30000

110000

Afghan Ltd has received an offer from an outside vendor to supply any number of chains Afghan Ltd requires at 8.20 per chain. The following additional information is available: a. Inspection, set-up and materials-handling costs vary with the number of batches in which the chains are produced. Afghan Ltd produces chains in batch sized of 1000 units. Afghan Ltd will produce the 10000 units in 10 batches. b. Afghan Ltd rents the machine used to make the chains. If Afghan Ltd buys all of its chains from the outside vendor, it does not need to pay rent on this machine.

Required

1. Assume that if Afghan Ltd purchases the chains from the outside vendor the facility where the chains are currently made will remain idle,. On the basis of financial considerations alone, should Afghan Ltd accept the outside vendor’s offer tat the anticipated production (and sales) volume of 10000 units? Show your calculations.

2. For this question, assume that if the chains are purchase outside, the facilities where the chains are currently made will b e used to upgrade the bicycles by adding mud flaps and reflectors. As a consequence, the selling price of bicycles will be raised by 20. The variable cost per unit of the upgrade would be 18, and additional

tooling cost of 16000 would be incurred. On the basis of financial consideration, alone, should Afghan Ltd make or buy the chains, assuming that 10000 units are produced (and sold)? Show your calculations.

3. The sales manager at Afghan Ltd is concerned that the estimate of 10000 units may be high and believes that only 6200 units will be sold. Production will be cut back, freeing up work space. This space can be used to add the mud flaps and reflectors whether Afghan Ltd buys the chains or makes them in-house. At this lower output; Afghan Ltd will produce the chains in 8 batches of 775 units each. On the basis of financial considerations alone, should Afghan td purchase the chains form the outside vendor? Show your calculations.

Caselet-1

The controller of Best Corporation has predicted the following costs at various levels of Juice output.

Juice Output (0.75-Liter Bottles)

10000 Bottles 15000 Bottles 20000 Bottles

Variable production costs…………………………...$ 35000

Fixed production costs…………………………………..100000

Variable selling and administrative costs……..……2000

Fixed selling and administrative costs………….….40000

$ 52500 $ 70000

100000 100000

3000

40000

195500

4000

40000

214000 Total……………………………………………………………..177000

The company’s marketing manager has predicted the following prices for the firm’s fine juices at various levels of sales.

Juice sales

10000 Bottles 15000 Bottles 20000 Bottles

Sales price per 0.75-liter bottle…………………..$ 18 $ 15 $12

Required:

1.

Calculate the unit costs of juice production and sales at each level of output. At what level of output is the unit cost minimized?

2.

Calculate the company’s profit at each level of production. Assume that the company will sell all of its output. At what production level is profit maximized?

3.

Which of the three output levels is best for the company?

4.

Why does the unit cost of juice decrease as the output level increases? Why might sales price per bottle decline as sales volume increases?

Caselet-2

CompTech Inc. manufactures printers for use with home computing systems. The firm currently manufactures both the electronic components for its printers and the plastic cases in which the devices are enclosed. Mr. Ahmad, the production manager, recently received a proposal from Universal Plastics

Corporation to manufacture the cases for CompTech’s printers. If the cases are purchased outside,

CompTech will be able to close down its Printer Case Department. To help decide whether to accept the bid from Universal Plastics Corporation, Ahmad asked CompTech’s controller to prepare an analysis of the costs that would be saved if the Printer Case Department were closed. Included in the controller’s list of annual cost savings were the following items:

Building rental (The Printer Case Department occupies one-sixth of the factory building, which CompTech rents for $ 177000 per year)………………………………………………………………………… $29500

Salary of the Printer Case Department supervisor...................................................................……$50000

In a lunchtime conversation with the controller, Ahmad learned that CompTech was currently renting space in a warehouse for $ 39000. The space is used to store completed printers. If the Printer Case Department were discontinued, the entire storage operation could be moved into the factory building and occupy the space vacated by the closed department. Ahmad also learned that the supervisor would be assigned the job of managing the assembly department, whose supervisor recently gave notice of his retirement. All of

CompTech’s department supervisors earn the same salary.

Required:

1.

You have been hired as a consultant by Ahmad to advise him in his decision. Write a memo to Ahmad commenting on the costs of space and supervisory salaries included I the controller’s cost analysis.

Explain in your memo about the ‘real’ costs of the space occupied by the Printer Case Department and the supervisor’s salary. What types of costs are these?

2.

Independent of your response to requirement (1), suppose that CompTech’s controller had been approached by his friend Mr. Wasim, the assistant supervisor of the Printer Case Department. Wasim is worried that he will be laid off if the Printer Case Department is closed down.

Wasim has asked his friend to understate the cost savings from closing the department, in order to slant the production manger’s decision toward keeping the department in operation. Comment on the

Controller’s ethical responsibilities.

Memorandum

Date: Today

To: Mr. Ahmad

From: M. A. Student

Subject: Costs related to Printer Case Department

The $ 29500 building rental cost allocated to the Printer Case Department is part of rental costs for the entire building. Even if the PCD is closed down, CompTech still will occupy the entire building. Therefore, the entire rental cost, including the 29500 portion allocated to the PCD will be incurred whether or not the department closes.

The real cost of the pace occupied by the PDC is the 39000 the company is paying of rent warehouse space.

This cost would be avoided if the PCD were closed, since the storage operation could b moved into the company’s main building. The 39000 rental cost is the opportunity cost of using space in the main building for.

The supervisor of the PCD will be retained by the company regardless of the decision about the PCD .

However, if the PCD is kept in operation the company will have to hire a new supervisor of the Assembly

Department. The salary of that new supervisor is a relevant cost of continuing to operate the PCD.

Another way of looking at the situation is to realize that with PCD is operation, the company will need two supervisor; the current PCD supervisor and a new supervisor the Assembly Department. Alternatively, the

PCD is closed, only the current PCD supervisor will be needed. He or she will move to the Assembly

Department. The difference, then, between the two alternatives is the cost of compensation the new

Assembly Department supervisor if the PCD is not closed.

2.

The Controller has an ethical obligation to state accurately the projected cost savings form closing the PCD.

The production manager and other decision makers have a right to know the financial implication of f closing the department. Several of the ethical standards for management accountant apply, including the following:

Competence:

Maintain an appropriate level of professional expertise by continually dev eloping knowledge and sills.

Perform professional duties in according ace with relevant laws, regulations and technical standards.

Provide decision support information and recommendations that are accurate, clear, concise and timely.

Recognize and communicate professional limitations or other constraints that would preclude responsible judgment or successful performance of an activity

Credibility

Communicate information fairly and objectively.

Disclose all relevant information that could reasonably be expected to influence an intended user’ understanding of the reports, analysis or recommendations.

Disclose delays or deficiencies in information, timeliness, processing or internal controls in conformance with organization policy and or applicable law.

Caselet-3

Mr. Rahman is a successful Afghanistan’s orchard man who has formed his own company to produce and package applesauce. Apples can be stored for several months in cold storage, so applesauce production is relatively uniform throughout the year. The recently hired controller for the firm is about to apply the high-low method in estimating the company’s energy cost behaviour. The following costs were incurred during the past 12 moths:

Month

January

Pints of Applesauce Produced

35000

Energy Cost ($)

23400

February

March

April

May

June

July

21000

22000

24000

30000

32000

40000

22100

22000

22450

22900

23350

28000

August

September

October

November

30000

30000

28000

41000

39000

22800

23000

22700

24100

24950 December

Required:

1.

Use the high-low method to estimate the company’s energy cost behavior and express it in equation form.

2.

Predict the energy cost for a month in which 26000 pints of applesauce are produced.

Caselet-4

Maiwand Travels & Tours has incurred the following bus maintenance costs during the recent tourist season.

Month Miles Travelled

By Tour Buses

Cost

November

December

8500

10600

11400 Afs.

11600

January

February

March

April

12700

15000

20000

8000

11700

12000

12500

11000

Required:

1.

Use the high-low method to estimate the variable cost per tour mile travelled and the fixed cost per month.

2.

Develop a formula to express the cost behavior exhibited by the company’s maintenance cost.

3.

Predict the level of maintenance cost that would be incurred during a month when 22000 tour miles and driven.

4.

Build a spreadsheet: Construct an Excel spreadsheet to solve all the preceding requirements.

Show how the solution will change if the following information changes: in March there were

21000 miles travelled and the cost was 12430 Afs.

Caselet-5

The following selected data were taken from the accounting records of Afghan Manufacturing. The company uses direct-labor hours as its cost driver for overhead costs.

Month

January

February

March

April

Direct-Labor Hours

23000

30000

34000

26000

Manufacturing Overhead

454000

517000

586000

499500

June 28000 515000

March’s costs consisted of machine supplies (102000), depreciation (15000), and plant maintenance

(469000). These costs exhibit the following respective behaviour: variable, fixed and semi-variable.

The manufacturing overhead figures presented in the preceding table do not include the Company’s supervisory labor amounts to 45000. The cost of 90000 from 15000-29999 hours and 135000 when activity reaches 30000 hours or more.

Required:

1.

Determine the machine supplies cost and depreciation for January.

2.

Using the high-low method, analyze the Company’s plant maintenance cost and calculate the monthly fixed portion and the variable cost per direct labor hour.

3.

Assume that present cost behaviour patterns continue into the latter half of the year. Estimate the total amount of manufacturing overhead the company can expect in November if 29500 direct labor hours are worked.

4.

Briefly explain the difference between a fixed cost and a step fixed cost.

5.

Assume that a company has a step fixed cost. Generally speaking, where on a step should the firm attempt to operate if it desires to achieve a maximum return on its investment?

Caselet-6

Disk City, Inc. is a retailer for digital video disks. The projected net income for the current year is

200000 based on a sales volume of 200000 video disks. Disk City has been selling the disks for 16 each. The variable costs consist of the 10 unit purchase price of the disks and a handling cost of 2 per disk. Disk City’s annual fixed costs are 600000.

Management is planning for the coming year, when it expects that the unit purchase price of the video disks will increase 30 percent.

Required:

1.

Calculate Disk city’s break-even point for the current year in number of video disks.

2.

What will be the company’s net income for the current year if there is a 10 percent increase in projected unit sales volume?

3.

What volume of sales must Disk City achieve in the coming year to maintain the same net income as projected for the current year if the unit selling price remains at 16?

4.

In order to cover a 30 percent increase in the disk’s purchase price for the coming year and still maintain the current contribution margin ratio, what selling price per disk must Disk City establish for the coming year?

5.

Build a spreadsheet: Construct an Excel spreadsheet to solve requirements 1, 2, 3, above. Show how the solution will change if the following information changes: the selling price is 17 and the annual fixed costs are 640000?

Caselet-7

CPC Company produced and sold 60000 backpacks ruing the year just ended at an average price of 20 per unit. Variable manufacturing costs were 8 per unit and variable marketing cost were 4 per unit sold. Fixed costs amounted to 180000 for manufacturing and 72000 for marketing. There was no year end work in process inventory.

Required:

1.

Compute the CPC Company’s break even point in sales dollars for the year.

2.

Compute the number of sales units required to earn a net income of 180000 during the year.

3.

The Company’s variable manufacturing costs are expected to increase by 10 percent in the coming year. Compute the firm’s break even point in sales dollars for the coming year.

4.

If the company’s variable manufacturing cost do increase by 10 percent, compute the selling price that would yield the same contribution margin ratio in the coming year.

Caselet-8

Silver Screen, Inc. owns and operates a nationwide chain of movie theatres. The 500 properties in the company vary from low-volume, small-town, single-screen theatres to high-volume, urban multiscreen theatres. The firm’s management is considering installing popcorn machines, which would allow the theatres to sell freshly popped corn rather than pre-popped corn. This new feature would be advertised to increase patronage at the company’s theatres. The fresh popcorn will be sold for

1.75 per tub. The annual rental costs and the operating costs vary with the size of the popcorn machines. The machine capacities and costs are shown below:

Annual capacity…. tubs

Economy

45000 tubs

Popper Model

Regular

90000 tubs

Super

140000

Costs:

Annual machine rental

Popcorn cost per tub

Other cost per tub

Cost of each tub

Required:

8000

.13

1.22

.08

11000

.13

1.14

.08

20000

.13

1.05

.08

1.

Calculate each theatre’s break even sales volume (measured in tubs of popcorn) for each model of popcorn popper.

2.

Prepare a profit-volume graph for one theatre, assuming that the Super Popper is purchased.

3.

Calculate the volume at which he Economy Popper and the Regular Popper earn the same profit or loss in each movie theatre.

Caselet-9

Condensed monthly income data for Watan Book Store are presented in the following table for May-

2014.

Mall Store Downtown Store Total

Sales 80000 120000 200000

Less: Variable expenses

Contribution Margin

Less: Fixed Costs

Operating income

32000

48000

20000

28000

84000

36000

4000

(4000)

116000

84000

60000

24000

Additional Information:

Management estimates that closing the downtown store would result in a 10 percent decrease in mall store sales, while closing the mall store would not affect downtowns store sales.

One-fourth of each store’s fixed expenses would continue through June 30, 2014, if either store were closed.

The operating results for May 2014 are representative of all months.

Required:

1.

Calculate the increase or decrease in the company’s monthly operating income during 2014 if the downtown store is closed.

2.

The management of the company is considering a promotional campaign at the downtown store that would not affect the mall store. Annual promotional expenses at the downtown store would be increased by 60000 in order to increase downtown store sales by 10 percent. What would be the effect of this promotional campaign on the company’s monthly operating income during

2014?

3.

One-half of the downtown store’s dollar sales are from items sold at their variable cost to attract customers to the store. The management is considering the deletion of these items, a move that would reduce the downtown store’s direct fixed expenses by 15 percent and result in the loss of

20 percent of the remaining downtown stores’ sales volume. This change would not affect the mall store. What would be the effect on Watan’s monthly operating income if the items sold at their variable cost are eliminated?

4.

Construct an excel spreadsheet to solve all of the preceding requirements. Show how the solution will change if the following information changes: the downtown store‘s sales amounted to 126000 and its variable expenses were 86000.

Caselet-10

Empire Chemical Company produces three products using three different continuous processes. The products are Alpha, Beta and Delta. Projected sales in gallons for the three products for the year 2013 &

2014 are as follows:

Alpha

Beta

2013

60000

40000

2014

65000

35000

Delta 25000 30000

Inventories are planned for each product so that the projected finished goods inventory at the beginning of each year is equal to 8 percent of that year’s projected sales.

Because of the continuous nature of Empire’s processes, work in process inventory for each of the products remains constant throughout the year.

The raw material requirements of the three products are shown in the following chart.

Raw Material

A

B

Units pounds pounds

Unit Price

8.00

6.00

Alpha Beta Delta

0.2 0.4 -

0.4 - 0.5

C gallons 5.00 1.0 0.7 0.5

D gallons 10.00 - 0.3 0.5

Raw material inventories are planned so that each raw material’s projected inventory at the beginning of a year is equal to 10 percent of the previous year’s usage of that raw material.

The conversion requirements in hours per gallon for the three products are Alpha: 0.07 hour,

Beta 0.10 hour and Delta 0.16 hour. The conversion cost of 20$ per hour is considered 100 percent variable.

Required:

1.

Determine Empire Chemical Company’s production budget (in gallons) for the three products for 2013.

2.

Determine the conversion cost budget for 2013.

3.

Assuming the 2012 usage of Raw Material ‘C’ is 100000 gallons; determine the company’s raw material purchases budget (in dollars) for C in 2013.

Caselet-11

Vista Electronics manufactures two different types of coils used in electric motors. In the spring of current year, Ahmad Tamim, the controller, compiled the following data.

Sales forecast for 2014 (all units to be shipped in 2014):

Products

Light coil

Units

60000

Price

65

95 Heavy coil

Raw material prices and inventory levels:

40000

Expected Inventories Desired Inventories Anticipated

Raw Material

Sheet metal

Copper wire

Platforms

January, 1 2014 December 31, 2014 Purchase price

32000 lb. 36000 lb. 8

29000 lb.

6000 units

Use of raw material:

32000 lb.

7000 units

Amount Used Per Unit

5

3

Raw Material

Sheet metal

Copper wire

Platforms

Direct-labor requirements and rates:

Product

Light coil

Light Coil

4 lb.

2 lb

-

Hours per Unit

2

Heavy Coil

5 lb

3 lb.

1 unit

Heavy coil

Finished-goods inventories (in units):

3

Rate per Hour

15

20

Product

Light coil

Heavy coil

Expected

January 1, 2014

20000

8000

Desired

December 31, 2014

25000

9000

Manufacturing overheads:

Overhead Cost Item Activity-Based Budget Rate

Purchasing and material handling………………………0.25 per pound of sheet metal and copper wire purchased

Depreciation, utilities and inspection…………………4.00 per coil produced (either type)

Shipping……………………………………………………………1.00 per coil shipped (either type)

General manufacturing overhead……………………..3.00 per direct labor hour

Required: Prepare the following budgets for 2014.

1.

Sales budget (in dollars).

2.

Production budget (in units).

3.

Raw-material purchases budget (in quantities).

4.

Raw-material purchases budget (in dollars).

5.

Direct-labor budget (in dollars).

6.

Manufacturing-overhead budget (in dollars).

Caselet-12

New Jersey Valve Company manufactured 7800 units during January of a control valve used by milk processors in its Camden plant. Records indicated the following:

Direct labor…………………………………………………………………………………………....40100 hr. at 14.60 per hr.

Direct material purchased………………………………………………………..…………….…25000 lb. at 2.60 per lb.

Direct material used………………………………………………………………………………………………………23100 lb.

The control valve has the following standard prime cost:

Direct material………………………………………………………………………………..3 lb at 2.50 per lb………….7.50

Direct labor……………………………………………………………………………………..5 hr. at 15.00 per hr…….75.00

Standard prime cost per unit………………………………………………………………………………………………..82.50

Required:

1.

Prepare a schedule of standard production costs for January, based on actual productions of 7800 units.

2.

For the moth of January, compute the following variances, indicating whether each is favourable or unfavourable. a.

Direct-material price variance b.

Direct-material quantity variance.

c.

Direct-labor rate variance. d.

Direct-labor efficiency variance.

Caselet-13

Maiwand Company produces paper for photocopiers. The company has developed standard overhead rates based on a monthly capacity of 180000 direct labor hours as follows:

Standard cost per unit (one box of paper)…………………………………………………..……$ 6

Variable overhead (2 hours @ $ 3 per hour)…………………………………………………...$ 10

Total………………………………………………………………………………………………………………….16

During April, 90000 units were scheduled for production: however, only 80000 units were actually produced. The following data relate to April.

1.

Actual direct labor cost incurred was $ 1567500 for 165000 actual hours of work.

2.

Actual overhead incurred totalled $ 1371500 of which $ 511500 was variable and $ 860000 was fixed.

Required:

Prepare two exhibits to show the following variances. State whether each variance is favourable or unfavourable, where applicable.

1.

Variable overhead spending variance.

2.

Variable overhead efficiency variance.

3.

Fixed overhead budget variance.

4.

Fixed overhead volume variance.

Caselet-14

Following are eight sets of partial factory overhead data, with favourable variances shown in parentheses:

Actual

Factory

Overhead

Applied

Factory

Overhead

Budget

Allow.(Based on

Capacity Utilized)

Spending

Variance

IDLE

Capacity

Variance i. ii. iii. iv.

$30000

?

24000

?

$29000

15000

24000

?

$32000

?

?

18000

$?

1000

(6000)

1000

$?

7000

?

2000

v. vi. vii.

Required:

18000

27000

16000

20000

?

16000

?

?

?

3000

(6000)

-0-

Compute the missing figures.

Caselet-15

On December 31 st , the work in process account of Zaryab Corporation showed:

?

(2000)

?

Work in Process

Materials 25300 Finished Goods 49700

Direct Labor 21150

FOH 16670

Materials charged to work still in process amounted to $ 6540. Factory overhead is a fixed percentage of direct labor cost.

Compute the individual amounts of factory overhead and direct labor charged to work still n process. (Round off all amounts to four decimal places).