Cost-Volume-Profit Analysis

advertisement

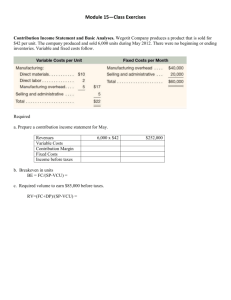

6 Cost Volume Profit Analysis Chapter 6 INTRODUCTION The Profit Function Breakeven Analysis Differential Cost Analysis Slide 1 6 The Profit Equation Operating Profit = Total Revenue – Total Costs Operating profit equals total revenue less total costs. Slide 2 6 The Profit Equation Operating Profit Slide 3 = = Total Revenue – Total Costs TR – TC 6 The Profit Equation Total = Revenue TR Slide 4 = Average Selling Units of × Price Per Unit Output P × X 6 Slide 5 The Profit Equation Total Costs = TC = Variable Costs Units of Fixed × + Per Unit Output Costs (V × X) + F 6 Slide 6 The Profit Equation Now, we’ll expand our original equation for profits! = (P × X) - [(V × X) + F] 6 Slide 7 The Profit Equation Now, we’ll expand our original equation for profits! = (P × X) - [(V × X) + F] = (P – V)X – F 6 Example Here is the information from the Hap Bikes: Total Sales (500 bikes) $ 250,000 Less: variable expenses 150,000 Contribution margin $ 100,000 Less: fixed expenses 80,000 Net income $ 20,000 Slide 8 Per Unit $ 500 300 $ 200 Percent 100% 60% 40% 6 Example Slide 9 = (P – V)X – F 6 Finding Target Volumes The formula to find a volume expressed in units for a target profit is . . . Target Volume (units) Fixed costs + Target profit = Contribution margin per unit How many bikes must Hap sell to earn an annual profit of $100,000? Slide 10 6 Finding Target Volumes Target Volume (units) Slide 11 Fixed costs + Target profit = Contribution margin per unit 6 Proof If Hap sells 900 bikes, its operating profit would be . . . Slide 12 = (P – V)X – F 6 Finding the Break-Even Point The Break-Even Point is the volume level where profits equal zero. To find the break-even point in units, we use the target volume in units equation and set the profit to zero. To find the break-even point in sales dollars, we use the target volume in sales dollars equation and set the profit to zero. Slide 13 6 Break-Even in Units Let’s use the Hap Bikes information again. Total Sales (500 bikes) $ 250,000 Less: variable expenses 150,000 Contribution margin $ 100,000 Less: fixed expenses 80,000 Net income $ 20,000 Per Unit $ 500 300 $ 200 Percent 100% 60% 40% Contribution margin ratio Slide 14 6 Break-Even in Units Break-Even = Volume (units) Slide 15 Fixed costs + Target profit Contribution margin per unit 6 Break-Even in Sales Dollars Break-Even = Volume (sales $) = Slide 16 Fixed costs + Target profit Contribution margin ratio $80,000 + $0 .40 6 Target Volume in Sales Dollars We can calculate the target volume in sales dollars using the contribution margin ratio. Contribution margin per unit Sales price per unit Slide 17 6 Target Volume in Sales Dollars The equation for finding the target volume in sales dollars is . . . Target Volume = (sales $) Slide 18 Fixed costs + Target profit Contribution margin ratio 6 Graphic Presentation Consider the following information for Hap Bikes: Income 300 units Sales $ 150,000 Less: variable expenses 90,000 Contribution margin $ 60,000 Less: fixed expenses 80,000 Net income (loss) $ (20,000) Slide 19 Income 400 units $ 200,000 120,000 $ 80,000 80,000 $ - Income 500 units $ 250,000 150,000 $ 100,000 80,000 $ 20,000 6 Graphic Presentation 450,000 400,000 350,000 300,000 250,000 200,000 150,000 100,000 50,000 - Slide 20 100 200 300 400 500 600 Volume per period (X) 700 800 6 Graphic Presentation 450,000 400,000 350,000 300,000 250,000 200,000 Break-even point 150,000 100,000 50,000 Slide 21 100 200 300 400 500 600 Volume per period (X) 700 800 Using CVP to Analyze Different Cost Structures 6 Cost structure - The proportion of fixed and variable to total costs of an organization. Operating leverage - The extent to which an organization’s costs structure is made up of fixed costs. Let’s look at an example of different costs structures for different companies. Slide 22 6 Using CVP to Analyze Different Cost Structures High Variable Company % (50,000 units) Sales $ 500,000 100% Variable costs 400,000 80% Contribution margin 100,000 20% Fixed costs 40,000 8% Operating profit $ 60,000 12% Break-even units Contribution margin per unit $ Slide 23 Hi Fixed Company % (50,000 units) $ 500,000 100% 100,000 20% 400,000 80% 340,000 68% $ 60,000 12% 20,000 2.00 42,500 $ 8.00 6 Using CVP to Analyze Different Cost Structures High Variable Company % (50,000 units) Sales $ 500,000 100% Variable costs 400,000 80% Contribution margin 100,000 20% Fixed costs 40,000 8% Operating profit $ 60,000 12% Break-even units Contribution margin per unit $ Hi Fixed Company % (50,000 units) $ 500,000 100% 100,000 20% 400,000 80% 340,000 68% $ 60,000 12% 20,000 2.00 42,500 $ 8.00 Let’s see what happens when both companies experience a 10% increase in sales. Slide 24 6 Using CVP to Analyze Different Cost Structures High Variable Company % (55,000 units) Sales $ 550,000 100% Variable costs 440,000 80% Contribution margin 110,000 20% Fixed costs 40,000 7% Operating profit $ 70,000 13% Break-even units Contribution margin per unit $ Slide 25 Hi Fixed Company % (55,000 units) $ 550,000 100% 110,000 20% 440,000 80% 340,000 62% $ 100,000 18% 20,000 2.00 42,500 $ 8.00 6 Margin of Safety Excess of projected (or actual) sales over the break-even volume. The amount by which sales can fall before the company is in the loss area of the break-even graph. Sales Break-even – volume sales volume Slide 26 = Margin of Safety 6 Margin of Safety Hap is currently selling 500 bikes, and we calculated the break-even to be 400 units ($80,000 fixed costs ÷ $200 contribution margin). Slide 27