Word Format - Summary of 504 Jobs Act Debt Refinance Provisions

advertisement

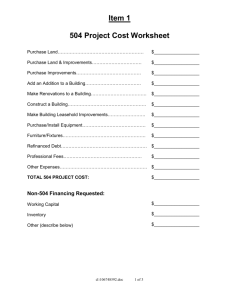

The small business concern (SBC or Borrower) must have a mortgage coming due for renewal on or before December 31, 2012. SBA plans to expand availability beyond this constraint, but it will remain subject, initially to balloon notes and the creation of a substantial cash flow benefit to the SBC. At this writing the cash out provision of the program is not yet available. Loans being refinanced must have been current for the past year with no payment being deferred or past due for more than 30 days. A transcript must be provided. If the loan is “own lender debt” a full transcript history of the loan must be provided to evaluate risk. Third Party Lender (TPL) must certify that they have no knowledge of a default or the likelihood of a loss or information related thereto. 504 loan proceeds are to be used to refinance the qualified debt with no money going to expansion or purchases. 85% of the refinance must have been for originally eligible purposes and must be documented to the satisfaction of SLPC. TPL and Borrower must certify eligibility of use of proceeds and all of the proceeds of the original loan must have been used for the benefit of the small business concern. Funding for the Refinancing Project must come from three (3) sources: o Third Party Lender - not less than 50% o SBA 504 Loan - not more than 40% o Borrower - not less than 10% o PLEASE SEE ATTACHED EXAMPLE Debt must have been incurred not less than two (2) years prior to the date the application is received by SBA. Small business concern must have been in business for two (2) years prior to the submission of the application. The Third Party loan and the 504 loan combined may not be more than 90% of the fair market value of the fixed assets securing the combined loans, which may not in any event, exceed the outstanding principal balance of the debt being refinanced. If the amount of the refinance is not sufficient to repay the entire outstanding debt, the CDC must disclose how the balance of the debt will be handled, as noted below. The lender of the qualified debt to be refinanced may: o forgive all or part of the deficiency (which may have tax consequences for the Borrower) o accept payment from the Borrower for all or part of the deficiency, o accept a new Note for the balance which will be subordinate to the liens of the TPL and CDC/SBA. Such notes will contain at least a three-year stand-by requirement o PLEASE SEE ATTACHED EXAMPLE In addition to a cash contribution, the Borrower’s 10% contribution may be satisfied by its equity in the eligible fixed asset (The 504 Project) serving as collateral for the Refinancing Project or by the equity in any other fixed assets that are acceptable to SBA as collateral. An independent appraisal of the fair market value of the project assets and any additional assets offered as additional collateral must be provided and must be dated within six months of the application. Appraiser requirements are those reflected in SOP 50 10 5(c). We are guessing that the appraisal(s) will have to be submitted to SBA with the application. Additional collateral pledges may have preexisting liens to the TPL and CDC/SBA. Debt may be refinanced even if it does not meet the job creation or other economic development objectives. However, then the 504 loan size may not exceed the product obtained by multiplying the number of full-time equivalent employees (40 hour work week) of the Borrower by $65M. (Note “504 loan size” is believed to refer to the debenture, not the entire project.). No refinancing of loans with an existing federal guaranty. (e.g. a 7(a) loan or USDA loan). No refinancing of a loan which is already part of an existing 504 project. No refinancing of debt from an Associate of the TPL/CDC, SBIC or a NMVCC. No refinancing of debt where a creditor is in a position to sustain a loss, as determined by SLPC. No loans may be processed under delegated authority. “Own Lender” debt refinanced into a TPL may not be included in securitization for SBA guaranteed loan pools. All loans must be funded by the sale of the debenture within six (6) months of approval. Delinquencies between approval and funding must be treated as “adverse changes” for approval to fund. All loans are subject to an ongoing fee of 1.043% on the outstanding debenture balance, which we believe is structured as a replacement of the existing ongoing borrower fee, thus representing an increase of 29.4 basis points.