Growth Capital

advertisement

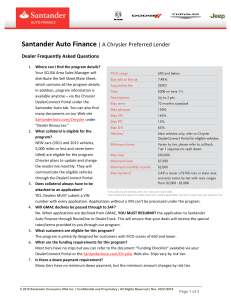

Breaking through the growth restrictions Martin Williams Director, Large Corporates – Eastern region Santander UK 12th September 2012 Background Banking crises 2008 onwards Credit markets tightened Balance sheet v P&L for Banks Basle III capital restrictions Political intervention? QE & Interest rates Continued economic uncertainty Euro contagion 1 Result (1) CASH IS KING! Greater analysis of every loan application Quality of credit submissions paramount Grey hair / no hair increasingly important! Bankers must prove actions taken to address impact of recession Financial evidence that business can demonstrate improving trends and impact of growth Greater reliance on external professional advisors due diligence 2 Result (2) Certain sectors faring better than others (eg. Manufacturing / utilities), but established Banks may face “caps” of exposure; reluctantly lending if they have to, encouraging exit if they don’t Santander and other “insurgents” looking to back better businesses regardless of sector – how good is management and their professional partners? Consider other options (new markets / Local initiatives / LEP / additional debt / Regional Growth Fund / Venture Capital etc) 3 Breakthrough programme The Breakthrough programme will invest £200 million in fast-growth SMEs, supporting local enterprise and community initiatives, creating jobs, inspiring entrepreneurs of the future and turbo-boosting a private sector led economy 1. Breakthrough Growth Capital 2. Breakthrough Live Santander has up to £200 million to invest in fast-growth SMEs turning over between £500k – £10m across the UK. The investment programme will run over the next 3 – 5 years and invest in up to 200 SMEs. Santander is running regional Breakthrough Live conferences for fast-growth SMEs. Working with Santander Universities the Breakthrough Live conferences bring together leading entrepreneurs to share experiences. 3. Breakthrough Masterclasses 4. Breakthrough Talent Santander is running a unique experience programme for fast-growth SMEs that takes them behind the doors of the world’s most iconic and best fast-growth businesses, to learn first hand how they did it – real experience to help their own growth journey. Santander has launched an online portal for SMEs participating in the Breakthrough investment programme to access the best student and graduate talent across our partner University network – including Universities in Scotland. 5. Breakthrough Responsibly In keeping with our focus on responsible business, Santander has launched a number of initiatives to encourage more responsible and inclusive business practice and to invest in Social Enterprise development. 6. Breakthrough International This initiative will help SMEs participating in the Breakthrough programme to reach new overseas markets if their growth plans and ambitions are beyond the UK. It includes subsidised trade missions, educational roadshows and support accessing information on exporting. What is Growth Capital? Growth Capital is one of the pillars of the SME Breakthrough Programme www.santanderbreakthrough.co.uk Santander has committed to make available £200m of funding to support high growth SMEs that have advanced beyond the start-up stage. 5 High Growth firms: locations The number of High Growth firms has not changed much despite the recessionary pressure. They employ almost 50 % of work force 5 years of successful growth, higher gearing, lower solvency rate Our product was designed to address the financing gap GAP Growth capital Criteria 10 We are looking to invest in SMEs with the following broad characteristics: Annual turnover £0.5m – £10m although flexible Minimum 3 year trading history Strong p.a. growth in a combination of sales, profits and / or employee numbers Track record of sustainable operating profitability and cash generation Proven management team • Businesses need not bank with Santander today but would have to bring their banking to us to benefit from a growth capital loan. Product features 11 Santander Growth Capital is a debt product rather than an equity product. Subordinated behind conventional senior bank debt as a mezzanine loan which allows a greater risk / return profile. The typical, key characteristics of the product are: – Loan amounts: £0.5m to £3m (in addition to senior debt) – Term: 3 to 7 yrs – Pricing: 10% margin (5% above LIBOR paid quarterly; 5% rolled up and capitalised) – Repayment: Bullet or refinance – no interim capital repayments – Security: Second ranking security for the subordinated loan 12 Benefits For SMEs Debt finance support is not limited to available security. Flexible form of financing supporting development / growth capital projects and initiatives. Management do not need to dilute their equity ownership. Due diligence process is quicker and less expensive than for equity financing. Free, extensive ongoing support with additional training and mentoring from “Breakthrough” activities. No early repayment penalty. Purpose and Practicalities • Financing must be growth initiative led with a clear benefit to the business. Projects need not generate new employment but these cases will be viewed favourably. Example projects might include: Investment in a new production line Implementation of a new IT platform Creation of an HR function Exploration of overseas markets or manufacturing • • What these examples have in common is that they are all asset light from a security perspective but ultimately value creating. We will not be attracted to deals where the majority of the investment is for refinancing existing debt or facilitating cash out to shareholders. We also expect to be supporting owner-managed businesses rather than those who have already secured institutional equity investment. 13 Summary If you are waiting for things to get back to the 2007/8 environment, you may have a (very) long wait Now is the new norm Growth is achievable with the right support Invest the time in sourcing suitable partners; use what is out there Believe in yourself and your business 14 Important Notice • • • The information and opinions in this document have been compiled by Santander Corporate Banking in good faith from sources believed to be reliable. The information and opinions contained in this document are published for the assistance of the recipients but they should not be relied upon as authoritative or definitive and should not be taken into account in the exercise of judgements by any recipient. Distribution of this document does not oblige us to enter into any transaction. Any offer would be made at a later date and subject to contract, satisfactory documentation and market conditions. Nothing in this document constitutes investment, legal, tax or accounting advice and we recommend you do not make a decision based on this information without first taking the appropriate advice. This document is intended for recipient only, should not be disclosed to retail clients, and should not be distributed to others or replicated without the consent of Santander Corporate Banking. Santander Corporate Banking is the brand name of Santander UK plc, Abbey National Treasury Services plc (which also uses the brand name of Santander Global Banking and Markets) and Santander Asset Finance plc, all (with the exception of Santander Asset Finance plc) authorised and regulated by the Financial Services Authority, except in respect of consumer credit products which are regulated by the Office of Fair Trading. FSA registration numbers: 106054, 146003 and 423530 respectively. Registered offices: 2 Triton Square, Regent’s Place, London NW1 3AN and Carlton Park, Narborough LE19 0AL. Company numbers: 2294747, 2338548 and 1533123 respectively. Registered in England. Santander and the flame logo are registered trademarks. .