1099-MISC

IRS

Reporting

Form 1099-MISC

Raffles

Civil Air Patrol

2009 National Conference

Learning Lab FM02

Stacy Jackson

Introduction

Wing Responsibilities for 1099-MISC Reporting

1099-MISC

Prizes and Awards

Rent and Royalty Payments

Services

Attorney Payments

Scenarios for Volunteers

Raffles

Wrap Up

Questions

Wing Responsibilities

Be diligent with Accounts Payable postings. The first step is having correct information.

Have only one vendor card for each vendor.

Your WFA can merge vendor cards if more than one card exists for a vendor.

Verify that transactions posted are accurate.

Indicate 1099 Eligible Vendors in QuickBooks

Done by editing the vendor and checking the 1099 option under the “Additional Info” tab.

Add the vendor Taxpayer ID information to QuickBooks

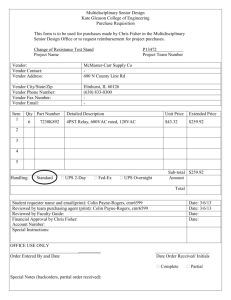

Vendor Edit Screen

Check this box if vendor is eligible for

1099 reporting

Enter vendor Tax

ID from W9 here

Wing Responsibilities

Decide which vendors should receive a 1099-

MISC

Obtain Form W-9 from vendors

The Form W-9 is used as a tool to obtain the necessary information from vendors. It will help determine if payments to vendors are reportable.

A Form W-9 should be obtained from all vendors and kept on file at wing headquarters.

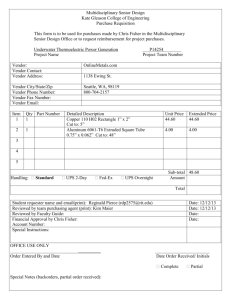

W-9 Example

Vendor should choose one business type.

Vendor must sign!

Vendor should enter one TIN number. This number should match their annual tax returns.

Wing Responsibilities

Determine the amount to be reported on each

1099-MISC

Provide all information needed to file your

1099-MISC Forms to your WFA. A spreadsheet will be provided that will aid in consolidating the information.

All information must be provided no later than Jan

15 th for the preceding calendar year.

NHQ will file all 1099-MISC Forms with the IRS, state tax authority, and recipients

1099-MISC

Required for the following

Prizes and Awards

Rent and Royalty Payments

Services performed by individuals who are not employees and are not incorporated

Gross Proceeds paid to Attorneys

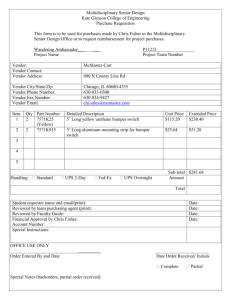

1099-MISC Example

All of the information for the recipient must match their annual income tax return

Prizes and Awards

Reportable amount:

$600 per calendar year

Information needed:

Individual’s name and address

Individual’s Social Security Number

Total amount of all prizes and awards paid to the individual or on the individual’s behalf during the year

Example:

Flight scholarships or any cash awards to members

Scholarships are considered awards unless paid to a candidate to attend an educational institution for a degree

Rent and Royalty Payments

Payments made to corporations and governments are not required to be reported

Reportable amount:

$600 per calendar year for Rent

$10 per calendar year for Royalties

Information needed:

Name and address that the vendor uses to file their annual tax return

Taxpayer Identification Number that the vendor uses to file their annual tax return

Total amount of all rent or royalty payments paid to the vendor during the year.

Example:

Hangar rental, office rental, or storage rental

Services

Payments made to corporations are not required to be reported.

Reportable amount:

$600 per calendar year

Information needed:

Name and address that the vendor uses to file their annual tax return

Taxpayer Identification Number that the vendor uses to file their annual tax return

Total amount of all payments made for services to the vendor during the year.

Example:

Catering, facility cleaning, lawn care, or pest control

Attorney Payments

Payments made to corporations must still be reported.

Reportable amount:

•

Reportable for any amount paid per calendar year

Information needed:

•

•

•

Name and address that the vendor uses to file their annual tax return

Taxpayer Identification Number that the vendor uses to file their annual tax return

Total amount of all payments made to the vendor during the year

Example:

•

Retainers and legal fees paid to law firms

Scenarios for Volunteers

There are several instances when a 1099-MISC is required to be sent to volunteers.

A volunteer receives a flight scholarship or activity scholarship from a CAP entity.

A volunteer receives a cash award from a CAP entity.

A volunteer rents out hangar, office, or storage space to a CAP entity.

A volunteer provides cleaning or lawn care services to a CAP entity and receives compensation.

Raffles

All raffles must be reported to NHQ/FM prior to the raffle taking place.

All required information must be obtained by the Wing or Unit.

IRS Form 5754 must be completed by each winner.

All prizes with a fair market value of $600 or more must be reported to the IRS.

IRS Form W-2G

Raffles

All prizes with a fair market value of $5000 or more are taxable.

Winner will pay 25% withholding tax on the fair market value less the initial wager. This must be collected from the winner when they collect the prize.

OR

Wing or Unit sponsor will pay 33.33% withholding tax on the fair market value less the initial wager.

NHQ/FM will complete all IRS Forms and filing requirements.

Taxes will be drafted from the Wing or Unit bank account and submitted to the IRS

Form 5754 Example

All information must be completed by

Part II = only taxable winners

W-2G Example

Some Final Notes

All forms must be filed with the same information as the individual or business uses to file their income taxes each year

Sole Proprietorships should be sent in the individual’s name, not the business name

Forms sent to individuals should contain their social security number, not an employer identification number.

All information should be reported by calendar year, not fiscal year

Some Final Notes

The Wing is responsible for obtaining all information via Form W-9 or Form 5754.

The IRS penalizes $50 per form for incorrect information filed on 1099 Forms or W-2G Forms that are not supported by the required back up.

If You Get Stuck or Need Help

Contact your Wing Financial Analyst

Contact National Headquarters

Stacy Jackson, WFA

sajackson@capnhq.gov

877-227-9142, Ext. 427

Cell – 334-224-7657