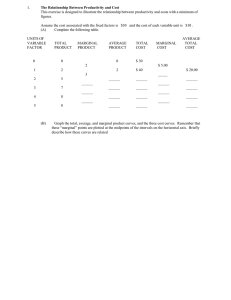

Review Sheet

advertisement

AP Microeconomics (Modules 55,56, pgs 567-570 in Module 57, 58-60) Test on Tuesday 3/24/15 Test Checklist Note: Review multiple-choice questions at the end of every module and additional multiple-choice questions provided with on line resources that come with the book. Modules 55 –Production Costs in the Short Run Study Activity 31 1. Understand the relationship between total cost, average cost and marginal cost curves. Be able to identify each of these curves on a graph and explain why the marginal cost intersects the average cost curves at their minimum points. 2. The marginal product curves and marginal cost curves are mirror images of each other – marginal costs in the short run begin to increase because of diminishing returns to input. 3. Fixed costs – remain constant over all levels of output --Average Fixed Costs – decrease with output as the overhead gets spread over a greater number of units produced. Module 56 Study Module 56 Reading Questions 1. Long –Run Production Costs – all inputs and costs are variable. --Economies of Scale, Constant Returns to Scale, Diseconomies of Scale. Modules 57 (pgs. 567-570), 58, 59 and 60 – Perfect Competition Study Reading Questions on Perfect Competition 1.) Know the characteristics of Perfect Competition (P.C.) (pg. 568-570) 2.) Know the difference between the industry’s supply and demand curves and the individual firm’s. 3.) Perfectly Competitive (P.C.) firms maximize profits by producing the last unit where MR > = MC. (This is called the Optimal Output Rule). For P.C., since MR=Price, we can restate this to say Price >=MC. 4.) P.C. has a perfectly elastic demand curve – understand the significance of this. 5.) Understand why the P.C. firm’s supply curve is the marginal cost curve above the minimum average variable cost (AVC). 6.) In the short-run, a P.C. firm that is producing can make profits, minimize losses or break-even. A P.C. will continue to produce (and not shut down) in the short-run as long as its price per unit is greater than or equal to the AVC. This is the same as saying it will operate as long as it makes enough total revenue to pay for its variable costs, or its losses are equal but not greater than its fixed costs. 7.) Understand why P.C. firms must break-even in the long-run (Price =ATC). Know what the graph for a P.C. firm at long-run equilibrium looks like. 8.) Be able to define allocative efficiency (producing a mix of goods most desired by consumers, which occurs where price = MC) and productive efficiency (producing in a least costly manner, which occurs where Price = min. ATC) 9.) Know why the P.C. firm is allocatively efficient in the short-run and long run, and productively efficient only in the long-run.