Fi800 Valuation of Financial Assets

Fi8000

Valuation of

Financial Assets

Milind Shrikhande

Associate Professor of Finance

Today

☺ Syllabus

☺ Course overview

☺ Lecture Sequence: Options…

Syllabus

☺ Expectations

☺

Be here

☺

Ask questions

☺

Work practice problems

☺ Required skills

☺

Spreadsheet (Excel) and Internet

☺ Required materials

☺

Text: Bodie, Kane and Marcus 6 th edition

☺

Solutions manual

Syllabus

☺ Grading

☺

3 Quizzes @ 20% each

Similar to or related to practice problems and examples

No make-ups

☺

Final exam (comprehensive) @ 30%

☺

Stock-Trak assignment @ 10%

☺ Make-up Policy

☺

No make-up quizzes

☺

Everyone must take the final exam

Syllabus

☺ Grading – Typical Department Policy

☺

No more than 35% A

☺

Majority (approximately 50%) B

☺

Lagging performance earns a C or lower

☺ Administrative – Withdrawal with a WF

☺

Beyond 3 absences from class

☺

Withdrawal after the semester midpoint

☺

Withdrawal while doing failing work

Syllabus

☺ Materials

☺

(Financial) Calculator – bring every day

☺

Text – leave it where you read it

☺

Lecture notes, handouts – provided

☺ Office Hours

☺

Drop-in, phone, e-mail and by appointment

Approaches to Valuation

☺ Discounted cash flows

The value of an asset is related to the stream of expected cash flows that it generates, and should reflect compensation for time and risk .

☺ Arbitrage pricing

When two assets have exactly the same stream of cash flows (magnitude, date, state) their prices should be identical.

Valuation of Financial Assets

Bonds Stocks Derivative

CF stream

Time line

Risk coupons and face-value fixed maturity dividends no maturity default risk systematic risk contingent on contract and underlying asset fixed expiration contingent on contract and underlying asset

Discounted Cash Flows (DCF) Valuation

The Idea

The value of an asset is the present value of its expected cash flows.

The Philosophical Basis

Every asset has an intrinsic value that can be estimated, based upon the characteristics of the stream of cash flows that the asset generates.

Inputs for DCF Valuation

☺ The magnitude of the expected CFs

☺ The timing of the expected CFs

☺ The risk level of the expected CFs

Assumptions Underlying DCF

Valuation

☺ Magnitude : investors prefer to have more rather than less.

☺ Timing : investors prefer a dollar today rather than a dollar some time in the future.

☺ Risk : investors would rather get a certain CF of

$1 than get a lottery ticket with an expected

(average) CF of $1.

The Mechanics of DCF

CF

1

CF

2

CF

3

CF

4

CF

T

|--------|--------|--------|--------|---------------|---> t

0 1 2 3 4 … T

Value

f CF t t

,

T k

Notation

PV = Present Value

FV = Future Value

CF t

= Cash Flow on date t t is the time (date) index ( t = 1, 2, …, T ) k = risk-adjusted discount rate

(risk-adjusted / opportunity cost of capital) rf = risk-free discount rate

(use as the discount rate if the probability of default is zero) g = growth rate

The Mechanics of Time Value

Compounding

Converts present cash flows into future cash flows.

Discounting

Converts future cash flows into present cash flows.

The Additivity Principal

Cash flows at different points in time cannot be compared or aggregated. All cash flows have to be brought to the same point in time before comparisons or aggregations can be made.

Compounding a Cash Flow

$100 FV

|--------|-----> t k = 5%

0 1

FV

100 1.05 $105

$100 FV

|--------|--------|---> t k = 5%

0 1 2

FV

2

$110.25

PV FV

|--------|--------|-----------|---> t

0 1 2 … T

FV

PV (1

k )

T

Example

In a study of returns on stocks and bonds between 1926 and 1997, Ibbotson and

Sinquefield found that on average stocks made 12.4% annual return, treasury bonds made 5.2% and treasury bills made 3.6% .

Assuming that these returns continue into the future, what will be the value of $100 invested in each category for 1year, 5 years, 10 years?

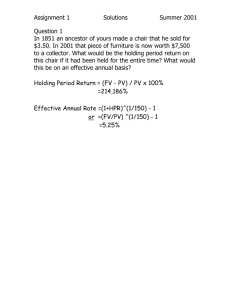

Holding

Period

1

Solution

Stocks

$112.40

T.

Bonds

$105.20

T.

Bills

$103.60

5

10

$179.40

$128.85

$119.34

$321.86

$166.02

$142.43

Discounting a Cash Flow

PV $100

|--------|-----> t k = 5%

0 1

PV

100

1.05

$95.24

PV $100

|--------|--------|-----> t k = 5%

0 1 2

PV

100

1.05

2

$90.70

PV FV

|--------|--------|------------|---> t

0 1 2 … T

PV

FV

(1

k )

T

The Present Value of a Stream of Cash Flows

CF

1

CF

2

CF

3

CF

4

CF

T

|--------|--------|--------|--------|--------------|---> t

0 1 2 3 4 … T

PV

(

1

)

(

2

PV CF

T

)

(1

CF

1 k )

(1

CF

k

2

)

2

CF

T

(1

k )

T

t

T

1

CF t

(1

k ) t

Examples

1.

How much will you pay today for a project that is expected to pay a dividend of $500,000 three year from now, if the appropriate (riskadjusted) annual discount rate for this project is 10%?

2.

What is the value of a project that is expected to pay $150,000 one year from now and

$500,000 three years from now, if the appropriate (risk-adjusted) annual discount rate for this project is 10%?

Solutions

1.

PV = $500,000/(1+0.1) 3 = $375,657.40

2.

PV = $150,000/(1+0.1) 1 + $500,000/(1+0.1) 3

= $136,363.64 + $375,657.40

= $512,021.04

Cash Flow Streams –

special cases

A growing perpetuity:

CF CF(1+g) … CF(1+g) (t-1) …

|---------|---------|-------------------|-------------------> time

0 1 2 … t …

PV

(1

CF

k )

CF

(1

(1

k

)

2 g )

t

1

CF (1

g )

(1

k ) t

CF (1

g )

(1

k ) t

...

CF k

g

(if k

g )

Example

In 1992, Southwestern Bell paid dividends per share of $2.73. It’s earnings and dividends had grown at 6% a year between

1988 and 1992 and were expected to grow at the same rate in the long term. The rate of return required by investors on stocks of equivalent risk was 12.23%.

What should be the value of the stock?

Solution

Current dividend per share = $2.73

Expected growth rate g = 6% = 0.06

CF

1

= $2.73 ·(1+0.06) = $2.8938

Discount rate k = 12.23% = 0.1223

PV

2.8938

$46.45

Example - continued

In fact, the stock was actually trading at $70 per share. This price could be justified by using a higher expected growth rate.

70 g

2.73(1

g )

0.1223

g

8%

Cash Flow Streams –

special cases

A growing annuity:

CF CF(1+g) … CF(1+g) (T-1)

|---------|---------|-------------------|-------------------> time

0 1 2 … T

PV

(1

CF

k )

CF

(1

(1

k

)

2 g ) CF (1

g )

( T

1)

(1

k )

T

t

T

1

CF (1

g )

( t

1)

(1

k ) t

CF k

g

1

1

1

g k

T

Example

Suppose you are trying to borrow $200,000 to buy a house on a conventional 30-year mortgage with monthly payments.

The monthly interest rate on this loan is

0.7%. What is the monthly payment on this loan?

Solution

PV = $200,000

T = 30·12 = 360 k = 0.7% = 0.007

g = 0

$200, 000

CF

0.007

1

CF

$1, 523.7

1

360

The Frequency of Compounding

The frequency of compounding affects both the future and present values of cash flows.

The quoted annual interest rate may be compounded more frequently than once a year. This will affect the effective annual interest rate which is determined by the specified frequency of compounding.

Example

A government note pays a coupon (interest) of 4.75% of par value. This means that a

$1,000 face-value note pays $47.50 in annual interest in two semiannual installments of $23.75 each.

The quoted annual interest rate is 4.75%, but it is compounded semiannually . What is the effective annual interest rate ?

Solution

1

effective rate

1 quoted

rate m

m

1

effective rate effective rate

1

0.0475

2

2

4.8064%

quoted

rate

The Frequency of Compounding

Frequency annual

Semi-annual monthly weekly continuous

Quoted

Rate

10%

10%

10%

10%

10% m

1

2

12

52

∞

Effective

Rate

10.00%

10.25%

10.47%

10.51%

10.52%

Continuous Compounding

1

effective rate

1 quoted

rate m

m

As m goes to infinity (m

) we get

1

effective rate

e

The Frequency of Compounding

- continued

1

effective m period

rate

effective period

rate

m

If one sub-period is a monthe and m=12, then

1

effective

annual

rate

effective

monthly

rate

12

If one sub-period is 6 months and m=4, then

1

effective year

rate

effective months

rate

4

Terminology and Notation

The quoted annual rate is also called the

APR (Annual Percentage Rate)

The Effective Annual Rate is the EAR

We will use the notation r q,annual r eff,annual

= quoted annual rate

= effective annual rate r annual

= annual rate (when r q,annual

= r eff,annual

)

Example

The quoted annual rate of return is 10%, compounded semiannually . Calculate the following rates: a.

Effective rate for 1 year (10.25%) b.

Effective rate for 2 years (21.55%) c.

Effective rate for 18 months (15.76%) d.

Effective rate for 6 months (5%) e.

Effective rate for 2 months (1.64%)