Investment Recommendation

Hold

Pricing

Closing Price (9/18/08) $97.82

52 Wk High (9/19/08) $110.74

52 Wk Low (11/20/08) $37.18

Ave Vol (10 day)

1.1M

Valuation

P/E

Current Ratio (mrq)

Quick ratio (mrq)

Debt/Equity (mrq)

ROA (ttm)

ROE (ttm)

ROI (ttm)

12.8

1.65

0.99

0.36

11.2%

28.1%

17.1%

Margins

Gross Margin (ttm)

Oper Margin (ttm)

Net Prof Margin (ttm)

35.8%

14.2%

9.8%

“Flowserve Corporation (Flowserve) is a manufacturer

and aftermarket service provider of comprehensive flow

control systems. The Company is engaged in

developing and manufacturing precision-engineered

flow control equipment, such as pumps, valves and

seals, for critical service applications. Through the

manufacturing platform, the Company offers a range of

aftermarket equipment services, such as installation,

advanced diagnostics, repair and retrofitting. The

Company operates in three business segments:

Flowserve pump division (FPD) for engineered pumps,

industrial pumps and related services; flow control

division (FCD) for engineered and industrial valves,

control valves, actuators and controls and related

services, and flow solutions division (FSD) for precision

mechanical seals and related products and services.”

(WSJ)

Flowserve operates in 56 countries worldwide and

employs around 15,000 people. The company serves

various industries including oil and gas, power

generation (nuclear and solar), chemical processing,

water resources, and general industry. Although about

60% of the company’s revenue is from the oil and gas

and chemicals industry, they are establishing a

presence in the clean and renewable energy field as

well. The company recently booked orders from the

solar power generation industry totaling $31.5 million.

They also received orders from Westinghouse for valves

to be used in nuclear power generators. (Reuters)

Flowserve’s presence in many different industries, as

well as competing sectors in the energy field makes it

well positioned for the future. They have grown net

income as well as EPS each of the last 5 years. In fact,

EPS is up 1,579% since the end of fiscal year 2004.

While this is impressive, the important thing to focus on

is continued growth for this mid-cap company.

Analyst: Jesse Bunse

Jhbcx5@mail.missouri.edu

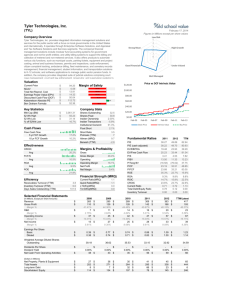

One can see by the chart above that Flowserve has consistently performed better than

its competitors as well as the S&P 500 over the past 5 years. While past performance

of a security is no guarantee of future performance, it is apparent that Flowserve’s

business model over the past half-decade is quite strong. The large dip in stock price

apparent at the end of 2008 coincides with the market crash, but more importantly the

quick drop in the price of crude oil, a major source of revenue for the oil and gas

industry that it serves. As more and more rigs and pipelines have become profitable

again, the stock price has risen accordingly.

Relative Valuation and Margins

Flowserve Corporation’s largest competitors by market capitalization are ITT

Corporation (ITT), IDEX Corporation (IEX), and Gardner Denver, Inc. (GDI). While

these companies compete with Flowserve in at least one specific industry, many are

diversified across other industries that Flowserve does not engage in. Therefore, any

relative valuation should be applied with a grain of salt. Below is how each company

stacks up with relation to one another.

Company

P/E

EPS (ttm)

FLS

ITT

GDI

IEX

12.6

11.4

10.4

14.5

$7.64

$4.20

$(3.04)

$1.16

EPS Growth

(ttm)

19.1%

11.6%

(175.3)%

(40.7)%

Debt/Equity

Current Ratio

0.36

0.52

0.48

0.42

1.65

1.49

2.29

2.42

As far as EPS and EPS growth, FLS is ahead of the competition. A September 14,

2009 S&P report projected EPS for 2009 at $8.15 (after $0.50 realignment charge) and

$9.65 in 2010.

Company

Gross Margin

Oper Margin

FLS

ITT

GDI

IEX

35.8%

27.6%

30.5%

39.0%

14.2%

9.9%

(6.3)%

11.3%

Net Profit

Margin

9.8%

6.9%

(8.2)%

6.8%

Sales Growth

(5 yr)

14.7%

17.8%

35.6%

13.3%

As margins are concerned, FLS shows signs of a healthy company compared to its

competitors. With a high rate of revenue growth, more of these dollars will reach the

bottom line. In the same report referenced earlier, analyst expectations were that FLS

gross margin would increase to 36.0% in 2009 from 35.3% in 2008. This trend is

observable from in the gross margin for the most recent quarter above. Margins tell a

lot about management of a company, and FLS has shown itself to be very efficient in

funneling cash from revenues to profit.

Balance Sheet Snapshot

On the balance sheet, the company looks fairly strong. The current ratio of 1.65 and the

quick ratio of .99 mean that they have the capabilities of meeting short term debt

obligations well. Also, they are well positioned to take advantage of new opportunities

with a high cash balance and a relatively low LT debt to equity ratio of 0.34. This figure

is only 77.83% compared to the industry as a whole, meaning that the company could

lever up if needed. Their total debt is valued at $570.98 million. Total debt to equity is

0.36, and this figure has been steadily decreasing since 2004, when it was at nearly

0.81. (Balance sheet data from WSJ) Very good news came out on September 18th, as

S&P upgraded its rating of Flowserve debt to BB+, one step away from investment

grade. This means that new debt can be issued at much lower rates, especially if

investment grade is achieved. (Dow Jones Newswires)

Income Statement Snapshot

Looking at the income statement (mrq) with relation to debt, the interest coverage ratio

for FLS is quite high (very attractive) at 16.02, another indicator that the company is not

burdened by debt, and is in a good position to lever up if needed. Since 2004, total

revenue is up 77.34% (as of last fiscal year), and net income after taxes is up an

astonishing 1,539%. This is from increased revenues compounded by a healthy 3.07%

average annual growth rate for the gross margin. These figures provide a basis for the

large appreciation in stock price since 2005. This company has shown high rates of

growth in the past few years, but analysts doubt we will see such impressive figures in

the near future. (Income statement data from WSJ)

Capital Expenditures

Capex for the future is hard to project, and for a company in a period of high growth like

FLS past data may not tell the whole picture. The 5 year average used in my DCF

evaluation below has a range from $45 million in 2004 to nearly $127 million in 2008.

Yet, the company projects that capex will be down to $100 million for 2009.

Future Oil Outlook

It has been established that the company is well positioned for the future, but it is

important to look at the economic conditions surrounding the end users of Flowserve’s

products and services. The following is a forward curve for crude oil futures reaching

out past June 2016.

It shows that the market sees crude reaching above $80.00 again by 2013. The most

important piece of information to get out of this graph is that the market currently does

not see crude oil reaching last year’s highs of near $150.00/barrel. While this may be

discouraging for the oil and gas industry, there is still healthy, sustainable growth on the

horizon. This, of course, is based on the assumption that the global recession is

nearing an end, and a period of expansion has begun. (Bloomberg) While OECD

countries will see virtually no growth in liquid fuel consumption from 2009-2010, nonOECD countries (such as the BRIC nations) will see an increase in consumption. More

specifically, world oil consumption (weighted GDP) will increase 2.4% in 2010.

(eia.doe.gov) It is safe to say that world oil consumption will increase in the near future,

and that as this happens more and more rigs will need to be built and maintained.

Sales by

Market 2008

6%

15%

Oil and Gas

General Industrial

39%

Chemical

17%

Power Generation

Water Treatment

23%

% of Bookings

YTD

18%

35%

Oil and Gas

Water

Power Generation

19%

Chemical

7%

General

21%

Revenue by

Region 2008

8%

35%

18%

North America

Europe

Middle East/Africa

Asia Pacific

11%

Latin America

28%

Source: Standard and Poor’s

Revenues

Information about the company’s 2008 revenues shows a dependence on the oil and

gas market. Also, 63% of revenues come from North America and Europe, showing a

concentration on more developed markets. Data from Flowserve’s Q2 2009 earnings

report shows sales growth in the Europe, Middle East and Africa region increasing to

44% of total sales, while North American sales decreased to 31%. I believe that there is

significant room for expansion in more developing markets where margins may be

higher, and the company’s healthy debt positions makes this a possibility. A statement

from S&P made on 9/14/2009 supports this conclusion. “What we see as FLS's strong

balance sheet and financial flexibility should aid results, while operating margins likely

expand on a better mix and plant realignments.”

Revenues-Future Developments

While little data on the previous two quarter’s revenue distribution is available, recent

bookings in solar power generation mentioned earlier show an uptick in demand (or

perhaps better marketing by FLS). Also, the Westinghouse order for its nuclear plants

indicates that for 2009 and beyond, power generation may be a larger part of revenues.

This bodes well for the company, as while nuclear and solar plants are much costlier

than their gas and coal powered counterparts, recent political and social developments

signal renewed interest in these forms of energy generation. New “Generation III”

nuclear plants may come on line as early as 2012. (WSJ) As engineers find ways to

make these plants safer, more cost-effective, and less wasteful, the future of nuclear

energy (which uses a lot of the components and services offered by FLS) will get

brighter. Yet, oil will not go away anytime soon, and the company’s core competence in

this industry will provide the bulk of revenues for years to come.

DCF Valuation

I chose to use the Warren Buffet Style DCF valuation. I used a beta of 1.428 from

Bloomberg, which was comparable to the average of betas from sites such as Yahoo!

Finance and CNBC. With a risk free rate of .13 and a historical market return of 11%,

the CAPM equation is as follows:

.13+1.428(11-.13)=15.65

I felt that this discount rate was slightly high, even for a mid-cap company like

Flowserve. I chose a more appropriate 13%. The growth rate for 2010 corresponds to

analyst coverage that that oil demand will not pick up fully until 2011. After this, used a

growth rate of 12% per year, which is conservative in that it is still well below previous

growth rates. Thereafter I used a 7% growth rate that corresponds to analyst

consensus. A 3% growth rate into perpetuity was used, while I think that a higher rate

may have been reasonable due to the company’s current potential. This led to an

intrinsic value per share of $94.51, which is just below what the stock is currently trading

at. With a lower discount rate of 12%, this becomes $105.36, slightly above the current

trading price. The inherent conservatism of my estimate is apparent in the high rates of

growth the company has seen in recent years. The reason for this decision was that

rates like previously seen cannot continue forever, yet when growth will slow down is

still somewhat in the air.

The table below shows the effects of different discount and first stage growth rates.

Sensitivity

12%

13%

14%

15%

Discount Rate

5%

$85.80

$77.61

$70.95

$66.43

7.5%

$101.76

$91.56

$83.26

$76.40

10%

$120.89

$108.20

$97.91

$89.42

11%

$129.56

$115.73

$104.53

$95.29

12%

$138.86

$123.80

$111.61

$101.56

Management

Flowserve selected Mark A. Blinn as the company’s next president and CEO. It should

be a smooth transition, as former CEO Lewis Kling has planned a retirement for

February for some time. Kling will remain with the company as a member of the Board

of Directors. The company has a Non-executive Chairman of the Board, which is good

in that it separates leadership and oversight.

Company Structure

Flowserve has three divisions, the pump division, flow control division (valves), and the

flow solutions division (seals). Each division includes original equipment sales as well

as aftermarket service. An increase in sales can translate into multiplied future

revenues due to the service function. The Q2 2009 earnings report showed little

change from Q2 2008, when original equipment sales made up 65% and aftermarket

services made up 35% of total sales. Being able to service its own equipment provides

future revenue, but also a good opportunity to see firsthand how to improve products.

FLS as a whole is a relatively simple organization which is good for transparency in

reporting. Another component of the company’s structure that has been of importance

to date is their large global presence and the negative foreign currency effect this has

had lately. A weakening dollar in the future would be good news for any company

repatriating funds into the United States. As our economic committee projected this

happening, FLS stands to benefit in the future if they can mitigate risk in foreign

currency transactions outside the US.

Concluding Remarks

In recent years, Flowserve has proven itself a very exciting company. A quick glance at

a 5 year history of stock prices shows that a lot of money has been made (and lost) with

the company. While I do not believe the security will reach previous highs of over

$120/share anytime soon, there is definite potential to reach this milestone again. The

appeal of the company is its concentration on its core competencies (pumps, valves,

and seals) coupled with its presence in all major markets that use these components.

They are present globally, and achieve less than 40% of their revenues from North

America. Flowserve is a well positioned company, but I through my DCF valuation I

believe that they are a little on the pricy side currently. While they are an excellent

company, I would hesitate to increase our holdings too much at the current share price.

I think we need to keep an eye on the company, and revisit increasing our holdings at a

later date. Currently, we hold 525 shares of FLS valued at $51,355.50. This is around

5% of the total portfolio. Depending on the risk appetite of the group, increasing

holdings would not be out of the question, but I feel the prudent move would be to sit on

what we currently have.

Sources

Wall Street Journal Online

www.Flowserve.com

www.yahoofinance.com

www.google.com/finance

www.scottrade.com (used to obtain S&P and Reuters Reports)

eia.doe.gov

Bloomberg

0

0