Industrials

advertisement

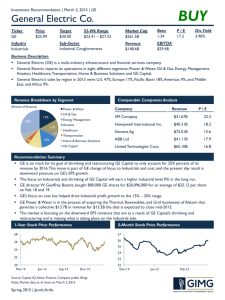

Company Analysis - Industrials By: Hahn, Wesley; Hartman, Michael; Heschel, Andrew; Holzman, Joshua 1 Agenda Recap class decision to hold industrials Review SIM Holdings Recommendations Conclusion 2 Recap: Class voted to leave Industrials underweight by ~1.5% relative to S&P500 Sector S&P 500 SIM Weight +/Weight 3 Consumer Discretionary Consumer Staples Energy Financials Health Care Industrials Information Technology Materials Telecommunication Services Utilities Cash 10.65% 11.05% 12.27% 14.00% 11.51% 10.56% 19.68% 3.56% 3.02% 8.74% 12.24% 12.41% 10.06% 11.77% 9.08% 21.69% 3.25% 4.12% -1.91% 1.19% 0.14% -3.94% 0.26% -1.48% 2.01% -0.31% 1.10% 3.70% 0.00% 2.57% 3.98% -1.13% 3.98% Current Positions (Industrials) Industrials ~10% of portfolio 4 Recommendation 5 Overall Recommendation Industrials is starting to trend up! United Technologies (UTX) has limited forward upside and Flowserve (FLS) and Danaher (DHR) have value positions and forward momentum. We recommend selling a portion of our position in UTX and levering up equally the position of FLS and DHR. DHR FLS UTX 6 % Assets Recommended % 2.83% 3.59% 2.80% 3.56% 3.03% 1.52% Levering % 126.77% 127.05% 50.00% Union Pacific 7 Union Pacific Railroad Conclusion: Current Market Price ~$102, or a +10% price premium relative to target price of $93. Aggressive growth-rate estimates + 2013 2012 2011 8% 8% 9% ( Revenue Growth Rates Low proportionate cost growth + EPS estimates > Consensus 8 = 1 year price target of $93. EPS - diluted Consensus Estimate (+/-) 2012 2011 $8.92 $7.08 $7.75 $6.50 15% 9% United Technologies Corporation 9 United Technologies Corporation Provides high technology products and services to the building systems and aerospace industries worldwide. Otis, Carrier, UTC & Fire Security, Pratt & Whitney, Hamilton Sundstrand, and Sikorsky Market Cap: $71.63 B Current Price: $79.05 2.7% Dividend Yield Target Price: $84.76 (+7.2%) Current Weight: 3.13% Recommend: Sell 157 bps 10 UTX – Positives Global Footprint: big in BRIC countries and emerging markets. History of strong growth and earnings over the past 10 years. Strong Balance Sheet and Free Cash Flow Ripe for new acquisitions. Recent Acquisition - Goodrich Well diversified company. 11 United Technologies Corp. has won a maintenance contract worth up to $350 million to support Japan Airlines’ fleet of Boeing 787 aircraft. United Technologies said Monday that its subsidiary, Hamilton Sundstrand Corp., would provide the maintenance for the fleet of 35 aircraft. UTX – Risks & Concerns Foreign Exchange: Over of business is done overseas, particularly in Europe. Potential strengthening dollar, recently weak dollar has boosted earnings. Integration of Goodrich acquisition. Complementary products, may not see the results in our time frame. Defense spending. State of the Economy. UTX doesn’t sell direct to end users. 12 BofA Merrill Lynch: “If we assume run rate net synergies approach 30% (based on a conservative estimate) of GR’s 2010 selling and administrative costs and are phased in and $3.4bn paid in cash (assuming that UTX leaves $2bn in cash on its balance sheet in keeping with its historical precedent), we estimate the deal would neither be accretive nor dilutive to 2012 earnings. Assuming synergies phase in in year two, we estimate 2013 could be accretive last few months, some see UTX taking a risk in paying for up for GR at present. UTX appears to be focused on maintaining its credit rating, judging by the amount of equity to be used in the transaction” UTX – Valuation 13 Relative to Industry P/Trailing E P/Forward E P/B P/S P/CF High 20.6 18.7 5.0 1.6 17.2 Low 8.2 8.9 2.2 0.7 6.4 Median 16.8 15.6 3.6 1.3 12.9 Current 14.1 12.9 3.0 1.2 11.0 Relative to S&P 500 P/Trailing E P/Forward E P/B P/S P/CF High 1.3 1.1 1.8 1.1 1.6 Low 0.57 0.46 0.9 0.6 0.7 Median .98 0.99 1.3 1.0 1.3 Current 1.1 1.0 1.5 1.0 1.3 UTX – Valuation Con’t Absolute Valuation A. P/Forward E P/S P/B P/EBITDA P/CF High Low Median Current B. C. 18.7 8.9 1.6 0.7 5.0 2.2 11.78 4.59 17.2 6.4 D. 15.6 1.3 3.6 9.17 12.9 E. 12.9 1.2 3.0 7.57 11.0 #Your Target Multiple F. 14.0 1.3 3.5 8.5 12.0 Average: $85.14 Target: (80/20 DCF & P/E) $84.76 Sell 157 bps of UTX. Limited Upside. Foreign Exchange Concern. 14 Wait and see what happens with global economy and Europe. *Your Target E, Your Target Price S, B, etc/Share (F x G) G. H. 5.89 82.46 61.56 80.03 24.54 85.89 10.36 88.06 7.44 89.28 Danaher 15 Danaher Overview Designs, manufactures and markets professional, medical, industrial and commercial products and services Operates in five segments: Test & Measurement Environmental Life Sciences & Diagnostics Dental Industrial Technologies Outperforming the S&P 500 and Main Competitors (5 Year) Growth derives from both segment core expansion and frequent external acquisitions Danaher Key Statistics Market Cap: $33.82 Billion Current Price: $49.27 Target Price: $59.26 (20.3% Upside) Recommendation: Buy 125 bps DHR vs. GE vs. S&P500 Over a 5 year time period... Danaher Positives Strong sales in foreign markets, notably those with growing economies Will thrive during early stages U.S. economic recovery Experienced management knowledgeable in the “Danaher Business System” Strong sales and revenue growth Danaher saw outstanding year-over-year core revenue growth, core operating margin expansion, cash flow and earnings performance. With purchase of Beckman Coulter, decreased exposure to potential economic decline Danaher Concerns Other companies are acquiring former Danaher managers Over 70% of sales growth in the last 5 years has come from acquisitions Large investment made with the $6.8 billion purchase of Beckman Coulter showed low Q3 earnings Absolute Valuation What are the experts saying… Flowserve 23 Flowserve Overview Sector: Industrial Goods Industry: Diversified Machinery Sells precession engineered flow control equipment. Three Segments FSG Engineered Products Division FSG Industrial Products Division Flow Control Division International operations No competitors are all inclusive : valves, pumps, and seals. Revenues $ 4,032,036 24 Flowserve Performance They are a growth company and over the last 5 years they 25 have seen an 87% increase in net income. Bookings up 15.9% versus previous year at $1.16 billion Recent increases in costs and decreases in Margins. Significant backlogged low to medium margin high cost projects. Rapid growth in short term projects and original equipment Record service and aftermarket bookings (support) of 42% of bookings ($488 million) Company commitment to equity value with share buy backs and large insider buys. Flowserve Concerns Operating margins continue to shrink for the last five quarters to 33.6% Currency exposure continues to effect bookings, 15.9% is effectively 10.2%. Large backlog of projects that continues to growth. People are not committing on large projects. SG&A and cost controls are offsetting lower earnings and will not continue forever. 26 Flowserve Conclusion: Historically has traded well above it’s competitors and the S&P 500. 27 Flowserve Conclusion: Current Market Price ~$97, trading close to the ratio’s. The value is being realized. Absolute Valuation A. P/Forward E P/S P/B P/EBITDA P/CF 28 High Low Median Current B. 53.9 2.1 6.0 16.26 28.0 C. 6.2 .2 .9 1.89 3.1 D. 15.1 .9 2.8 7.26 10.4 E. 10.3 1.1 2.0 6.78 9.1 #Your Target Multiple F. 15.1 .9 2.8 7.26 10.4 Target Target Price G. 7.34 73.29 41.00 11.19 9.27 H. 110.834 65.96 114.8 81.24 96.422 Flowserve Conclusion: Current Market Price ~$97, or a 26% price discount relative to target price of $131.16. Growth-rate estimates consistent with past performance + = 1 year price target of $131.16 is conservative. Terminal Discount Rate = Terminal FCF Growth = 29 Current Price Implied equity value/share Upside/(Downside) to DCF $ $ 12.0% 3.0% 97.30 131.16 34.8% 2012 2011 20% 18% 15% $6,593 $5,494 $4,656 ( Revenue Growth Rates ( EPS estimates < Consensus 2013 Revenues EPS - diluted Consensus Estimate (+/-) 2012 2011 $8.26 $8.91 $7.07 (under mgmt. $7.45) $7.69 15% 9% 30 Appendices 31 A: UTX DCF 32 B: Danaher DCF 33 C: Flowserve DCF 34