Writing Tax Research Memos

advertisement

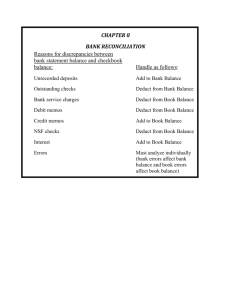

Writing Tax Research Memos BA 630 Individual Tax Purposes To find a solution to the tax problems of one’s clients or employer • To organize the facts, issues, and conclusions of the project To facilitate a review of the research activities by colleagues To allow for subsequent examination of the research issue Audience Users : are well versed in federal tax law understand frequent and complete references to primary and secondary sources of the tax law need no introduction to the hierarchy of tax authority or to statutory citation practices Organization Tax research memo consists of three main parts: 1. Brief Introduction • Summary of the facts • List of the issues • Conclusions 2. Supporting Analysis 3. Recommended Actions Introduction Include the date Provide a complete list of facts Clearly state tax issues that the client faces Immediately after issues, provide an unambiguous conclusion as derived from supporting analysis Facts Provide a heading to clearly identify and set off the facts Provide a complete statement of facts Include only facts provided by the client Pay attention to the timing of the events Combine all related facts together so that they reside in one location Issues State issues clearly and unambiguously Write issues in question form Provide sufficient detail so that the issue’s tax implication is clear, but avoid including a detailed cite within the issue Number and arrange issues in the most logical order Issues: Examples Not a question and vague Question and specific A question arises as to how much a taxpayer can deduct the payment he made for the lessons. Can part or all of the $13,000 payment be deducted and, if so, what is the character of the deduction? Issues: Examples Unclear tax concept Explicit tax concept What is the tax treatment for a company under Reg. §1.162-5(c)(1) when it pays its employee’s tuition? Can Borden Company deduct the $2,300 it pays to Smith to cover his tuition? Issues: Examples Accounting concept Tax concept Can Bikes-R-Us, Inc. expense the rental payment to its chief financial officer? Can Bikes-R-Us, Inc. deduct the rental payment to its chief financial officer? Conclusions For each issue in dispute, give a clear and unambiguous conclusion in a separate sentence Then, proceed to explain logically how you arrived at your conclusion Supporting Analysis Discuss tax authority in sufficient detail to show its relationship to the client’s situation Connect logically each cited authority with the facts Make your line of reasoning so clear that misinterpretation is impossible Supporting Analysis Insufficient Better The theft loss is deductible in 2001 according to §165(e). Section 165 (e) indicates that theft losses are deductible in the taxable year sustained. Thus, the theft loss is deductible in 2001. Supporting Analysis If the clearest tax authority is a ruling or judicial decision, always begin with the most relevant Code provisions Next, discuss any related Regulation if it narrows the focus or clarifies the statutory law Finally, finish with the on-point or analogous judicial decision or ruling Recommendations State the required follow-up actions If the research is related to proposed transactions, explain the recommended changes Use of abbreviations Abbreviate common tax terms, especially in citations: - Reg. rather than Regulation or Treasury Regulation - Rev. Rul. rather than Revenue Ruling - IRC rather than Internal Revenue Code Avoid, however, the temptation to abbreviate many words and phrases beyond commonly accepted The End! Materials used: • Writing Tax Research Memos Web site http://www2.gsu.edu/~accerl/ • Federal Tax Research by W. Raabe