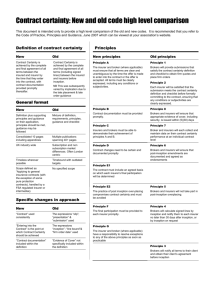

Signed Lines Guidance

advertisement

The Calculation and Notification of Signed Lines Market 1. Introduction 1.1 This paper sets out additional guidance to clarify, and in some cases change, market practice in relation to the calculation of signed lines, and to the means of notification of signed lines to insurers. It has been produced in response to a commitment to the FSA to provide further guidance on these topics during December 2005. 1.2 The Contract Certainty Project Board (CCPB) and the Market Reform Group (MRG) have considered both broad principles and some relatively detailed out-workings of the principles. The body of the paper sets out the proposals that have been agreed to date. Further guidance will follow. 2. Contract Certainty Background 2.1 The market has agreed a definition of Contract Certainty (“CC”), as follows: ”Contract certainty is achieved by the complete and final agreement of all terms (including signed lines) between the insured and insurers before inception.” 2.2 This is clarified in the CC Code of Practice which establishes the principle that brokers will calculate signed lines by inception and notify them to each insurer no later than 30 days after inception, or by inception date on request. Guidance on abiding by this principle notes that: ”Wherever possible, the [signing down] calculation method should be explicit on the submission, subject to client wishes, allowing the insurer to determine how their line will be calculated.” 3. Calculation of Signed Lines The broker should obtain client instructions regarding signed lines prior to inception, wherever possible. 3.1 Pre-Inception Signing Method The submission should clearly state the method that will be used to calculate signed lines. In the absence of a signing clause on the submission, or client instructions, the following principle applies: That losses, premium allocation and risk exposure for the duration of the contract will be determined via the following sequence: 3.2 through the application of any lines to stand (such lines not to exceed 100% of the order); followed by pro rata signing of the remaining lines. Client Instructions Post-Inception Any post-inception change(s) in signing must be agreed by the affected parties. www.lmp-reforms.com This note is provided for information purposes only and is not intended to be binding. The Market Reform Programme Office, Society of Lloyd’s, IUA, LMA and LMBC accept no responsibility whatsoever for liability as a result of any reliance placed on it. Furthermore, non-compliance with any matter contained in the note shall not invalidate or call into question any contract or agreement nor shall failure to comply with the standards or guidelines create any right of action or claims in any third party. This note does not affect the legal relationships between the parties to insurance/reinsurance contracts. V1.1. 20/12/05 The Calculation and Notification of Signed Lines Market 4. Interim Arrangements for the Notification of Signed Lines 4.1 There is agreement between brokers and insurers that the de-linking of premium accounting transactions is a practicable approach, in the majority of cases, to the routine communication to insurers of signed lines, which are settled through the bureau, within 30 days of inception date. NB. There are other means of advising signed lines e.g. premium settlement (stage 1 not de-linked), flexible settlement, FDO. 4.2 It is recognised by brokers and insurers (whether bureau or non-bureau) that notification of signed lines is needed at inception in order to meet the contract certainty definition. Notification within 30 days is therefore an interim solution and the aim, over time, will be to reduce the timescale. Signed lines are available to the insurer at inception by asking the broker for early notification, or by writing a line “To Stand”. 4.3 In the short term it is for individual insurers, in conjunction with brokers, to identify the means by which they will accept and record the notification of signed lines at inception (e.g. the use of repositories, phone or email) and the audit trail associated with the notification process. Slip repositories may provide a partial solution to notification of signed lines, but will not provide the automated approach offered by de-linking. 4.4 The following approach is being taken to drive greater usage of de-linking across the bureau market: MRPO will work with insurers to identify, analyse and (where necessary and practical) create work-arounds for class of business issues which inhibit insurer usage of de-linking. LMBC will seek commitments from brokers regarding the usage of de-linking and/or other means of notifying signed lines within 30 days. IUA/LMA will promote the acceptance of de-linking amongst their members, and the adoption of the early bureau signing message, based upon these broker commitments. The LMA are developing safeguards to address those classes where there are concerns regarding the potential for policy issuance in advance of the receipt of premium. MRPO will provide CCPB and Associations with Lloyd’s statistics on adoption, use and timeliness of de-linking by brokers and insurers. IUA will consider matching this approach, for the company bureau. MRPO and the Associations will continue to monitor the usage of de-linking, and to promote increased up-take. 4.5 It is proposed that, in the short term, the routine means of providing signed lines to non-bureau insurers within 30 days will be by means of closings (de-linked from the premium settlement), and which may be on paper or via electronic closing messages. Brokers and non-bureau companies are encouraged to enter into bi-lateral agreements regarding the form and timing of their closing notifications. www.lmp-reforms.com This note is provided for information purposes only and is not intended to be binding. The Market Reform Programme Office, Society of Lloyd’s, IUA, LMA and LMBC accept no responsibility whatsoever for liability as a result of any reliance placed on it. Furthermore, non-compliance with any matter contained in the note shall not invalidate or call into question any contract or agreement nor shall failure to comply with the standards or guidelines create any right of action or claims in any third party. This note does not affect the legal relationships between the parties to insurance/reinsurance contracts. V1.1. 20/12/05