Budget 2011 Highlights The Government is going ahead with plans

advertisement

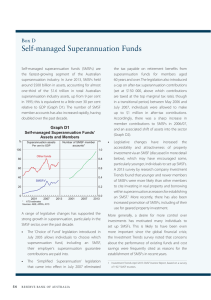

Budget 2011 Highlights The Government is going ahead with plans to exempt up to $500 of interest income from tax. In a bid to crack down on income splitting, children will no longer receive the low income tax offset for unearned income (subject to some exceptions). Company tax rate – confirmation of previous announcement The Government has confirmed that it will cut the company tax rate to 29 per cent from the 2013/14 financial year. It will then be cut further to 28 per cent from the 2014/15 financial year. To assist small business companies the Government has announced that they will be eligible for 28 per cent company tax rate from the 2012/13 financial year. Low income tax offset to be reflected in PAYG withholding The amount of the low income tax offset (LITO) refunded through reduced PAYG tax withholding is to be increased from 50% to 70%. The remaining 30% of LITO will still be paid as a lump sum on assessment of income tax returns. Children and low income tax offset This measure provides for a limitation of the ability of minors to access the low income tax offset (LITO). From 1 July 2011, children under the age of 18 will be unable to reduce the tax they would otherwise be obliged to pay on their 'unearned' income (eg dividends, rent, interest and royalties) by accessing the LITO. Importantly, any income earned by minors from any work they do will not be affected, and similarly for any compensation payments and inheritances they receive. Phase out of dependent spouse tax offset The dependent spouse tax offset will be phased out for taxpayers with a dependent spouse born on or after 1 July 1971. The change will not affect taxpayers with an invalid or permanently disabled spouse, supporting a carer, or people who are eligible for the zone, overseas forces and overseas civilian tax offsets. Interest bearing accounts/annuities The Government confirmed that from 1 July 2011 taxpayers will be eligible for a 50 per cent discount on the first $1,000 of interest earned per annum. This will include interest earned on deposits, bonds, debentures and annuity products as well as interest earned indirectly through managed funds. There had been speculation that this measure would be deferred to 1 July 2012. Marginal Tax Rate* 15% 30% 37% 45% *Excluding Medicare Levy Tax saving per annum $75 $150 $185 $225 Increase to medical rebate threshold The Government previously announced that from 1 July 2010 the medical rebate threshold would increase from $1,500 to $2,000. It is only net medical expenses above this amount that are eligible for the 20% tax offset. In future, this threshold will increase by the CPI, with the first increase to take effect from 1 July 2011. Superannuation There was a welcome announcement on excess contributions and confirmation of the increase in Superannuation Guarantee (SG) and additional Government superannuation support for low income earners. Unfortunately predicted changes to the rules on personal deductible superannuation contributions did not take place. Refund of excess concessional contributions The Budget announced that individuals will now have the option of a refund up to $10,000 of any excess concessional superannuation contributions, made by them or on their behalf in any particular year. Where this choice is made, the amount refunded will be assessed as income to the individual at their marginal rate of tax, rather than incurring excess contributions tax. However, the choice will only be available for breaches in respect of the 2011/12 year or later years, and only for the first year a breach of the contribution caps occurs. Self Managed Superannuation Funds (SMSFs) The $150 supervisory levy imposed on SMSFs will increase to $180 from the 2010/11 year. This revenue will be used to fund some minor changes to the regulation of SMSFs that were recommended by the Cooper Review. The most significant change is the introduction of a penalty regime so that the Australian Taxation Office (ATO) can punish breaches in a measured and appropriate way. At the moment the ATO’s only choice is to make the whole fund non-complying and subject to the top marginal tax rate. The other noticeable change is that fewer accountants will be entitled to audit SMSFs. Those that will be auditing SMSFs will have to register and pay a registration fee. Super contribution information on payslips From 1 July 2012 employers will be required to show on payslips the actual amount of superannuation paid into accounts. In addition, superannuation funds must notify employers and employees quarterly if regular payments cease. Minimum payment amounts for superannuation pensions restored by 2012/13 In recent years, the Federal Government has sought to cushion self-funded retirees who source their income from a superannuation income stream against the effects of financial market instability. This has been achieved by temporarily reducing the minimum payment factors for account-based, allocated and market-linked pensions. The 2011/12 financial year will be the last year these measures will apply, with the 'regular' minimum payment factors being restored on 1 July 2012. This means that the minimum pension factors for superannuation income streams will be as follows until 30 June 2011. Age 55-64 65-74 75-79 80-84 85-89 90-94 95 or older Regular percentage factors 4% 5% 6% 7% 9% 11% 14% 2011/2012 year 3% 3.375% 4.5% 5.25% 6.75% 8.25% 10.5% Clarification of tax treatment of limited recourse borrowings As previously announced, the Government will amend the income tax treatment of assets purchased using limited recourse borrowing arrangements to provide certainty for superannuation funds by treating them as the owner of the underlying asset for income tax purposes, with effect from 1 July 2007. This has been seen as necessary as currently, a technical interpretation of the law does not support the accepted practice. Superannuation co-contribution — pause to the indexation of the income threshold extended to 2012/13 The Government announced in the 2010/11 budget that the income thresholds will remain at $31,920 and $61,920 for the 2010/11 and 2011/12 financial years. This has been extended for a further year to 2012/13. The 2011/12 budget re-announced the following measures: Increasing the Superannuation Guarantee to 12% The Government has confirmed that it will increase the SG rate from 9% to 12%, with increments of 0.25% in the first two years, and 0.5% thereafter. The increase will be phased in from 1 July 2013. Government superannuation contribution for low income earners The Government has confirmed that from 1 July 2012 individuals on adjusted taxable income of up to $37,000 will have a 15% matching rate applied to concessional contributions made up to a maximum annual amount of $500. A permanent increase in the concessional contribution cap to $50,000 per annum for those over 50 The Government has confirmed that the transitional measure (that was due to expire on 30 June 2012) afforded to contributors aged 50 years of age and over should remain permanently for those with account balances of less than $500,000.